12/14/2025 Youtube video summaries using Grok AI

Six Personal Observations That Convinced Me to Retire Early

This is a summary of a personal reflection from a retired engineer (now in his 60s, who retired at 54) sharing six key insights or "principles" that pushed him toward early retirement. These are drawn from his own experiences, fears, and observations in the retirement planning community. He emphasizes that these helped him overcome common barriers like anxiety and perfectionism, ultimately allowing him to retire sooner than planned.

1. Prioritize Health Over Everything — Don't Let Your Job Destroy It

A personal survey showed that ~57% of respondents' biggest retirement fear is health-related (47% general health issues for self/spouse, plus 10% long-term care needs). Yet running out of money ranked lower at 33%. The irony: many stay in high-stress jobs that harm health through poor sleep, lack of exercise, unhealthy eating, and chronic stress — exactly what accelerates the fears they're avoiding.

Key takeaway: Start your health journey today — focus on stress reduction, better sleep, nutrition, and exercise. Waiting until retirement is too late; a toxic job could make retirement shorter or less enjoyable.

2. Don't Let Anxiety and Misunderstood Monte Carlo Simulations Trap You at Work

Anxiety often involves overestimating risks while underestimating your control. Monte Carlo simulations (common in retirement planners) might show a 70-80% success rate, which feels "failing" if you're aiming for 95-100%. But that percentage assumes zero adjustments over 30+ years.

In reality, everyone adapts: during market downturns, you'll naturally cut spending (e.g., fewer restaurants, cheaper vacations). Implementing "guardrails" — like reducing spending by 5-10% when portfolios drop — dramatically boosts success odds without needing perfect scores.

Key takeaway: Chasing 99% success often means working extra years unnecessarily. Recognize you'll intervene, giving you far more control than the static simulation suggests.

3. Avoid Moving the Goalposts — It Makes You Feel "Poor" Forever

It's common to set a retirement target (e.g., $1 million saved), hit it, then raise it to $1.2 million due to inflation fears, bad economic news, or general anxiety. This resets progress, breeding dissatisfaction and delaying retirement.

This happens post-retirement too: even with more money than planned, fear persists. Humans are wired for negativity bias (fear hits twice as hard as positivity) — an evolutionary trait for survival, but unhelpful here.

Key takeaway: Accept that no target feels "enough" in the moment. Stick to original goals to avoid perpetual striving.

4. Time Is Finite — Ask Yourself the Steve Jobs Question Daily

Inspired by Steve Jobs' Stanford commencement speech: "If today were the last day of my life, would I want to do what I'm about to do?"

Too many "no" answers in a row signal it's time for change. The speaker, enjoying ~50% of his engineering job (mentoring, teamwork) but hating the other half (paperwork, emails, bureaucracy), realized work had too many "nos."

Retirement has "nos" too, but far fewer consecutive ones, allowing more control over time.

Key takeaway: Value your limited days; don't spend most of them on unfulfilling work.

5. The "Perfect" Plan Is Only Visible in the Rearview Mirror

Looking back, the path to early retirement (starting savings young, living below means, staying invested through downturns) seems obvious. But forward, it's foggy — you can't connect the dots ahead of time.

Perfectionism paralyzes; waiting for certainty means never retiring. Instead, follow the advice (attributed to coach Lou Holtz): "Do the next right thing."

Key takeaway: Progress through consistent small decisions (saving, healthy habits) compounds. Trust the process without needing full visibility.

6. Fees Matter, But There's a Middle Ground Beyond All-or-Nothing

High advisory fees (e.g., 1% AUM) act like "termites" eroding wealth, but full DIY isn't for everyone. Alternatives exist:

- One-time plan reviews (~$250-300) by certified planners to spot weaknesses.

- Full plan creation (~$3,000-4,500) with ongoing support, as a low-commitment way to test advisors.

The speaker recommends specific firms offering these (with negotiated rates for his audience), blending DIY control with professional input.

