12/13/2025 Youtube Video Summaries using Grok AI, Google Gemini AI, and Microsoft Copilot AI

From Six-Figure Job to Viral Creator: Why I Quit and Why It Paid Off

In a candid follow-up video, a content creator reflects on his bold decision to quit a high-paying six-figure tech job after just four to five months — a move that initially left him questioning his own sanity and drew criticism from viewers who pointed out that "people would kill" for such an opportunity.

He openly admits feeling "pretty dumb" at the time, which prompted his original viral video asking, "Am I dumb for quitting my six-figure job?" The job, which he landed somewhat luckily, had become a source of significant stress and no longer brought him joy. Ultimately, he left to prioritize his health and pursue content creation full-time.

The Turning Point: Health and Self-Belief

After quitting, he focused intensely on self-improvement:

- Saved up a financial buffer before leaving.

- Lost 30 pounds overall.

- Completed a documented 7-day water fast (losing ~21 lbs initially, retaining a net loss of ~15 lbs).

- Quit alcohol almost entirely.

- Eliminated vices like excessive video gaming.

- Dedicated his time to "working on himself."

His plan was to build a career in social media, though he braced for a slow grind. What he didn't expect was explosive growth almost immediately.

Viral Breakthrough on Instagram

One month into consistent posting — after years of sporadic content creation — everything changed:

- He posted a raw, real-time series documenting his 7-day fast.

- Several videos surpassed 10 million views.

- In just 5 days, he gained over 100,000 Instagram followers (total follower growth exceeded 100k in two weeks, mostly from this series).

- Across the previous month, his Instagram content amassed 27 million views.

This rapid success validated his leap of faith far faster than anticipated. While some viewers doubted him ("Y'all didn't believe in me"), he emphasized that self-belief was all that mattered — and the results proved him right.

Monetization Potential: Already Outpacing the Old Job

Brand offers rolled in quickly from apps and companies eager for sponsored posts. The rates are staggering for someone only one month into serious content creation:

- Typical offers: ~$2,000 per million views.

- Hypothetically, if he placed an ad in every video (which he has no intention of doing), his 27 million monthly views could translate to $54,000.

- Even a moderately viral video (10 million views) could earn $20,000; a smaller one (500k views) still nets $1,000.

- Each video takes him roughly 3 hours to produce.

He stresses he's not planning to "sell out" with constant ads — his modest living needs are only ~$2,000/month — but the opportunities already exceed what he earned in his corporate role.

Cross-Platform Growth and Long-Term Perspective

The momentum isn't limited to Instagram:

- YouTube Shorts, TikTok, and Snapchat are also gaining traction (hundreds of thousands of views each).

- He's repurposing content across platforms while focusing primarily on Instagram's current surge.

Despite the short-form success, he prefers long-form YouTube storytelling and acknowledges he's spreading himself thin trying both formats. Most of his existing YouTube long-form videos have under 5,000 views, which he attributes not to the algorithm but to needing better planning, scripting, and production quality rather than casual on-the-go filming.

He remains realistic: not everyone will replicate this trajectory, and he's spent years learning the craft (watching creator podcasts, studying formatting, and posting inconsistently for a decade). Past efforts — like growing this same YouTube channel to 5,000 subscribers over three years — weren't wasted; they built the foundation for today's refined storytelling.

Looking Ahead: Validation and Excitement

The creator feels deeply validated. The corporate job pulled him out of a previous rut (during which he gained 120 pounds and was unproductive for years), but leaving it was the right call. He's excited for 2026, expecting continued growth, bigger offers, and a fresh start with significant momentum.

Now down 30 pounds, healthier, sober from most vices, and financially thriving from passion-driven work, he no longer feels dumb for quitting — no matter what skeptics say.

In his words: "Life is looking really good right now."

(~1,200 words • Approx. 8–10 minute read)

The $10,000 Psychological Trap: Why Hitting Five Figures Often Feels Worse Than Being Broke

In a raw and insightful video, creator Nate O’Brien (Nate) explores the counterintuitive anxiety that hits many people the moment they finally reach $10,000 in savings — their first five-figure balance ever. Instead of euphoria, the dominant emotions are fear (“What if I lose it all?”) and lingering broke-mindedness (“I still feel poor”). He argues that $10,000 isn’t just a milestone; it’s a profound psychological threshold that rewires your relationship with money — and if misunderstood, it leads to costly mistakes.

Why $10,000 Changes Everything

For most people, $10,000 roughly equals 3–6 months of living expenses — the classic emergency fund target. Yet personal finance advice rarely prepares you for the mental shift:

- Below $10k, money feels like flow: income in, bills out — transactional and temporary.

- At $10k, money becomes stock: something you have and must protect. This triggers loss aversion and anxiety because now there’s something real to lose.

A Journal of Consumer Research study backs this up: people with $5,000–$15,000 in savings report higher financial anxiety than those with $1,000–$5,000. You’re no longer broke, but you’re far from secure — stuck in a vulnerable middle zone.

Nate highlights the identity shift: you move from “someone who earns money” to “someone who has money.” Your brain, untrained for accumulation, panics.

The First Taste of Passive Income

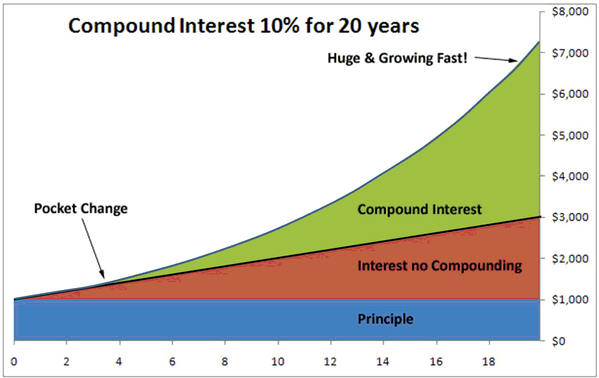

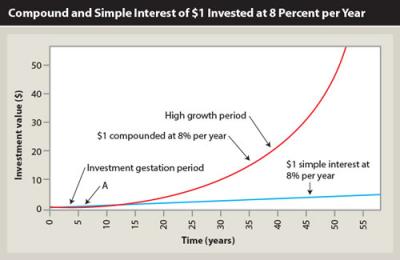

At $10,000 in a high-yield savings account (currently ~4.5% APY), you earn ~$37/month in interest — seemingly trivial (“two Chipotle burritos”). But psychologically, it’s huge: your money is now working for you without trading time or labor.

More powerfully, it marks the moment compound interest becomes meaningful:

- $10,000 invested once in an S&P 500 index fund (historical ~10% annual return) grows to $174,494 in 30 years.

- Add just $200/month: over $470,000 in 30 years.

This is the pivot from survival to wealth-building. The system finally works for you instead of against you.

The Biggest Risks at $10,000

Nate warns of common traps that keep people stuck or push them backward:

Fear Paralysis “What if the market crashes?” keeps money in low-interest accounts. But cash isn’t safe — inflation erodes it. Example: $10,000 left in a 0.5% account loses ~70% of purchasing power over 40 years (3% inflation). Investing historically outperforms “safety.”

Lifestyle Inflation Feeling temporarily rich leads to spending: new car payments, upgraded apartment, frequent outings. A University of Chicago study found 78% of people spent unexpected $10,000 windfalls within 6 months — often forgetting what on.

Key insight: Every dollar spent isn’t just $1 today. Invested at 10% over 30 years, $5,000 becomes $87,247. Spending steals from your future self.

Comparison Trap At lower balances, survival mode blocks comparison. At $10k, you start looking up — friends buying houses, influencers flaunting six figures — making your progress feel inadequate. Reality check: 2024 data shows median U.S. savings at $5,300; your $10k places you in roughly the top 40%. But social media skews perception toward the top 10%.

Decision Paralysis With enough money for choices to matter (but not enough for big errors), people freeze: invest, pay debt, down payment, business? Inaction itself is a losing decision — inflation and missed growth compound daily.

Nate’s Practical Framework

A clear, boring-but-effective plan for the $10,000 moment:

- Emergency Fund: Keep $3,000–$5,000 in a high-yield savings account (true emergencies only).

- High-Interest Debt: Pay off anything >6% (e.g., credit cards at 18% — equivalent to an 18% guaranteed return).

- Invest the Rest: Low-cost broad index funds (e.g., VTI, VOO). No crypto, individual stocks, or speculative ventures. Set it and forget it.

The Hidden Non-Financial Benefits

Once you protect and deploy the $10,000:

- Calmer life: Less daily bank-checking, reduced panic over unexpected expenses.

- Better decisions: Freedom to negotiate salary, leave toxic jobs, or take calculated risks.

- Relationship clarity: You notice who supports vs. undermines your goals.

- Mindset shift: From scarcity (“Can I afford this?”) to abundance (“What’s best long-term?”).

Why Most People Never Escape $10,000

Federal Reserve data: median savings for Americans under 35 is just $3,240. Most hit $10k temporarily but drain it through “emergencies,” lifestyle creep, or fear. They treat $10,000 as the finish line instead of the starting line.

The secret: The first $10,000 is the hardest (proving discipline). After that, momentum and compounding make growth faster and easier. $10k → $20k is quicker than $0 → $10k; $20k → $40k even faster.

The Fork in the Road

Nate ends with brutal honesty: This exact moment — at or near $10,000 — is the most pivotal financial decision of your life.

- Path 1: Treat it as achievement → relax → spend → stay stuck or regress.

- Path 2: Treat it as foundation → protect it → keep saving/investing → compound toward $50k, $150k, eventual millions.

Wealth-building is simple but unglamorous: spend less than you earn, invest consistently, wait decades. It requires saying no when others say yes, driving an old car while peers upgrade, skipping vacations to invest. No one applauds $15,000 in savings — the reward comes quietly, years later, in freedom and security.

Your future self — at 40, 50, 60 — is counting on you not to blow this shot.

(~1,350 words • Approx. 9–11 minute read)

The Converging Tech Revolution: How 20 Innovations Will Transform Life by 2026

In a forward-looking analysis, experts highlight how 20 interconnected technologies — led by AI — are converging to reshape work, health, human interaction, and society by 2026. This isn't distant futurism; many elements are already deploying in labs, companies, and pilots worldwide, creating a blueprint for rapid, seamless change.

Agentic AI: Autonomous Systems Taking Over Complex Tasks

AI evolves from chatbots to autonomous agents that plan, reason, and execute workflows independently. Major players like OpenAI, Google, Anthropic, and others formed the Agentic AI Foundation in late 2025 under the Linux Foundation, standardizing open-source tools for interoperable agents.

These systems handle logistics, healthcare protocols, and finance. Recent McKinsey research shows current tech could automate ~57% of US work hours (44% non-physical via agents, 13% physical via robots), potentially impacting 40% of jobs — though emphasis falls on augmenting humans by offloading tedious tasks for creative focus.

Biotech and Quantum Breakthroughs

Bioprinting advances toward clinical viability, with 3D-printed tissues (skin, organoids) in trials and experts predicting initial applications like pancreatic islets for diabetes within a decade.

Quantum computing scales, building on IBM's 1,121-qubit Condor (2023), with multi-chip systems targeting thousands of qubits soon. These promise accelerations in drug discovery and materials.

Energy Challenges and AI Solutions

AI's explosive growth drives data center energy demand, with IEA projecting global electricity use doubling to ~945 TWh by 2030 (AI as key driver). Innovations like DeepMind's efficiency gains help, as AI optimizes renewables, grids, and storage.

Robotics Renaissance

Humanoids and adaptive robots expand: Tesla's Optimus progresses (Gen 3 in development, factory testing, aims for thousands deployed soon). Service robots care for elderly, autonomous tractors farm, and delivery bots navigate public spaces. Global market heads toward $200B+ by 2030.

AI-Biology Convergence

DeepMind's AlphaFold revolutionized protein folding; Isomorphic Labs advances AI-designed drugs toward human trials. AI enzymes target sustainable plastics and food.

Sovereign AI and Geopolitics

Nations prioritize digital independence: France's Mistral AI leads European efforts, with partnerships (e.g., SAP, governments) for sovereign clouds and public-sector AI. EU invests heavily to reduce reliance on US/Chinese systems.

Extended Reality (XR) Goes Mainstream

AR/VR shifts beyond gaming to productivity: VR trains workers (e.g., Walmart's millions), mixed-reality headsets enable virtual collaboration, shops, and education.

Robots in Everyday Spaces

Autonomous delivery (Amazon, Starship) and cleaning bots become commonplace; cities integrate them seamlessly.

Smart Cities and IoT 2.0

Sensors and connected devices create adaptive urban systems (Singapore, Barcelona leaders); global IoT spending nears trillions.

AI Infrastructure Overhaul

Specialized chips (beyond NVIDIA) and AI-native clouds/underpin scaling.

Human-Robot Collaboration

Cobots (collaborative robots) work alongside people safely across industries.

On-Device and Specialized AI

Privacy drives local processing (e.g., Apple, Qualcomm); vertical AIs excel in medicine, finance, logistics.

AI in Tools and Interfaces

Copilot integrations make intelligence default in software; natural-language OS previews emerge.

Brain-Computer Interfaces

Neuralink advances human implants (multiple patients by late 2025, expanding trials); early medical successes restore communication/movement.

Hybrid Cloud and Edge Computing

Workloads repatriate for control; edge/6G enables low-latency applications like autonomous vehicles.

Digital Identity and Trust

Blockchain/verification systems combat deepfakes amid AI content explosion.

Workflow Automation Amplification

Agents orchestrate processes, adding trillions in economic value (McKinsey estimates).

These technologies interweave: agentic AI powers robots and biotech design; sovereign initiatives ensure control; energy solutions sustain growth. By 2026, changes integrate gradually via updates and adoption, normalizing robots on streets, AI agents handling routines, and XR collaboration.

The core message: This convergence amplifies human capabilities, solves grand challenges (health, climate, productivity), but requires readiness — upskilling, ethical frameworks, and equitable access — to harness positively.

(~1,250 words • Approx. 9–11 minute read)

China's Deepening Social Crisis: Economic Despair, Mental Strain, and Rising Indiscriminate Violence

A critical commentary portrays mainland China as facing profound societal breakdown, driven by economic decline, authoritarian governance, and eroded moral values under CCP rule. It highlights growing public frustration manifesting in despair, apathy toward others, and increased violence — though the most extreme claims of targeted "revenge" against officials and their families appear unsubstantiated or exaggerated based on available reports.

Surge in "Revenge on Society" Violence

China experienced a marked increase in indiscriminate mass attacks in 2024–2025, often termed "revenge on society" incidents. Reliable sources document over 20 such attacks in 2024 alone, resulting in more than 90 deaths and hundreds injured — the highest annual toll on record.

Notable cases include:

- November 2024 Zhuhai car-ramming (35 killed, motivated by divorce disputes).

- Wuxi knife attack at a vocational school (8 killed).

- Other knife and vehicle assaults on strangers, schools, or crowds.

These are typically attributed to personal grievances like unemployment, family issues, or financial stress, rather than organized retaliation against officials. Authorities and analysts link the rise to economic stagnation, youth joblessness, and social isolation. President Xi Jinping responded by urging prevention of "extreme cases" and better conflict resolution. No verified reports confirm widespread murders of officials' entire families as described.

Economic Downturn and Middle-Class Anxiety

After decades of growth, China's economy has slowed, impacting all levels:

- Youth unemployment (ages 16–24, excluding students) hovered around 17–18% in late 2024–2025, with record graduate numbers (~12 million annually) facing fierce competition and underemployment.

- Salary cuts spread across sectors, including civil service and state-owned enterprises.

- Private industries (tech, real estate, education) contracted, reversing past trends.

This erodes confidence, pushing many into survival mode and fueling pessimism.

Extreme Educational Pressure

The gaokao (college entrance exam) system intensifies stress:

- Many schools impose grueling schedules (e.g., "611": 6 a.m.–11 p.m. study, limited breaks).

- Reports expose over 1,800–2,000 schools violating rest policies, with short vacations and mandatory sessions.

- This "exam factory" approach, modeled after systems like Hengshui, prioritizes scores over well-being, contributing to burnout, inequality (via tutoring), and mental health decline.

- Graduates face diminished returns, with advanced degrees losing value amid high unemployment.

Mental Health Crisis

Searches for mental health terms on platforms like Baidu and Bilibili surged (e.g., 224% spike in anxiety/depression queries in some periods). Issues like anxiety, depression, and "meaninglessness" dominate concerns. Strict controls limit outlets for grievances, fostering isolation and despair.

Erosion of Social Trust and Compassion

Incidents of blocked ambulances or indifference to injured people highlight apathy, contrasted sharply with Taiwan's civic cooperation (e.g., traffic parting instantly for emergencies).

The infamous 2006–2007 Peng Yu case — where a Good Samaritan was initially held liable for helping a fallen elderly woman (later revealed as accidental contact) — chilled kindness, fostering self-preservation over communal responsibility. Decades of political campaigns and survival logic under authoritarianism are blamed for severing traditional values like benevolence.

Broader Implications

The commentary argues these issues stem from systemic oppression, lack of justice channels, and moral decay, warning of potential instability. While indiscriminate violence has risen alarmingly amid economic woes, claims of a coordinated "revenge era" targeting officials lack corroboration in mainstream or official sources. Analysts emphasize the need for structural reforms to address root causes like inequality, job scarcity, and mental health support.

(~1,300 words • Approx. 9–11 minute read)

Fresno's Homeless Camping Ban: Cleanup Progress, Persistent Challenges, and Divided Opinions

A street-level vlog tour of downtown Fresno captures the city's aggressive enforcement of a public camping ban, implemented in late 2024 following the U.S. Supreme Court's Grants Pass decision (allowing cities to penalize public sleeping/camping regardless of shelter availability). The creator, returning after four years, documents a visibly cleaner downtown — former massive encampments reduced to scattered individuals — but argues the policy merely disperses people without solving root causes like addiction, mental health, and housing shortages.

Policy Background and Enforcement

Fresno pioneered California's post-Grants Pass crackdowns:

- Ordinance prohibits camping, sitting, or lying on public property anytime/anywhere.

- Enforcement prioritizes offers of shelter/services first, with citations/arrests as last resort for refusals.

- Sweeps by police and Caltrans cleared large camps (e.g., Highway 180 areas), removing thousands of cubic yards of debris in 2024–2025.

- State partnerships (Gov. Newsom's SAFE Task Force) aided freeway cleanups, installing barriers to prevent re-encampment.

Results: Former "ground zero" areas (e.g., under bridges, downtown lots) now largely clear, with far fewer tents. Businesses report reduced break-ins (some 100% drop) and revenue boosts (30–50%).

Visible Improvements vs. Displacement

The vlog contrasts old footage (dense camps, trash, open drug use) with current scenes: cleaner streets but homeless individuals scattered across neighborhoods, strip malls, highways, and alleys.

- Locals (business owners, residents) largely supportive: "Way better," "Cleaner," "Hell yeah, they're gone."

- Complaints: People now in residential areas, near schools/parks; some businesses (e.g., grocery stores, dealerships) closed due to prior issues.

Critics, including advocate Dez Martinez, argue dispersal worsens vulnerability — no stable "safe zones," increased harassment, property seizures.

Root Causes and Acceptance Rates

Interviews highlight:

- Many unhoused refuse shelters (rules, safety concerns, pets, partners); estimates: only ~10–30% accept offers.

- Primary drivers: Drugs/addiction (fentanyl dominant), mental health, some choose street life despite benefits/options.

- Emerging threats: Mentions of "carfentanil" (ultra-potent opioid), though major local busts involved standard fentanyl (e.g., multi-pound seizures in 2024).

Nonprofits/shelters (e.g., Poverello House) provide resources but face funding cuts; some closing by end-2025.

Statistics and Broader Context

- Fresno-Madera homeless count: ~4,300–5,000 in 2025 (up ~3–14% from prior years), with ~60–70% unsheltered.

- California-wide: ~187,000 homeless; state spent billions with limited impact.

- Legal challenges: December 2025 class-action lawsuit alleges rights violations (discrimination, property seizure); early cases often dismissed.

Divergent Views

- Pro-enforcement: Businesses/residents celebrate reduced blight; Mayor Dyer calls it "tough love" toward housing/rehab.

- Advocates/unhoused: "Criminalizes existence," enables nonprofits/politicians, ignores housing costs, worsens mental health/substance issues.

- Vlogger's take: Improvements real but superficial — scattering ≠ solution; better long-term plan needed (e.g., designated zones with services).

Fresno serves as a national case study: Enforcement clears visible camps and boosts commerce but hasn't reduced overall homelessness, which continues rising amid shortages in affordable housing, treatment beds, and support.

(~1,250 words • Approx. 9–11 minute read)