Key takeaway: Watch fees, but pay selectively for expertise where it adds value — avoiding extremes.

Final Thoughts

These observations nudged the speaker to retire earlier, despite imperfections. He hopes they encourage others to retire 1-2 years sooner, emphasizing action over fear. Retirement isn't about flawless plans but reclaiming health, time, and peace of mind. (Word count ~850; estimated 8-10 minute read.)

Retiring Comfortably with Less Than $200,000: A Case Study on Buzz and Why Comparison Is the Enemy

This is a summary of a video by David (from the channel "David in Progress"), who uses fellow YouTuber Buzz (from "Buzz's Retirement Garage") as a positive case study to challenge the idea that you need hundreds of thousands—or millions—in savings to retire well. David argues that retiring with under $200,000 can not only "work" but "work well," especially when paired with Social Security, low expenses, and a debt-free lifestyle. The core message: Stop comparing yourself to others; your retirement number is uniquely personal.

Who Is Buzz and Why Does He Matter?

Buzz is a retired YouTuber in his mid-60s who focuses on living comfortably solely on Social Security. Recently, he revealed his retirement savings:

- Started retirement with around $300,000.

- Now it's less than $200,000 (he doesn't disclose exact figures).

Buzz felt down after seeing other creators talk about retiring with "$500,000 or less" as if that were a modest amount. This triggered the "comparison trap"—feeling inadequate because his nest egg is smaller. David uses this to highlight how harmful comparison can be in personal finance.

Buzz's Actual Financial Picture: He's Doing Great

- Social Security: $3,876/month ($46,512/year) — covers 100% of his monthly bills (he shares detailed breakdowns on his channel).

- Lifestyle: Married, no debt, modest expenses.

- Additional income: Successful YouTube channel generating side earnings (which he can invest).

- Investments: Some individual stocks and other assets, but he doesn't draw down the principal for living expenses.

By median standards, Buzz is ahead:

- For married households aged 65–74, median retirement savings is only ~$112,000 (per recent data David referenced).

- Even at under $200,000, Buzz is above average.

His Social Security alone is a "superpower." To generate $46,512 annually from investments (using the common 4% safe withdrawal rule), someone without Social Security would need roughly $1.16 million in savings. Buzz gets that guaranteed income stream without touching his nest egg.

The Power of Not Spending Your Savings

Because Social Security covers essentials, Buzz's < $200,000 can grow untouched via compounding. David runs a simple projection using a low-cost, diversified portfolio (60% FXAIX, 30% FXNAX, 10% FZIPX — historically ~7% average annual return):

- Starting at $200,000:

- 5 years → ~$280,000

- 10 years → ~$393,000

If Buzz invests his YouTube earnings (e.g., into a Roth IRA for tax-free growth), the pot grows even faster. This creates a growing buffer for future expenses (healthcare, emergencies) he's occasionally worried about.

Early Retirement vs. Traditional Retirement: Different Rules

David (early retired, no Social Security or Medicare yet) notes that FIRE (Financial Independence, Retire Early) folks often need larger portfolios because:

- No guaranteed income streams.

- Higher healthcare costs pre-Medicare.

- Longer retirement horizon.

The classic 4% rule or 25x expenses multiplier can feel intimidating if applied blindly. But for someone retiring at 65+ with Social Security and Medicare, the effective "needed" savings drops dramatically. Social Security acts like a inflation-adjusted bond ladder—reliable and risk-free.

The Real Problem: Comparison and One-Size-Fits-All Numbers

Influencers often throw out big figures:

- $1 million as the "magic" number.

- Some (like Suze Orman) claim even $10 million isn't enough.

These create unnecessary anxiety. Comments David sees: "I'll never have enough," or regret over not saving earlier. But:

- Personal finance is personal.

- What matters most: How much does your life actually cost?

- Key factors: Debt (mortgage/car payments), spending habits, location, health.

Chasing someone else's number brings stress, not peace.

David's Advice and Call to Action

- Know your own number: Calculate expenses honestly. Subtract guaranteed income (Social Security, pensions). The remainder is what savings must cover.

- If already retired with "less": Don't beat yourself up. Maximize what you have—let it compound, add side income if possible, focus forward.

- If years away: Use any wake-up call positively. Cut expenses, boost savings—it's not too late.

- Mindset shift: Comparison causes stress; clarity comes from self-awareness.

David praises Buzz for his transparency and inspiration, reminding viewers that Buzz is "doing terrific" and improving yearly. He encourages generating some income in retirement (YouTube, side gigs) for flexibility and purpose.

Final Takeaway

Retiring with less than $200,000 isn't failure—it's often success when paired with Social Security, low costs, and smart habits. Buzz proves you can live well without a massive portfolio. Stop comparing; define success on your terms. Focus on controllable factors: expenses, debt, and growth of whatever you have. Peace in retirement comes from knowing your number works for your life.

(Word count ~920; estimated 8–10 minute read.)

Lessons from a Failed Specialty Café: Why It Closed After 4 Months and What I Learned

This is a candid reflection from Charlie (YouTube channel focused on home espresso and latte art) about his short-lived specialty café venture. In December 2022, he and his sister opened a small café in the rural village of Hilton, Cambridgeshire, UK. Despite high hopes, they closed in March 2023 after just four months. Charlie shares the key mistakes, hard realities of running a café, and how the experience shaped his life and content creation.

The Setup and Initial Vision

- Charlie moved in with his sister to bootstrap the business on a tight budget.

- They renovated the space themselves (plastering, painting, lighting) to save money.

- Rent was affordable, and locals had long requested a café, so they assumed daily regulars would sustain it.

- Focus: Specialty coffee with in-house roasting (sister’s partner roasted the house blend; Charlie handled smaller specialty batches).

- Equipment: Budget-conscious (La Spaziale S5 compact espresso machine, Mahlkönig K30 grinder, Turin DF83 for single-dosing). Great beans (e.g., Brazilian house espresso, rotating Ethiopian and El Salvadorian specialties), but no high-end machines or fancy interior.

They aimed to create a “third space” — a community hub beyond home and work.

Why It Failed: The Biggest Mistakes and Challenges

- Wrong Location and Underestimating Foot Traffic

- Rural village setting meant low walk-by traffic.

- Many locals weren’t active on social media, so Instagram ads (Charlie’s marketing background) were ineffective.

- Word-of-mouth spread slowly in countryside areas; grassroots growth takes far longer than expected.

- Insufficient Runway Capital

- They opened with essentially zero buffer after setup costs.

- Recommendation: Have 9–12 months of operating expenses saved (rent, salaries, beans, electricity — which skyrocketed during the 2022 UK energy crisis).

- Many mornings: No customers until after 9 a.m., yet they had to open at 8 a.m. to fulfill the “café promise” of reliability.

- Opening in Mid-December Was a Disaster

- Freezing UK winter discouraged people from venturing out.

- Energy crisis made heating expensive and the space uncomfortably cold (thin walls, small electric heater).

- Charlie developed painful “barista wrist” (like carpal tunnel) from cold-stiff hands locking portafilters daily — it lingered for 8 months.

- Specialty Coffee in Low-Volume Shop Is Costly

- Daily dial-in adjustments (for humidity, temperature) wasted shots when traffic was low (sometimes only 10 customers/day).

- This inflated bean costs by ~30% on slow days.

- Choice: Waste beans to maintain quality or serve subpar drinks — they chose quality, hurting margins.

- Bootstrapping Limits Quality Perception

- Couldn’t afford premium machines (dreamed of Slayer or La Marzocco GB5) or upscale interior.

- Customers sense the difference; Google reviews praised the coffee but the space felt basic.

- Community Building Takes Time and Effort

- They hosted successful coffee cuppings (sold out) and helped with a village “Warm Hub” event during energy crisis.

- These brought some customers, but winter timing slowed momentum.

- True longevity comes from culture and community, not flashy launches.