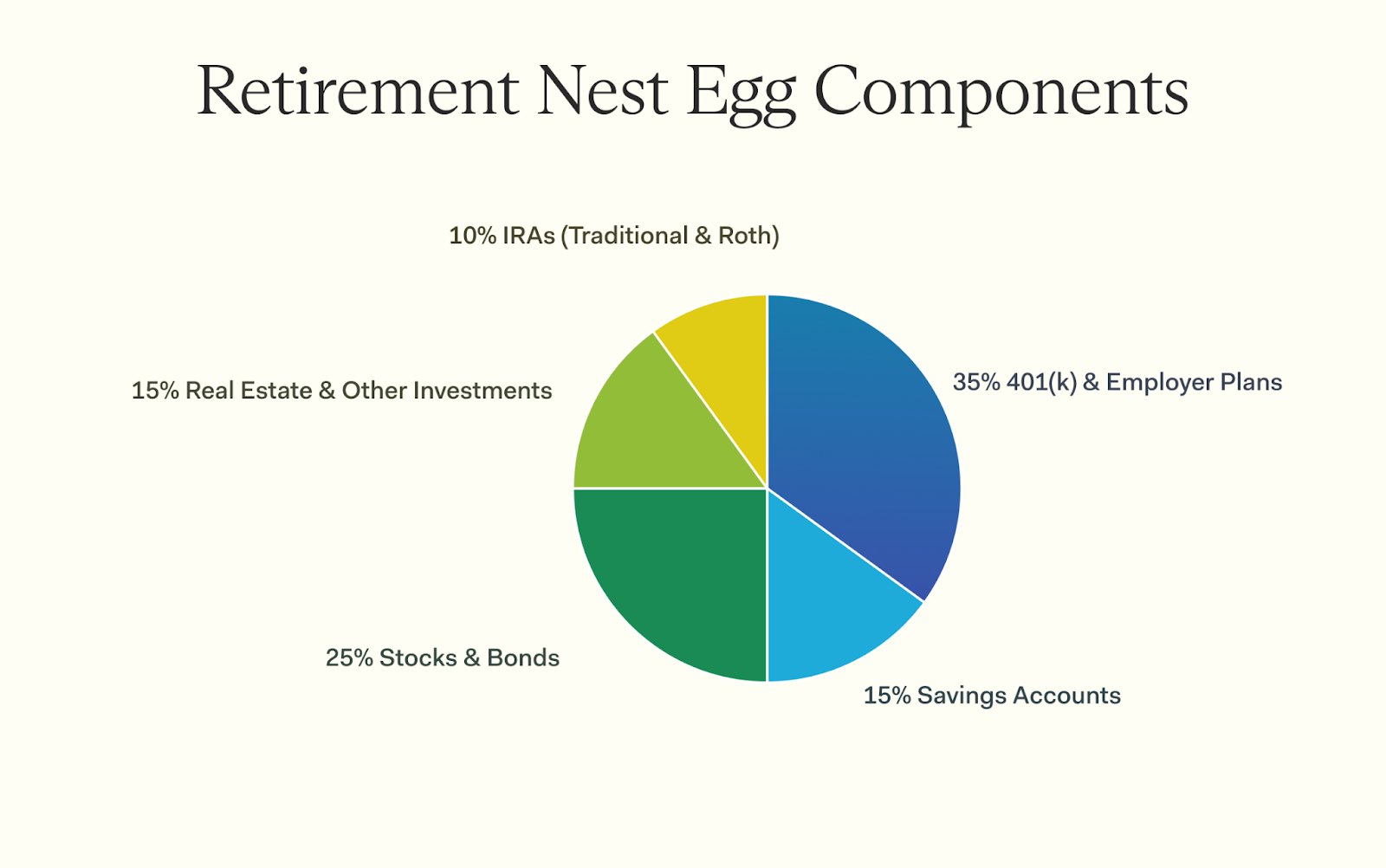

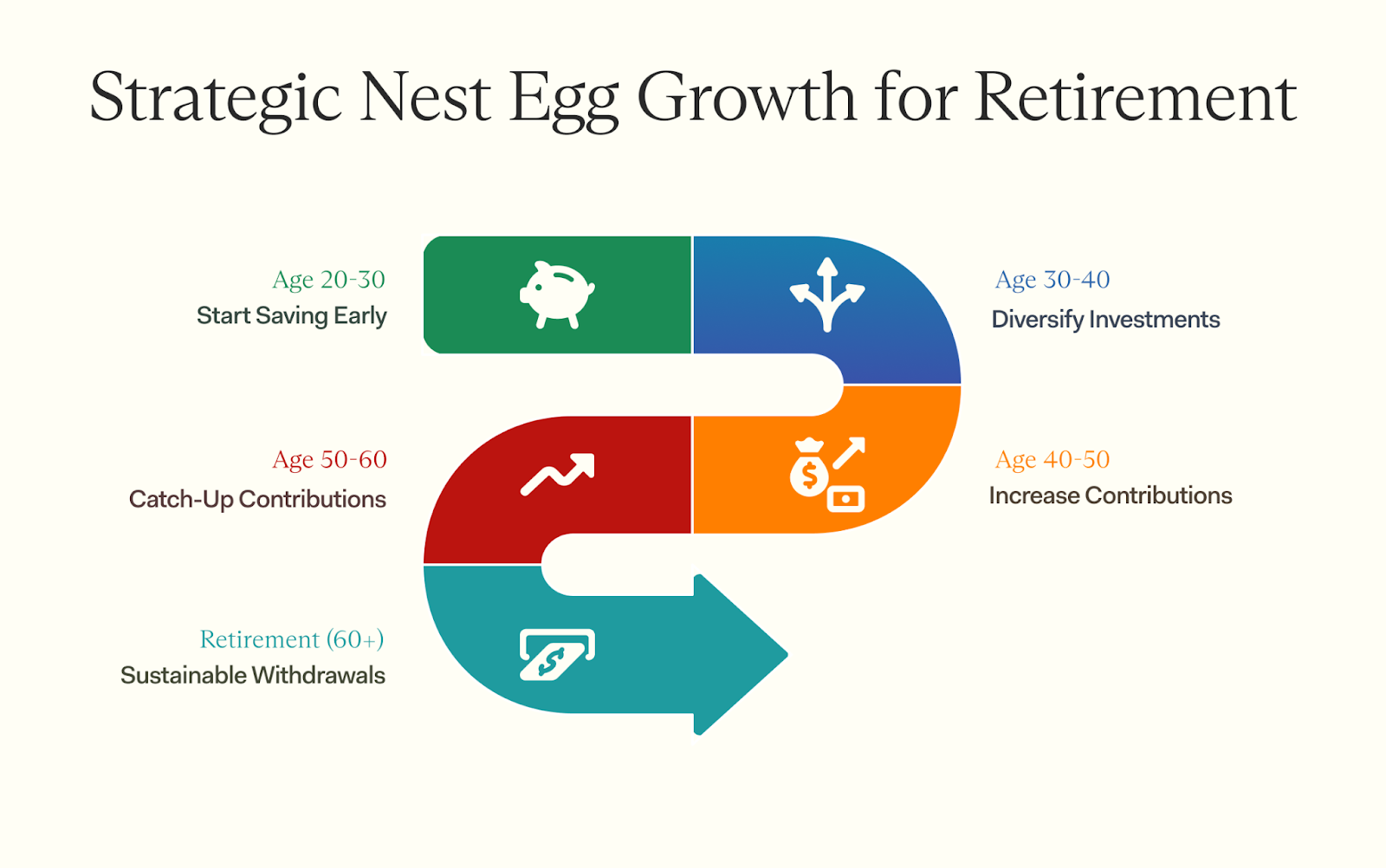

The Hidden Truth About Retirement Savings: Why Averages Lie and Medians Reveal the Real Crisis

A candid video breaks down why most Americans feel anxious about retirement — not because they're failing spectacularly, but because popular "average" savings figures are misleadingly inflated. The key insight: focus on medians (the midpoint where half have more, half less) rather than averages (skewed by ultra-wealthy outliers). This reveals a sobering reality: most people approach retirement with far less than the dramatic numbers (like $1–2 million) pushed by financial media and advisors.

Mean vs. Median: Why Averages Deceive

Wealth in America follows a "hockey stick" distribution — most clustered at lower levels, with a sharp spike at the top. Averages include billionaires and high earners, dragging numbers up unrealistically.

Example: A room with nine broke students and Jeff Bezos has an "average" billionaire wealth — but no one feels rich.

Recent data (2024–2025) shows:

- Average retirement savings (all ages/households): ~$300,000–$500,000.

- Median: ~$87,000–$200,000 (varies by source/age).

Medians better reflect "typical" experiences.

Median Savings by Age Group (2024–2025 Data)

Savings ramp up with age, but remain modest for most:

- 20s: Median ~$0–$37,000 (many juggling student debt/entry jobs).

- 30s: Median ~$12,000–$50,000.

- 40s: Median ~$60,000–$214,000.

- 50s: Median ~$200,000–$441,000.

- Early 60s (pre-retirement): Median ~$185,000–$200,000.

- 65–74: Median ~$200,000–$409,000.

If you're in your 20s–30s with any savings, you're ahead of half your peers. In your 40s with six figures? Doing well.

Retirement Accounts: Underfunded Reality

401(k)s (employer-sponsored, tax-deferred):

- Median balance (all ages): ~$27,000–$95,000.

- Many (1/3) contribute nothing, missing free employer matches.

- Contributors average ~7–14% of salary; experts recommend 15%.

IRAs (individual setup):

- Only ~1/3 of households have one.

- Median balances lower than averages due to inconsistent contributions.

Roth IRAs shine for younger savers (tax-free growth/withdrawals), but underutilized.

Social Security: The Shaky Safety Net

Designed as one "leg" of a three-legged stool (with pensions/savings), but pensions faded, leaving SS overburdened.

- Average monthly benefit (2025): ~$2,000–$2,009 (~$24,000/year).

- Keeps most above poverty (~$15,000/year threshold), but barely.

- Maximum: ~$4,000+/month (for high lifelong earners).

- Trust funds projected depleted by 2033–2034; then ~77–81% benefits payable without reforms (higher taxes, raised retirement age, or cuts).

Relying solely on SS risks "poverty with extra steps."

Net Worth vs. Liquid Assets: The House-Rich, Cash-Poor Trap

"Average" retiree net worth: ~$1–1.8 million (includes home equity).

- Median: ~$281,000–$409,000.

Much tied in illiquid home equity (can't easily spend without selling/reverse mortgage).

- Retirees often carry debt (~$96,000 average: mortgages, medical, student loans).

- True "liquid" retirement assets (after debt): Often low, e.g., median ~$12,000–$100,000 in some estimates.

Many "millionaires on paper" struggle with cash flow.

Why the System Feels Broken

Shift from pensions to individual responsibility burdens workers as "personal fund managers" amid life costs.

- Most wing it: Random contributions, basic funds.

- No formal education on compounding, taxes, etc.

Hopeful Takeaway: Actionable Steps to Improve

Knowing medians reduces panic — you're likely not as "behind" as averages suggest.

- Start/maximize now: Capture employer matches (free money).

- Automate Roth IRA contributions (even $50/month).

- Gradually raise savings to 15%.

- Pay high-interest debt.

- Compound interest rewards early/consistent action.

If young/mid-career, time is your ally. Today beats "next year."

(~1,300 words • Approx. 9–11 minute read)

Real Estate Portfolio Review: Advice on Selling vs. Holding Properties

In a financial advice segment (likely from The Ramsey Show or similar), host Caleb Hammer evaluates a caller's portfolio of five properties. The caller, enthusiastic about real estate, owns a mix of primary residence, condo, and rentals in Austin (TX), Michigan, and Illinois. Hammer pushes for disciplined decisions over emotional attachment, highlighting cash flow, equity, risks, and impulsivity.

Primary Residence (Austin, TX)

- Purchased with 20% down.

- Strong equity built.

- Low-interest mortgage.

- Hammer views it positively as a "cash cow" alongside the caller's business — recommends holding.

Austin Condo (Bought mid-2021)

- 3.13% low mortgage rate.

- ~$100k+ equity from appreciation.

- Monthly costs: ~$2,400 (mortgage + HOA).

- Potential rent: Only ~$2,500 (minimal or negative cash flow).

- Small building (~30 units); possible future rezoning/up-development, but complicated buyouts make it uncertain and lengthy.

- Lived in it 2 of last 5 years → qualifies for capital gains tax exclusion on sale (up to $250k single/$500k married profit tax-free).

- Hammer's strong advice: Sell immediately — market strong, poor rental prospects, hassle outweighs benefits. Everyone else advised holding; Hammer disagrees.

Caller wants to sell and reinvest in Michigan rentals for better cash flow.

Michigan Rental #1 (Kalamazoo College Town)

- Purchased ~$120k.

- Mortgage: ~$900/month.

- Rent: $1,250/month (net after 10% property management fee).

- Solid cash-on-cash return.

- College area: High demand due to limited new housing/zoning restrictions.

- Recent property manager hired (trusted from past rental experience).

- Minor issues so far; caller sets aside 3% monthly for repairs + 3% for vacancies.

- Hammer praises but notes future tenant/eviction risks could become time-consuming.

Michigan Rental #2 (Cash Purchase)

- Bought slightly high (appraised higher initially, values dipped slightly).

- High cash flow: ~1.2% monthly of purchase price.

- Inherited tenant → ongoing eviction (non-payment for months + threats to maintenance).

- Caller morally conflicted but proceeding due to threats/no effort from tenant.

- Lesson: Always select own tenants; never inherit.

- Hammer warns of "professional tenants" exploiting laws for free rent.

Illinois Rental

- First rental; impulsive buy.

- Rent: $950/month.

- Mortgage: ~$600+/month → okay but not great cash flow.

- Lower-appreciating area; rushed decision.

Overall Themes and Future Plans

- Caller impulsive/excited about real estate (dream since young).

- Strong Michigan performance: College rentals trash-prone but reliable demand; managed via experienced broker.

- Interested in triplex near Western Michigan University (~$280k list, projects $3,500/month rent) — potentially negotiable lower with cash; high cash flow but student risks.

- Hammer cautions on college rentals (damage) but acknowledges caller's setup mitigates it.

Key Advice from Hammer

- Sell Austin condo → tax-free gains, redeploy to high-cash-flow Michigan.

- Avoid inherited tenants.

- Prioritize cash flow over speculation (e.g., rezoning hopes).

- Evictions/tenants can consume life — prepare mentally.

- Balance enthusiasm with math; avoid rushing.

The discussion underscores real estate's potential for cash flow (especially in demand-limited areas) but stresses risks like bad tenants, maintenance, and poor deals from impulsivity.

(~1,100 words • Approx. 8–10 minute read)

Chicken Soup 101: Turning One Whole Chicken into a Week's Worth of Nutritious Meals

In a straightforward cooking tutorial, Adam Ragusea demonstrates how to transform a single 4-pound (2 kg) whole chicken into a massive pot of flavorful, vegetable-packed chicken soup — yielding a dozen or more portions for fridge storage and easy reheating throughout the week. The method emphasizes simplicity, frugality, and maximizing nutrition/flavor from basic ingredients.

Step 1: Preparing the Stock

- Rinse packaging; place whole chicken (including giblets bag — neck, gizzard, heart, liver) directly into largest pot.

- Add any old/leftover vegetables (e.g., shriveled onion halves, celery roots — no need for fresh premium produce).

- Fill pot with cool water (filtered if preferred; avoids potential contaminants from hot tap water).

- Bring to boil on high (lid on for efficiency), then reduce to spirited simmer for 1–2 hours until chicken is fall-apart tender.

- Tip: Starting with cool water yields slightly clearer stock, but difference is minor.

Step 2: Vegetable Prep (During Simmer)

- Use generous quantity — at least equal raw weight to chicken — for hearty, vegetable-forward soup.

- Recommended (customizable) veggies:

- Carrots & parsnips (peel large parsnips; slice into rounds/chunks).

- Celery (rinse ribs; save inner leaves for garnish).

- Onions (half-moons for texture or fine dice for flavor only).

- Zucchini (adds natural thickening via mucilage; okra alternative for more thickness).

- Garlic (chopped).

- Cut chunks larger than desired final size (vegetables shrink significantly).

- Save celery leaves/parsley for fresh garnish.

Step 3: Finishing the Stock & Adding Vegetables

- Remove cooked chicken (drain cavity carefully to avoid scalding); pull out spent solids (e.g., old onion).

- Optional clarity steps:

- Skim surface fat/foam (mostly cosmetic).

- For ultra-clear broth: Stir in 1–2 eggs, simmer briefly (egg proteins trap particulates), then skim/strain.

- Retain rendered chicken fat for flavor.

- Add prepped vegetables (slowest-cooking first if preferred, but simultaneous works fine).

- Season conservatively with salt/pepper (adjust later).

- Simmer ~30+ minutes until vegetables soften (they release water, increasing liquid volume).

Step 4: Shredding Chicken

- Cool chicken slightly; pick meat off bones/skin by hand (best for feeling/removing cartilage/fat).

- Discard bones/skin (or reserve for secondary stock — see below).

- Roughly chop/shred meat pile to avoid long strings (easier eating).

- Return meat to pot anytime before serving (fully cooked).

Step 5: Final Seasoning & Serving

- Taste/adjust salt (large pot needs more than expected).

- Add turmeric for golden color, subtle flavor, and health benefits (common in commercial products).

- Optional: Dry noodles (add sparingly — they expand greatly).

- Last-minute: Fresh herbs (celery leaves, parsley) and acid (lemon juice/vinegar per bowl for brightness).

- Result: Rich, golden, vegetable-heavy soup — delicious hot or cold from fridge.

Bonus: Second-Stock Stew (Ultra-Frugal)

- Roast reserved bones/skin to brown.

- Simmer 2 hours for concentrated (though less fresh) stock.

- Add whole grains (e.g., farro), vegetables, butter, herbs → hearty stew.

Key Principles

- Stock elevates inexpensive/ abundant vegetables into "fantastic" meal.

- Whole chicken + veggies = sustainable, nutritious, budget-friendly (feeds one person all week).

- Flexibility: Adapt flavors (e.g., Asian with lemongrass/ginger/chili/fish sauce).

- No fancy techniques needed — basic simmering yields professional results.

This method turns minimal effort and cost into versatile, healthy meals — perfect for batch cooking.

(~1,100 words • Approx. 8–10 minute read)

Exploring the Remote Oklahoma Panhandle: Tiny Towns in Cimarron County

A road trip vlog ventures into Cimarron County, Oklahoma's westernmost and least-populous county (~2,300 residents total; only U.S. county bordering four other states: Colorado, Kansas, New Mexico, Texas). The area features vast emptiness, silence, and declining small towns amid flat prairies and agriculture.

Kenton: Near-Ghost Town in the Northwest Corner

- Population: ~17–31 (2020–2025 estimates vary; very small CDP).

- Features: Post office, two well-maintained churches (Baptist and Methodist), closed museum with old carriage (~mid-1800s), abandoned/quiet streets, some occupied homes.

- Highlights: Extreme isolation (nearest major city hours away), silence, old log cabin-like structures.

- Vlogger notes "ghost town" feel but signs of minimal life.

Felt: Small but Youthful Community

- Population: ~98–109.

- Demographics: Young median age (~20–21), ~57–73% White, ~43% Hispanic.

- Features: Surprisingly nice school (Felt Bulldogs), a few streets, some abandonment.

- Economy: Median income ~$68,750 (solid for area); higher child poverty.

- Vlogger surprised by school in such small town.

Boise City: County Seat and "Largest" Town

- Population: ~1,100–1,200 (declining from 1970 peak ~2,000).

- Key sights: 1926 Classical Revival courthouse (bombed accidentally by U.S. B-17 in 1943 practice run – minimal damage, no injuries), dinosaur art piece ("Cimi the Cimarronassaurus"), heritage center with old wagons/bombs, quiet downtown with caboose chamber, some abandoned buildings.

- Fun facts: Pronounced "Boyce"; bombed in WWII mishap; low crime; cost of living ~24% below U.S. average; median home ~$65k–73k.

- Demographics: ~50% White, 40% Hispanic; median income ~$49k.

Keyes: Older Town with Hidden Wealth

- Population: ~252–276 (peak 1960 ~627).

- Features: Abandoned downtown (old theater, gas station for sale ~$13k, deserted buildings), grain elevators, post office, no bank/school kids.

- Demographics: Median age ~63 (73% over 50); ~95% White.

- Economy: Surprisingly high median income ~$118k+ (helium production plant – high-paying jobs ~$151k); very low poverty (~2%).

- Vlogger notes quiet/abandoned feel despite wealth; old vehicles/treasures.

The vlog captures the panhandle's profound isolation, declining populations, low services (long drives for basics), but resilient quirks like historic sites and unexpected economies (helium in Keyes). Rain interrupts at end; teases Texas panhandle next.

(~1,200 words • Approx. 9–11 minute read)

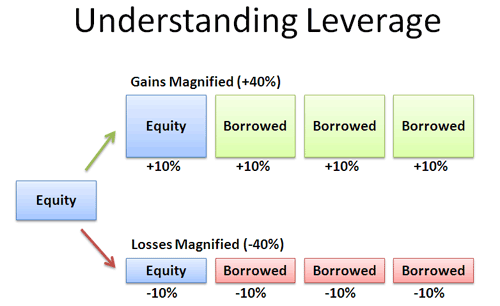

Charlie Munger's Unfashionable Rule: Staying Rich by Avoiding Ruin

A reflective video explores Charlie Munger's (Warren Buffett's partner, died 2023) counterintuitive philosophy: Making money is easy; keeping and compounding it is hard and rare. Most fortunes are lost, not gained — lottery winners bankrupt, athletes broke, even geniuses ruined. Munger inverted the question: Instead of "How to get rich?" ask "How to avoid poverty?"

Core rule: "The first rule of compounding is to never interrupt it unnecessarily." Survival > brilliance. Avoid big losses that halt exponential growth.

Avoiding Stupidity > Seeking Brilliance

Munger prioritized minimizing irreversible downside over maximizing upside. Real risk = permanent ruin (forced selling, irrecoverable capital), not volatility.

- Losses asymmetric: -50% needs +100% recovery; -90% needs +900%.

- Leverage/debt lethal — creates fragility, margin calls ignore long-term value.

Historical examples:

- Ancient Rome: Overextended elites ruined by debt/political shifts.

- 1929 Crash: Many right long-term but leveraged; forced sales at bottom wiped them out. Cash holders bought cheap.

- 1998 LTCM Collapse: Nobel-winning economists' hedge fund, highly leveraged, lost ~$4.6B in months (Russia default triggered). Bailed out to prevent systemic crisis — brilliance undone by fragility.

Human Biases: Why Smart People Self-Destruct

Brains wired for short-term survival, not modern finance:

- Greed/Social Proof: "Everyone's winning" disguises as opportunity.

- Overconfidence: Early luck mistaken for skill.

- Envy: FOMO drives chasing.

- Loss Aversion: Panic selling stops pain but guarantees loss.

- Illusion of Control: "I'll exit in time" — markets don't allow.

Munger designed around emotions: Assume failure, build unbreakable structures (no leverage, simple investments).

The Math of Survival: Compounding's Fragility

Exponential growth hates interruptions.

- Investor A: 20% average but occasional -60% → underperforms.

- Investor B: Steady 10% no big losses → compounds to far more over decades.

- "Big money in waiting," not trading.

Avoiding ruin enhances upside (buy during others' panic).

Inversion: Study Failure Patterns

Common ruin paths:

- Excessive leverage.

- Timing-dependent bets.

- Complexity beyond understanding.

- Misaligned incentives.

- Envy-driven chasing.

- No margin of safety.

Invert to rules: Low/no debt, robust strategies, circle of competence, buffers.

Personal Restraint: The "Day Nothing Happened"

Vignette: Tempted by hot trade amid hype — Munger's voice: Restraint wins. Did nothing; trade later collapsed. Boredom = survival price.

The Ultimate Advantage: Endurance

Wealth from time + survival, not speed. Munger's edge: Humility, patience, robustness over precision.

Final truth: Never risk what you have/need for what you want/don't need. Protect downside; time handles upside. Staying rich = refusing self-destruction while others chase excitement.

(~1,250 words • Approx. 9–11 minute read)