The Personal Toll

- Charlie invested most savings and months of time → left broke.

- Moved back from Tokyo, felt isolated in countryside, struggled mentally.

- After closure: Returned to full-time job managing a successful YouTube channel (creative direction, thumbnails, analytics).

- Took a content break after father’s passing in August 2023; considered quitting YouTube entirely.

Silver Linings and What Kept Him Going

- Positive Google reviews showed people appreciated the high-quality coffee.

- Clever deals (e.g., portable counter with built-in tap/rinser — no expensive plumbing needed).

- Reinvigorated passion: Trips to Madrid (met creators, dialed in amazing setups) and Host Milan (industry connections) reignited excitement.

- Community feedback on his videos (helping people pull better shots or pour latte art) remains the most rewarding part.

Current Path: Quitting the Job to Go All-In on Content and a New Product

- Saved aggressively from full-time job.

- Quit in April (year not specified, but post-2023).

- Launching The Brew Ledger — a physical journal for tracking espresso recipes, grinder settings, beans, etc. (something he’s used personally for years).

- First print run of a few hundred copies arriving soon; planning crowdfunding.

- Encourages sign-up at homecafebycharlie.com mailing list and Instagram (@homecafecharlie) for updates.

Key Takeaways Charlie Wants to Share

- Starting a café is extremely hard — especially specialty in low-traffic areas.

- Promise excellence in everything (remake bad drinks, dial in properly) even when it hurts short-term profits.

- Location, timing, capital buffer, and community are make-or-break.

- YouTube (especially gear-heavy niches) is tough financially — ad revenue barely covers costs, let alone profits.

- Failure teaches more than success; he’s grateful for the lessons and connections.

Charlie ends on a hopeful note: He’s excited again about coffee, deeper technical content, and building something tangible with The Brew Ledger. He invites questions about the café experience, starting a business, YouTube struggles, or the upcoming product.

(Word count ~920; estimated 8–10 minute read.)

How Millennials and Gen Z Were Priced Out of Homeownership: The Four Big "Scams"

Alice, a millennial CPA and wealth management firm owner, argues that skyrocketing U.S. housing costs over the past 20+ years aren't just normal market cycles—they're a structural shift favoring older, wealthier homeowners at the expense of younger generations. Using a relatable example (parents buying a house cheaply in the '90s vs. today's requirements), she outlines four key factors and offers practical strategies to navigate them.

The Stark Generational Gap

- In the 1990s: A $200k house with a $600/month mortgage, affordable on a $35k salary (at age 28).

- Today: The same house might cost $2M, requiring a $4,200/month mortgage and ~$168k annual income.

- Reality: Median income for young adults (25–34) is around $57k (as of recent data), making similar homes unattainable for most.

This has widened the wealth gap: Older generations rode asset appreciation waves, while younger ones face permanent renter status.

Scam #1: Mortgage Interest Deduction (MID) – A Wealth Transfer Upward

U.S. taxpayers can deduct mortgage interest when itemizing, but benefits skew heavily to high-income, large-mortgage owners:

- Lower/middle-income families often take the standard deduction → no benefit.

- High-earners: $8k–$15k+ annual savings.

- Result: Encourages bigger loans/higher prices (economists estimate 5–10% price inflation from MID).

- Cost: ~$25–30 billion/year in lost government revenue (recent estimates), mostly aiding existing wealthy homeowners.

Originated in 1913 when cash buys were common; now it subsidizes debt-fueled appreciation for asset owners.

Scam #2: Restrictive Zoning Laws – Artificial Supply Limits

In most U.S. cities, 60–75%+ of residential land is zoned exclusively for single-family detached homes, banning duplexes, triplexes, or apartments.

- Example: A lot that could hold 4 affordable units is restricted to 1 expensive house.

- Roots: Post-WWII policies, often to preserve "neighborhood character" (and property values for incumbents); some trace to exclusionary intent.

- Consequence: Restricted supply + growing population = soaring prices.