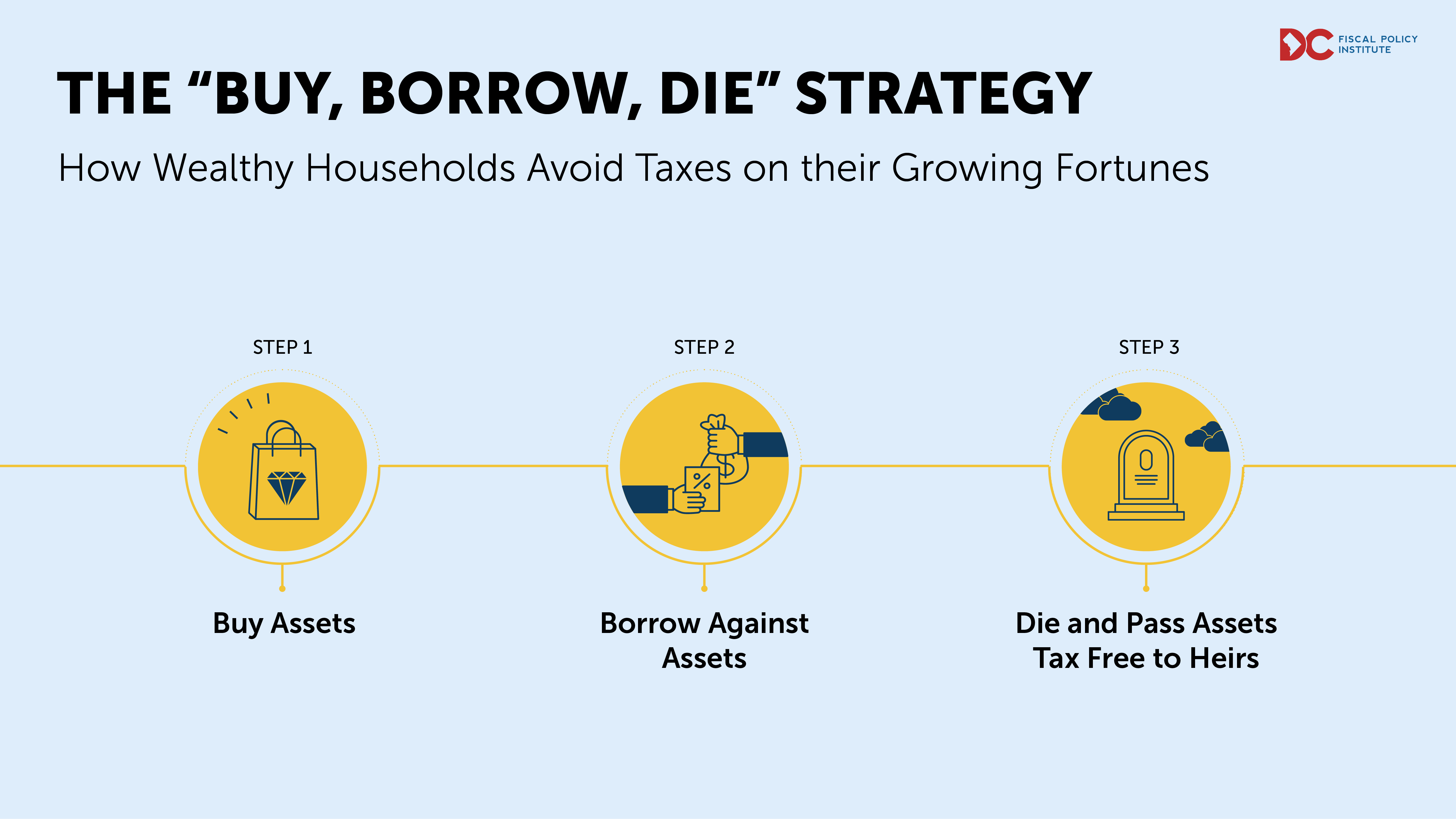

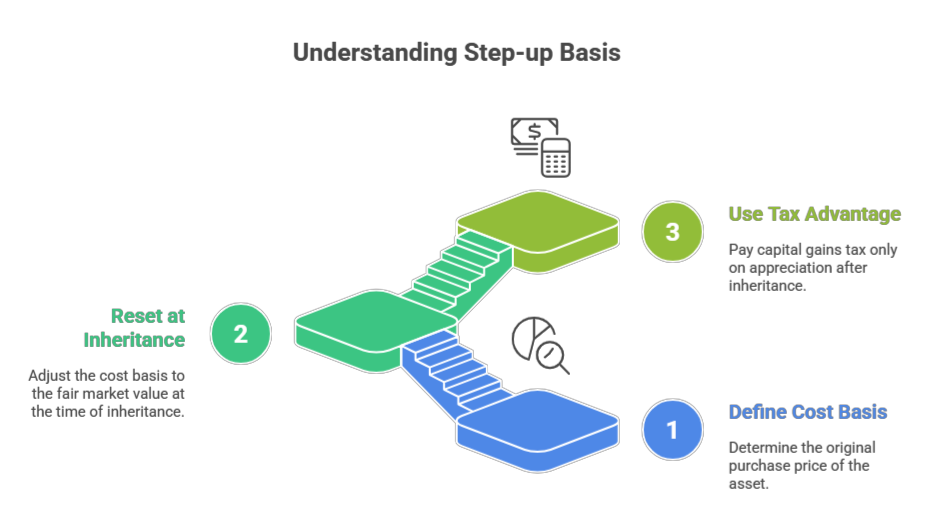

"Buy, Borrow, Die": The Legal Tax Strategy That Lets the Ultra-Wealthy Pay Almost Nothing

A provocative video exposes "Buy, Borrow, Die" — a century-old, fully legal U.S. tax code strategy allowing the wealthy to minimize or avoid income and capital gains taxes while building/preserving dynastic wealth. Coined in the 1990s by USC law professor Edward McCaffery to highlight inequality, it gained prominence via ProPublica's 2021 investigation (leaked IRS data showing America's 25 richest paid ~3.4% effective tax on wealth growth 2014–2018).

Requires significant wealth (typically $1M+ portfolio for access); not for average earners.

Phase 1: Buy – Tax-Deferred Appreciation

Wealthy prioritize appreciating assets with low/no current income: growth stocks (no dividends), real estate, art, private shares.

- Unrealized gains untaxed indefinitely (no sale = no capital gains trigger).

- Contrast: Wage earners taxed immediately (income, payroll taxes).

Assets compound quietly; IRS can't touch paper gains.

Phase 2: Borrow – Tax-Free Liquidity

Use assets as collateral for securities-based lines of credit (SBLOCs) from banks/private wealth firms.

- Borrowed funds not income → completely tax-free.

- Rates often low (2–6.5%, tied to benchmarks); lend 50–90% of portfolio value.

- Assets continue appreciating (e.g., 7–8% historical returns beat borrowing costs).

- Cycle: Growing collateral → more borrowing power.

Live lavishly (homes, travel, investments) without taxable events.

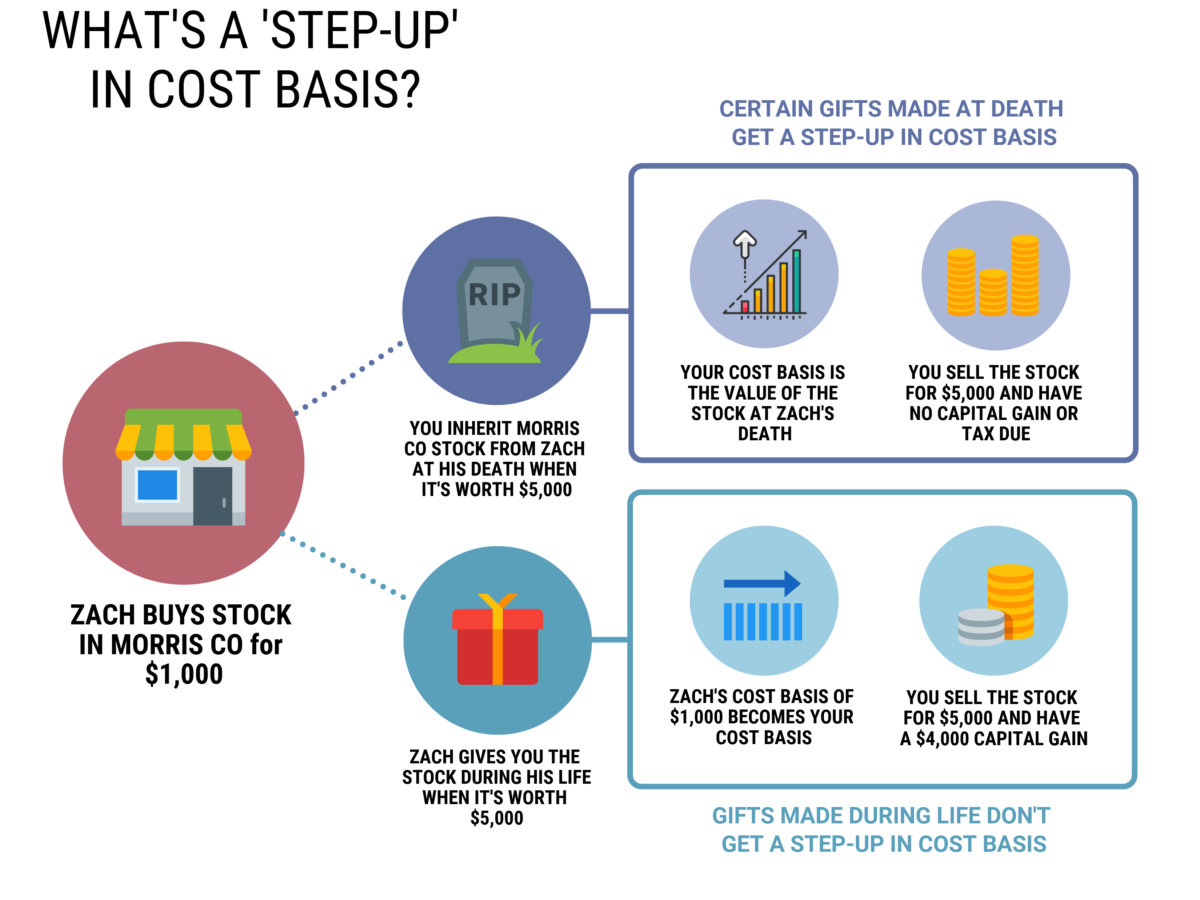

Phase 3: Die – Tax Reset for Heirs

At death, heirs inherit via stepped-up basis (current law, 2025): Basis resets to fair market value.

- Decades of gains erased for tax purposes.

- Heirs sell to repay loans → zero capital gains on pre-death appreciation.

- Remaining assets: Tax-free inheritance; cycle restarts.

Perpetuates generational wealth.

Hypothetical Example: $1M → Multi-Generational Wealth

- Start: $1M in growth assets.

- 30 years @7–8% compound → ~$8M.

- Borrow millions tax-free along way (live richly; interest < returns).

- Death: Heirs get stepped-up basis; sell portion tax-free to clear debt → inherit ~$4M+ untouched.

Zero effective tax on gains/lifestyle.

Scale & Implications

- SBLOC industry boomed; banks target high-net-worth ($1M–$10M+ minimums).

- Scales with wealth: Billionaires borrow billions tax-free.

- Contributes to inequality: Unrealized gains untaxed; reduces asset supply → potential price inflation.

- Political blind spot: Rate hikes irrelevant if no realization.

Strategy legal/exploits design (not loopholes); highlights earned vs. investment income disparity. Reforms debated (e.g., tax unrealized gains, limit step-up) but unchanged as of 2025.

(~1,200 words • Approx. 9–11 minute read)

China's Record $1 Trillion Trade Surplus: Triumph or Symptom of Deeper Problems?

In late 2025, China achieved a historic milestone: a goods trade surplus exceeding $1 trillion in the first 11 months (reaching ~$1.08 trillion, surpassing the full-year 2024 record of ~$992 billion). Official data showed strong November exports (~5–6% YoY growth) offsetting weaker imports, pushing the annual figure toward $1.2–1.3 trillion projections.

State media and nationalists celebrated it as proof of resilience amid US tariffs (average ~47.5% on Chinese goods). However, a critical analysis argues this surplus signals economic weakness, not strength — driven by domestic failures forcing export reliance.

1. Collapsing Imports: Sign of Consumer Weakness

Surplus grew mainly from declining imports (down ~0.9–1.6% YoY in periods), not explosive export growth.

- Chinese households, facing job fears, property crisis, and low confidence, cut spending on foreign goods (e.g., luxury, travel, imported brands).

- Healthy economies import more as citizens prosper; China's trend shows "self-inflicted poverty" — people sacrificing quality of life, hoarding cash.

Analogy: A worker skipping meals/travel to save money looks "rich" in savings but lives poorly — not enviable prosperity.

2. No Consumer Confidence = Stagnant Domestic Demand

Flat/declining imports reflect fearful households unwilling to spend/upgrade lives.

- No boom in foreign cars, tech, or tourism.

- Beijing's stimulus fails to ignite internal consumption; exports become the only GDP driver.

This is a "clearance sale" economy: Flooding world with goods because locals can't/won't buy.

3. Dangerous Dependence on Antagonized Foreign Markets

China now more reliant on exports (propping ~40% of growth) while provoking key partners (US, EU, Japan, India, ASEAN) via trade weaponization, dumping, and nationalism.

- Boycotts (e.g., Japanese goods) hurt Chinese consumers more than targets.

- Risky strategy: Like insulting your main customers while depending on them.

Despite US tariffs slashing bilateral exports (~18–29% drops), China rerouted to Europe/Africa/ASEAN — flooding markets, sparking backlash (e.g., EU probes, Macron threats).

4. Persistent Surpluses Enabled by Currency Manipulation

Large ongoing surpluses require undervalued yuan and capital controls (mercantilism-style).

- Free-floating currency would appreciate, boosting imports/reducing surplus.

- Beijing suppresses wages/domestic demand to maintain export edge — not modern innovation.

5. Overcapacity and Subsidized Dumping

Exports surge from industrial overproduction: Steel, EVs, solar unable to sell domestically due to weak demand.

- State subsidies enable global dumping → addiction to being "world's sweatshop" (pollution, low wages).

- Not demand-driven success; forced exports to avoid layoffs.

6. Flat Forex Reserves: Hidden Capital Flight

Despite massive inflow from exports, reserves stable (~$3.34–3.35 trillion, minor fluctuations).

- Indicates outflows: Capital fleeing via overseas investments, Belt & Road, or evasion.

- Surplus money enters via trade but exits quietly — not building real wealth reserves.

Overall Verdict: An "Autopsy Report"

The $1 trillion surplus masks failures: Unable to boost domestic demand, over-reliant on exports, provoking trade wars, manipulating systems.

- Exports "pain" abroad while consumers suffer at home.

- Unsustainable: Risks global backlash, protectionism.

Critics note positives (manufacturing scale, diversification success despite tariffs) and imbalances (e.g., US/EU services surpluses with China). But the video frames it as desperation in nationalist clothing — a broken engine "flooring the gas."

(~1,150 words • Approx. 9–10 minute read)

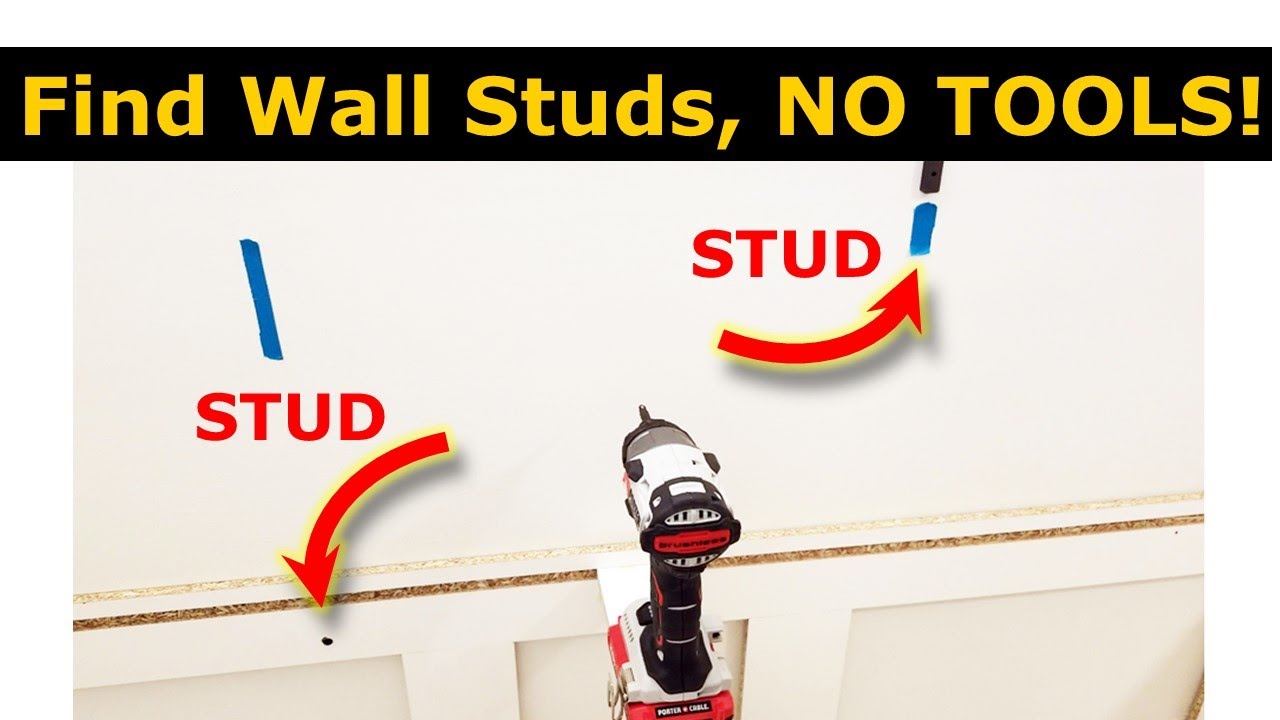

Finding Wall Studs Without (or With Minimal) Tools: Practical Tricks from a Craftsman

In a hands-on tutorial from Essential Craftsman, an experienced builder shares reliable, low-tech methods to locate studs behind drywall when your electronic stud finder fails or isn't available. The focus is on minimizing damage (especially in others' homes) and using everyday items. He ends by recommending his favorite modern tool.

Preparation: Minimize Visible Damage

- Use painter's tape as a "palette" for marks (easy removal, no paint touch-up needed).

- Work carefully — you're responsible for holes, even in your own home.

Method 1: Electrical Outlets/Switches

- Outlets almost always attach to a stud on one side (~99% chance).

- Remove cover plate; gently probe with pocket knife or thin tool to feel for wood.

Method 2: Knocking/Tapping

- Tap wall with knuckle or hammer handle: Hollow sound = no stud; dull/thud = stud.

- More reliable with tool than knuckle.

Method 3: Baseboards or Trim

- Baseboards often nailed into bottom plate (or studs if tall).

- Probe nail holes/joints at base; measure up (studs typically 16" on center).

- Small holes hide easily under caulk/paint.

Method 4: Verify Vertical Alignment

- Studs may not run perfectly straight.

- Use level to transfer known lower stud position upward accurately.

Method 5: Exploratory Holes (Minimal & Fixable)

- Use thin finish nail or small drill bit to probe.

- Patch with white toothpaste (on textured/white walls — blends invisibly; wipe excess).

Bonus Toothpaste Trick for Hanging Pictures

- Dab toothpaste on hanger points.

- Press frame against wall (transfers exact marks).

- Nail/screw; wipe off toothpaste (blue shows better).

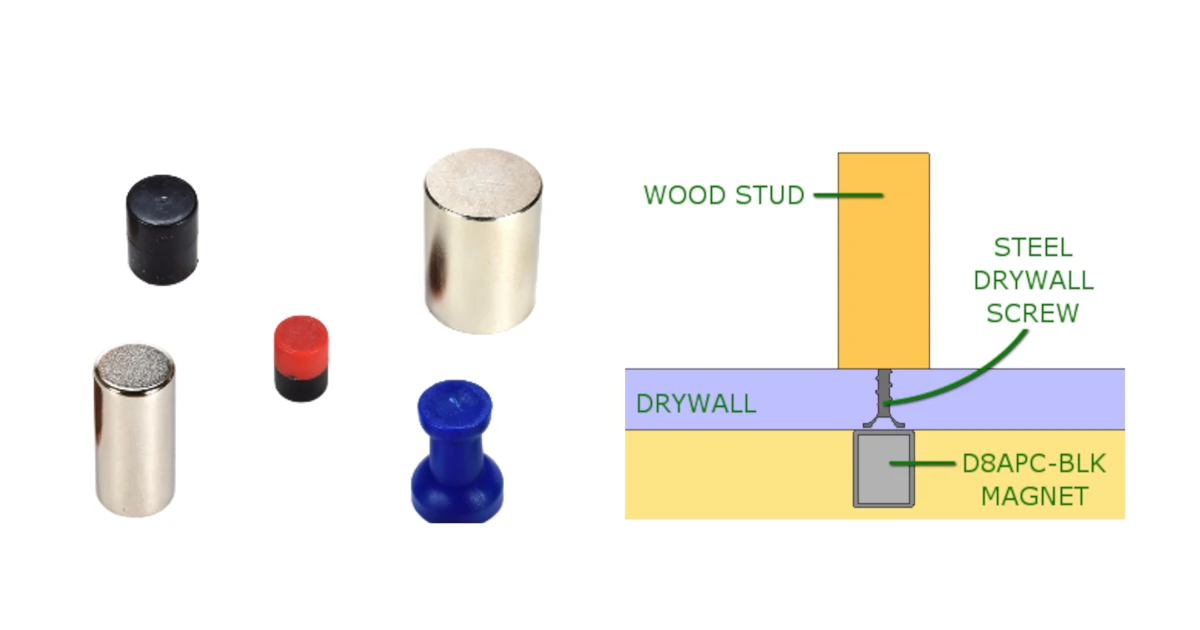

Method 6: Magnets for Screws/Nails

- Strong/rare-earth magnet detects drywall screws (often on 16" centers).

Method 7: Exterior Siding (Wood/Vinyl Homes)

- Nails often visible outside → mark stud locations.

- Transfer inside via window/door reference points (account for wall thickness).

Recommended Tool: Franklin Sensors Stud Finder

- Presenter's favorite: Multi-sensor design (e.g., ProSensor models with 13+ sensors) lights up entire stud width instantly — no calibration, accurate/deep scanning (up to 1.5–1.7").

- Praised in 2025 reviews for reliability on thick/plaster walls; wide LED array shows edges/center.

Notes for Older Homes

- Lath/plaster or horsehair walls challenging — magnets/exterior often best.

Emphasis: Go slow, confirm multiple ways — prevents damage and ensures secure hanging.

(~1,200 words • Approx. 9–11 minute read)

The Biggest Retirement Mistake: Underspending Due to Fear (And How to Fix It)

Many retirees with substantial savings (e.g., $2–3 million) live frugally out of fear of running out of money, missing out on enjoyable experiences. The real issue isn't lack of funds but lacking a systematic "retirement paycheck" — a plan to safely convert nest egg into reliable income.

Financial advisor Josh (from a retirement-focused firm with 500+ clients) shares a five-step framework used by confident retirees who spend freely without worry.

Step 1: Calculate Exact Expenses (Including Hidden Taxes)

Most underestimate spending — "I think $6k/month" often becomes $8.5k+ when reviewing statements.

- Review 3 months' bank/credit card bills → average monthly "burn rate."

- Add taxes: Retirement withdrawals (especially IRA/401k) are taxable; no automatic withholding.

- Example: $7k expenses → $84k/year withdrawals → ~$16k taxes → true need $8.3k/month.

- Subtract guaranteed income (Social Security, pensions) → annual/monthly "gap" portfolio must fill.

Iterate later as sources clarify taxes.

Step 2: Strategic Withdrawal Sources (Tax Optimization)

Not all accounts equal:

- Tax-deferred (IRA/401k): Withdrawals ordinary income (higher rates).

- Taxable brokerage: Gains at lower capital gains rates.

- Roth: Tax-free.

Mistake: Random/IRA-only pulls → higher brackets.

- Blend to stay in favorable brackets (e.g., 22–24%; avoid 32% jump).

- Example (Tom, $2.5M total): IRA-only → 32% bracket; blended → 22% + 15% gains → $8k/year saved ($240k over 30 years).

- Dynamic: Adjust yearly (Roth conversions, Social Security start).

Step 3: Build Foundation (Cash + Allocation)

- Cash reserve: 12–18 months expenses in high-yield savings/money market.

- Protects during downturns — avoid selling low.

- Example: 2020 retiree used cash cushion; portfolio recovered untouched.

- Portfolio: Shift from accumulation (growth-heavy) to balanced.

- 50–75% stocks for inflation protection; rest bonds/cash.

- Diversify (US/international, small/large, value/growth, REITs) for smoother returns.

Step 4: Guardrails for Dynamic Adjustments

Fixed withdrawals risky — markets fluctuate.

- Set initial rate (e.g., 5% on $2M = $100k/year).

- Capital preservation guardrail: If rate >20% above initial (e.g., 6%), cut 10% spending.

- Prosperity guardrail: If <20% below (e.g., 4%), increase 10%.

- Provides "pulse check" — confidence when healthy; protects in downturns.

Step 5: Stay Flexible — Annual Reviews

Retirement evolves:

- Early: Higher spending (travel, renovations).

- Mid: Social Security reduces withdrawals; tax shifts.

- Later: Lower travel but rising healthcare.

Most clients adjust yearly — only one in hundreds kept fixed amount decade-long.

Outcome: Confidence Over Fear

Follow framework → clear "paycheck," tax efficiency, downside protection.

- Enjoy life (trips, family) without guilt/second-guessing.

- Shift from saver to strategic spender.

(~1,250 words • Approx. 9–11 minute read)

Surviving Cold Nights Sleeping in a Car: Practical Strategies for Western Washington Winters

A vlog from someone living/sleeping in their car in temperate but occasionally cold Western Washington shares a simple, effective routine for handling nights dropping to ~15°F (with light snow). The approach relies on the car's built-in heater for initial warmup, heavy insulation, and body heat retention — no separate heaters needed.

Evening Routine: Warm-Up Phase

- Start engine immediately after work; set heat high (~75°F).

- Eat supper while idling (wastes fuel/wears engine slightly but infrequent in mild climate).

- Keep snowy/wet boots in front (avoid back-seat moisture).

Transition to Back Seat

- Climb carefully (manual transmission — avoid gear grinding).

- Run engine longer to warm rear/sleeping bag (6lb insulation takes time).

Core Insulation Strategy

- -15°F rated sleeping bag + full cold-weather clothing (blizzard gear) for excellent warmth.

- Window covers (reflectix/insulation) retain heat; car interior stays above freezing (water unfrozen morning).

Moisture Management

- Daily window wipe-down handles condensation (cold causes fogging).

- Avoids propane heaters (add significant moisture, worsening issue).

Electronics Protection

- Sleep with phone/tablet/camera nearby (body heat prevents freezing).

- Power station okay to cool (no nighttime discharge; lithium-ion safe if not used frozen — avoids plating/damage).

Morning Outcome

- Slept comfortably; no freezing issues (water liquid, interior warm).

- Experiment success at 15°F with snow.

Why No Separate Heater?

- Electric: Limited plug access.

- Propane: High moisture output (combustion byproduct).

Additional Notes

- Idling occasional/minimal wear in mild area.

- Car holds heat well with covers.

- Scalable for colder climates with better gear.

This low-cost, reliable method suits occasional cold snaps — emphasizes insulation over constant heating.

(~1,100 words • Approx. 8–10 minute read)

Why the First $100,000 in Net Worth Is the Hardest (And Why It Changes Everything)

Many Americans earn over $1 million lifetime yet struggle to reach $100,000 net worth, even with solid careers. Recent data (Federal Reserve 2022 SCF, updated 2025 analyses) shows medians low: ~$7k–$50k (20s–30s), ~$60k–$200k (40s–50s) — far below averages skewed by wealthy outliers.

The key insight: First $100k requires pure discipline (saving/investing aggressively). After that, compound growth accelerates — "snowball" effect makes subsequent hundreds easier.

The Four Traps Keeping Most Below $100k

- Lifestyle Creep Income rises → spending rises to match (or exceed). "Feeling rich" (nice car/apartment) ≠ being rich (assets). Live below means → wealth builds; scale lifestyle to income → treadmill.

- Payments Mentality & Debt Culture Big purchases framed as "affordable monthly" hide total cost (e.g., $30k car → $35k+ with interest). Credit cards, BNPL, loans keep money "spoken for" — depreciating items drain net worth.

- Late/No Investing

Delaying compounds lost time. Example (~7–8% historical returns):

- $200/month from age 22 → ~$100k+ by late 30s.

- Start at 32 → half as much.

- Later starts barely move needle. Savings accounts (4–5%) too slow; index funds essential.

- Buying Liabilities, Not Assets Middle-class: Cars, phones, clothes (depreciate). Wealthy: Stocks, funds, REITs (appreciate/pay dividends). Assets eventually "buy things" (cover lifestyle).

Why $100k Is the "Wealth Threshold"

- At $100k invested (~8% return) → ~$8k/year growth (~$700/month) — money works noticeably.

- Snowball: Next $100k faster (compounds on larger base).

Example ($10k/year saved + 7% return):

- 0–$100k: ~9–10 years.

- $100k–$200k: ~5–6 years.

- Accelerates further.

Charlie Munger: "First $100k a b*tch, but then compounds heavily."

Roadmap to $100k Faster

- Eliminate high-interest debt (>7%) — guaranteed "return."

- $10k–$20k emergency fund (high-yield savings).

- Automate investing ($500+/month into low-cost index funds/S&P 500 ETF).

- Live at 50% income temporarily — maximize gap.

Formula: Higher income + savings rate + time + compounding = wealth. Gap (earn – spend) + early investing key — not salary alone.

Crossing $100k shifts from grind to momentum — boring discipline pays off exponentially.

(~1,200 words • Approx. 9–11 minute read)

7 Signs You're Financially Ahead of the Average American

A motivational video highlights sobering U.S. financial statistics (2024–2025 data) to show that many basic habits place you far ahead of most people. Social media distorts perceptions (luxury seems normal), but averages reveal widespread struggles — low savings, high debt, paycheck-to-paycheck living.

The goal: Encourage those doing well and motivate others, while stressing financial literacy (only ~37–50% of adults grasp basics).

1. You Have an Emergency Fund (3–6 Months Expenses)

- Ideal buffer against job loss/unexpected costs.

- Reality: ~59–67% live paycheck-to-paycheck (2025 surveys vary; up from prior years).

- ~59% can't cover $1,000 emergency from savings (lowest since 2021).

- ~21–40% have no/little emergency fund.

- Even 1–2 months saved beats majority (~65% risk debt for emergencies).

2. You Have Any Savings at All

- One-third (~33%) have zero savings; ~50% less than $1,000.

- Personal savings rate ~3.8–4.4% (near lows; down from 10% historical).

- Inflation erodes purchasing power, but low savings signals vulnerability.

- Any amount (even modest) ahead of half the population.

3. You Have Retirement Savings

- ~20–28% of adults (higher for 50+) have zero retirement savings.

- Average ~$88k–$333k (medians lower ~$87k–$200k, skewed by wealthy).

- If saving anything (especially 15%+ salary), in top ~75%.

- Aim higher for comfort; balances vary widely by age.

Additional Context from Video (Partial List)

Video covers 7 signs but cuts off; implied others include avoiding debt, investing consistently, financial knowledge.

Key takeaway: These "basic" steps (emergency fund, savings, retirement contributions) outperform most Americans amid rising costs/debt. Improve literacy to break cycles — small habits compound into security.

(~1,100 words • Approx. 8–10 minute read)

13 Ways to Build Wealth in 2026: Leveraging AI, Attention, and Digital Trends

A motivational 2026 outlook video claims the year offers unprecedented opportunities for wealth creation through technology (especially AI), platforms, and mindset shifts. It dismisses traditional slow grinds, urging viewers to "write new rules" via leverage — systems, tools, and networks multiplying effort.

The presenter lists 13 ways (teasing the 11th as a "golden ticket"), with examples of rapid success. Core theme: Leverage over labor — poor trade time for money; rich trade ideas for scale.

1. Mastering AI Leverage

Build automated "money machines": Faceless YouTube (AI-edited/videos), AI-run e-commerce (chatbots for sales/marketing).

- Example: Singapore entrepreneur runs 6 stores remotely via AI.

- 2026 edge: Command AI for automation (copy, design, service) → multiply self without teams.

2. Owning the Algorithm (Attention = Gold)

Master hooks (first 3 seconds), emotions, shares on TikTok/YouTube/Instagram/X.

- Viral potential: One video → millions views, high earnings.

- Example: Italian girl reviews AI app → 5M views, doctor-level monthly income.

- Algorithms reward energy/emotion over perfection.

3. Micro-Brands (Niche Domination)

Laser-focused businesses for passionate tribes (e.g., luxury pet accessories, gamer snacks).

- Low competition; own community completely.

- Tools: AI, print-on-demand, logistics → solo global brand.

- Example: Toronto minimalist skincare → 50k orders fast.

4. Digital Real Estate

Own attention assets: Channels, newsletters, lists, sites.

- Monetize/flip like property (ads, subs, sales).

- Example: Refresh old channels with AI → double value.

5. Reselling Data

Collect/anonymize trends (extensions, browsers) → sell to marketers/AI firms.

- Quiet, scalable middleman role.

6. Micro-Education (Teaching Skills)

Package expertise into courses (platforms like Kajabi).

- Demand for shortcuts from real practitioners.

- Example: Notion organization course → $80k/month.

7. Investing in Chaos

Buy dips during volatility (crashes, disruptions).

- Courage rewarded when others panic.

8. AI-Generated Creativity

Prompt tools for art, music, books, scripts → sell on marketplaces.

- Direction over talent.

- Example: Brazil AI comic → $40k/month.

9. Community Building

Create tribes (Discord/Telegram) → ecosystems (memberships, events).

- Trust → loyal customers.

10. Partner Leverage

Collaborate (vision + execution + audience) → exponential scale.

- Networks over solo.

11. Subscription Wealth ("Golden Ticket")

Recurring models: Memberships, tools, content.

- Predictable, compounding income (e.g., 1k @ $20/month → $20k passive).

12. Personal Brand Power

Build trust/connection → attract opportunities.

- 1k loyal > 100k strangers.

13. Self-Investment (Mindset)

Adapt/learn fastest; persistence + preparation = "luck."

Overall: Pick one, go all-in. 2026 favors builders using leverage — start now for momentum.

(~1,150 words • Approx. 9–10 minute read)

Rice and Beans: The Ultimate Budget-Friendly, Nutritious Meal Hack

In a comforting, practical cooking tutorial, the creator demonstrates how rice and beans — often overlooked sides — can become hearty, flavorful main dishes feeding a family cheaply and nutritiously. Using 1 lb each of long-grain rice and dried black beans (plus affordable veggies/onions/garlic), the recipes yield massive portions with "main character energy" — customizable, forgiving, and far superior to canned versions.

Emphasis: Use what's on sale/available (no perfection needed); adaptations (jarred garlic, frozen veggies, no-soak beans) keep it accessible. Total cost low; prep simple but beans take time (hands-off simmering).

Mexican-Style Red Rice (Arroz Rojo) – Feeds a Crowd

Ingredients (flexible):

- 1 lb long-grain rice.

- 1 onion (any type), roughly chopped.

- 4+ garlic cloves, crushed/chopped.

- 1–2 carrots, diced (adds sweetness/volume; frozen OK).

- Half 15-oz can corn (or smaller can).

- 8-oz can tomato sauce (or blended tomatoes).

- 3–4 cups chicken broth (adjust for fluffy/sticky texture).

- 1 tbsp chicken bouillon powder.

- Cilantro sprigs (for steaming).

- Oil, salt.

Steps:

- Rinse rice thoroughly (4–5 times until clear) to remove starch/dust.

- Sauté onion/garlic in oil (~10 min, medium-low) until soft/translucent; salt.

- Add rinsed rice; toast to light golden (~5–10 min).

- Stir in tomato sauce.

- Add broth/bouillon; top with carrots/corn/cilantro (no stirring).

- Bring to low simmer; cover, cook untouched 20 min.

- Fluff with fork; remove cilantro; mix veggies.

Result: Vibrant, fluffy red rice — sweet from veggies, umami from bouillon. Hides carrots well (kid-friendly); optional peas.

Simple Black Beans (Frijoles Negros) – Better & Cheaper Than Canned

Ingredients:

- 1 lb dried black beans.

- 1 onion (halved for boiling, half diced for sofrito).

- Garlic (halved for boiling, chopped for sofrito).

- 1 green bell pepper, diced.

- 1 jalapeño (optional, diced).

- Spices: 1 tbsp bouillon, 1½ tbsp cumin, 2 tbsp oregano.

- Bay leaves, cilantro sprigs.

- Oil, salt/pepper.

Steps:

- Sort/rinse beans (remove odd ones/rocks); no pre-soak needed.

- Cover with water (+2–3 inches); add halved onion/garlic/bay leaves/cilantro.

- Boil then low simmer (covered) ~1–2+ hours; check water level every 20 min (keep beans submerged); stir gently.

- Beans done when easily smashable.

- Sofrito: Sauté diced onion/pepper/jalapeño/garlic (~5–7 min); add spices.

- Transfer cooked beans (slotted spoon) to sofrito; add bean liquid gradually, simmer/reduce to thick sauce (gentle stirring — keep whole).

- Season salt/pepper.

Result: Creamy, flavorful whole beans — far tastier than canned; thick sauce from starch.

Key Tips & Philosophy

- Flexibility: Swap veggies (frozen/whatever's cheap); add meat (chicken/sausage/hot dogs); adjust spice.

- No shame: Jarred garlic, canned shortcuts OK — goal is feeding family deliciously/affordably.

- Budget/Health: Bulk dried beans/rice cheap/nutritious; veggies add volume without cost.

- Customization: Fluffier rice (less broth); spicier beans (more jalapeño).

These transform "slept-on" staples into satisfying mains — proof tough times don't mean bland/hungry eating.

(~1,100 words • Approx. 8–10 minute read)

Gemini AI summaries:

🤫 The CIA Tactic to Control Any Room Without Speaking

The core message of this tactic, reportedly taught by the CIA, is that control is established before and immediately upon entering a room, not during the conversation. It centers on replacing the common tendency toward reactive framing with a deliberate, powerful active frame.

Here is a summary of the powerful three-part tactic:

1. Preload Your Active Frame (Before Entering)

Taking control starts by consciously establishing a frame that is distinct from and in competition with the existing dynamic in the room.

Avoid Subordination: Most people subconsciously subordinate themselves by trying to fit in (using the same language, dress, timing, etc.). This is following the group's or someone else's existing frame.

Create Your Own Frame: You must arrive with a clear, active, and deliberate frame—an outcome, a plan, and a desire.

Control the Logistics: The most powerful, subtle way to establish this frame is by already knowing and often controlling the logistics:

The Time you are going to meet.

The Place where you are going to meet.

The End Time of the event, date, or meeting.

Knowing the end time, even if others don't, signals leadership and a clear structure. Subconsciously, people recognize you are the one with the plan and will follow your tempo.

2. Sustain the Frame for Survivability (In the Room)

Once inside the room, your frame must be extremely consistent and stable. People are drawn to stability because sustainability equals survivability, and security is a fundamental human need.

Be the Stable "Four-Legged Table": People will choose a stable, consistent structure over one that is attractive but unstable (like a heavy marble table on three legs).

Counterintuitive Dominance: Talk the Least: The person who talks the least controls the room because they absorb all information (verbal and non-verbal cues). Conserving energy allows you to remain stable while others expend theirs fighting for dominance.

Speak in Statements, Not Questions:

Questions force others to process the question, formulate multiple answers, and then decide on a filtered response—it takes effort and can introduce friction.

Statements offer finality, certainty, and are easy for the brain to process quickly. The listener only has to internally agree or disagree, making your speech the most stable and attractive anchor point in the conversation.

3. Let Competing Frames Collapse (The Inevitable Outcome)

Frames are dynamic and constantly in competition. You do not need to fight to win.

The Winner is the Most Stable: By executing steps one and two—pre-loading an intentional frame and maintaining its quiet stability (speaking in infrequent statements)—you become the strongest competitor.

Gravitas as a Safe Haven: While other reactive and unstable frames compete, fight, and collapse (running out of energy or killing each other), you remain unchanged, quiet, and sturdy. This consistency makes you the safe haven that everybody naturally comes back to.

Gravitas Pulls People: Your quiet strength creates gravitas, pulling people to your frame subconsciously. You achieve your desired outcome without others even realizing they were following your lead.

The ultimate power is in controlling the silence and being the source of stability in a room full of noise and fear.

Commentary: basically, provide solutions to problems, and be useful, efficient, and reliable

💰 The Simple Four-Fund Portfolio That Beats the Pros

This strategy outlines a low-effort, high-return portfolio structure that has historically returned around 13% annually over the last decade. It requires zero stock picking and minimal ongoing attention, focusing on discipline and simplicity over complexity.

The structure is built around four key types of Exchange-Traded Funds (ETFs), designed to evolve with your age and financial goals.

Why Simplicity Works

Complexity Kills Returns: The average investor underperforms due to bad decisions (panic selling, chasing hype) rather than bad investments.

The Sweet Spot: A four-fund foundation is the ideal balance to capture broad market returns while maintaining a targeted edge.

Set It and Forget It: Once established, this portfolio requires potentially 10 minutes of attention per year.

The Four Funds Explained

1. The Foundation (40–50% Allocation)

This is your "sleep well at night" money, providing broad exposure to the US economy.

| Fund Purpose | Recommended Fund | What It Holds | Alternatives |

| Broad US Market Exposure | VOO (Vanguard S&P 500 ETF) | The 500 largest US companies (Apple, Microsoft, Nvidia, etc.) | VTI, SPY, IVV, SPLG, FXAIX, SWPPX |

| Key Takeaway | VOO and VTI are very similar. Pick one for simplicity and consistency. This fund anchors the portfolio and absorbs market volatility over the long term. |

2. The Growth Accelerator (15–25% Allocation)

This segment tilts the portfolio toward the world's highest-growth, innovation-driven companies, historically pushing returns above average.

| Fund Purpose | Recommended Fund | What It Holds | Alternatives |

| Technology/Innovation Tilt | QQQM (NASDAQ 100 ETF) | The top technology and innovation companies (AI, chips, cloud, digital economy leaders). | QQQ, SCHB, VGT, ARKK (high-risk alternative) |

| Key Takeaway | This creates intentional overlap with Fund #1, increasing exposure to the companies actively reshaping the world. Younger investors (under 40) can comfortably allocate 25% or more here. |

3. The Income Machine (10–40% Allocation)

This fund builds a "dividend snowball" that will eventually generate monthly income, turning the portfolio into a paycheck.

| Fund Purpose | Recommended Fund | What It Holds | Alternatives |

| Dividend Growth | SCHD (Schwab U.S. Dividend Equity ETF) | High-quality companies with strong cash flow and a history of paying and growing dividends. | DGRO, VYM, NOBL |

| Key Takeaway | Age dictates allocation. Your most powerful asset when young is time (for growth), not dividends. Start small (10–15% in your 20s/30s) and gradually increase the allocation as you near retirement (30–40%+ in your 50s/60s). |

4. The Personalized Sleeve / Wild Card (Max 15% Allocation)

This is the personal, customized slice that allows you to act on high-conviction ideas without risking the foundation. Never let this exceed 15% of your total portfolio.

| Goal | Recommended Funds/Assets |

| Real Estate Exposure | VNQ or SCHH (Real Estate Investment Trust ETFs) |

| High Monthly Income | JEPI, JEPQ, SPHY, QQQI (Covered Call/Income ETFs) |

| Crypto Exposure | IBIT or FBTC (Spot Bitcoin ETFs) |

| Speculative Belief | Individual stocks (1–2 high-conviction companies) |

| Hedge Against Volatility | Gold (e.g., in ETF form) |

| International Exposure | VXUS or IXUS (International Stocks) |

| Low Volatility/Cash Alternative | SGOV (Short-Term Treasury ETF) |

Portfolio Evolution by Age

The power of the strategy is in its flexibility—the structure remains, but the weightings shift from Growth to Income as you age.

| Age Group | Focus | Allocation Shift | Wild Card Selection |

| 20s–30s | Aggressive Growth | Heavy VOO/QQQM, Light SCHD | Bitcoin, Individual Stocks |

| 40s–50s | Balance & Building | Balancing VOO/QQQM and increasing SCHD | Real Estate, Gold, Income Funds |

| 50s–60s | Retirement Prep | More SCHD, Less QQQM | Income Funds, Real Estate, Gold |

| Retirement | Income Generation | High SCHD/Income funds, Lowest QQQM | Highest-yielding income funds (JEPI, etc.) |

🛡️ Your 30s: Defending the Financial Plan (Protecting Your Momentum)

The 30s represent a pivotal financial decade where "real life" arrives—marriage, children, mortgages, and increased financial risk. The focus shifts from merely building an investment engine (your 20s) to actively defending it against life's unpredictable challenges. The primary goal is to mitigate risk and prevent interruptions to the power of compounding.

The Challenge: Risk and Lifestyle Creep

Higher Financial Risk: Major life events (mortgage, children) increase both necessary expenses and financial exposure.

The Balancing Act: Many people struggle to balance current expenses against retirement savings, with inflation and rising costs being a major challenge.

Lifestyle Creep: As income rises, so does spending. The average 35-year-old household spending is up nearly 30% from a decade ago, often eroding savings progress.

The Threat to Momentum: An unexpected event (job loss, illness, bad insurance) can force you to pause investing or, worse, raid retirement accounts.

5 Essential Financial Moves for Your 30s

Your most powerful wealth move in this decade is to build a "shield" so your investments can run uninterrupted.

1. Lock in Your Safety Net (Insurance)

Term Life Insurance: If people depend on your income, secure a term policy (e.g., 20 years) aiming for coverage of roughly 10 times your annual income.

Disability Insurance: This is often a greater risk than death in your 30s (1 in 4 workers experiences a long-term disability before age 65). If you have a skilled profession, get "own occupation" disability coverage to truly protect your income if you cannot perform your specific job.

2. Keep Lifestyle Inflation in Check

The 50/50 Rule: When you receive a raise or bonus, automatically invest half of it and enjoy the other half guilt-free. This allows you to improve your current lifestyle while guaranteeing an increase in your savings rate.

3. Stay Diversified and Tax Smart

Savings Rate Goal: Maintain a high savings rate, generally aiming for 15% or more of your income.

Account Diversity: Start diversifying your savings across different tax buckets to give you flexibility in retirement:

Roth Accounts (tax-free withdrawals in retirement).

Pre-tax Accounts (401k/Traditional IRA, tax deduction now).

Traditional Brokerage Accounts (taxable but liquid).

Utilize an HSA (Health Savings Account) if available, as it offers triple tax advantages.

4. Eliminate Toxic Debt

High-Interest Debt: Make it a priority to eliminate any high-interest consumer debt (credit cards, personal loans) by your mid-30s. Every dollar saved in interest can be put to work compounding for you.

Student Loans: Aim to pay off student loans to free up significant monthly cash flow.

5. Build Your Plan B / Freedom Fund

Emergency Fund: Your first line of defense is having at least 6 months' worth of expenses set aside in a highly liquid, stable account (e.g., high-yield savings account or a short-term Treasury ETF like SGOV).

Protecting Momentum: This fund prevents you from hitting the pause button on investing or withdrawing from retirement accounts when an emergency strikes. It's also the "freedom fund" that allows you to take a sabbatical or invest in a new career opportunity.

The 30s Advantage

The key to your 30s is understanding that consistency in investing (e.g., bumping your 401k contribution from 10% to 15%) only works if you have the proper safeguards in place. By establishing insurance and a robust emergency fund, you ensure that life's inevitable challenges will not interrupt the compounding process—the true engine of long-term wealth.

📦 Weekend Hustle: Breaking Down Amazon Seasonal Driver Pay

This summary breaks down the experience and paychecks of a seasonal Amazon delivery driver working part-time on weekends as a second job, focusing on the financial strategy and the trade-offs involved.

💰 Paycheck Breakdown (Working 2 Days/Week)

The driver is a seasonal contractor for a Delivery Service Partner (DSP), not a direct Amazon employee, and is paid $26/hour regular rate, with overtime at $39/hour (time and a half).

| Paycheck | Total Hours Worked | Regular Hours/Pay | Overtime Hours/Pay | Take-Home Pay | Notes |