Countries like Japan/Germany allow denser building near demand, keeping prices stable.

Scam #3: Institutional Investors Dominating the Market

Since ~2010 (post-2008 crash), investors (hedge funds, corporations, foreign buyers) have bought millions of single-family homes:

- Often cash offers → outbid families.

- Peak: Up to 25–28% of purchases in hot years (e.g., 2021); some markets 40–50%.

- Big players: Firms like Invitation Homes (80k+ properties) treat homes as commodities, converting ownership to rentals.

No issue with investing per se, but scale disadvantages young families, turning potential owners into permanent renters.

Scam #4: Post-2008 Monetary Policy and Asset Inflation

Low interest rates (to recover from recession) made borrowing cheap → inflated assets:

- Home prices: Up ~180%+ since 2008.

- Stocks (S&P 500): Up ~400%+.

- Wages: Only ~30–40% growth.

Boomers/older owners (who held assets in 2008) gained massively; younger people entered a pricier market.

Combined with U.S.-specific supply restrictions, this created extreme unaffordability.

What You Can Do: Practical Strategies

Much is systemic, but individuals can adapt:

- Geographic Arbitrage — Move to affordable areas (e.g., Midwest/South: homes <$200k in Pittsburgh, Cleveland, Kansas City, parts of Texas). Trade lower salary for ownership.

- House Hacking — Buy multi-unit property; live in one, rent others to cover mortgage. Turn home into income-producing asset.

- Alternative Models — REITs, co-housing, community land trusts, shared equity for real estate exposure without full ownership.

- Build Wealth First (Rent + Invest) — Stocks historically outperform real estate post-2008 (400% vs. 180%). In high-rate environments, renting cheaply and investing the difference can outperform expensive buying (early mortgage payments mostly interest).

Alice emphasizes budgeting (offers free zero-based tool) and mindset: Know the system, then play smart within it.

(Word count ~950; estimated 8–10 minute read.)

Interviews with Dave Ramsey, Jimmy John Liautaud, and Charlie Sheen: Secrets to Building (and Rebuilding) Wealth

This YouTube video features host James (a content creator interviewing high-profile figures) traveling to Nashville, Tennessee, to speak with three successful men: financial guru Dave Ramsey, sandwich chain founder Jimmy John Liautaud, and actor Charlie Sheen. The interviews focus on their paths to wealth, key lessons, sacrifices, and advice for the younger generation. (Note: As of late 2025, public estimates place Dave Ramsey's net worth at ~$200 million, Jimmy John's at ~$2–3 billion, and Charlie Sheen's at ~$3 million after past setbacks.)

1. Dave Ramsey: The Debt-Free Path to Wealth

Dave Ramsey (age 65), founder of Ramsey Solutions, built his empire after personal bankruptcy in his 20s, which deepened his faith and anti-debt philosophy.

Key Highlights:

- Company revenue: ~$300 million in the interview year.

- Real estate holdings: ~$850 million (mostly his campus), all paid in cash.

- Net worth: He casually says "probably a billionaire," but current estimates are $200 million.

- On debt: "Debt equals risk; the borrower is slave to the lender." Avoids it entirely, even for scaling—grew organically to withstand crises like COVID or 2008.

- Real estate advice: Buy with cash, move slowly. Debt-free properties generate massive cash flow, creating a "positive snowball" (first few are hardest).

- Patience and opportunism: Bought land cheap long-term; scooped bargains in 2008 crash.

- Life-changing advice: "Nobody's coming to save or discover you. Get up, leave the cave, kill something, drag it home—every day."

- On younger generations: Praises optimism but warns against seeking "easy buttons"—true success is slow-cooked.

- Guiding principle: "Follow God" (Jesus).

Ramsey emphasizes consistent action, faith, and rejecting debt for long-term security.

2. Jimmy John Liautaud: Grinding from Sandwiches to Billions

Jimmy John Liautaud (age 61), founder of Jimmy John's, started with modest goals but sold the chain (valued ~$3.5 billion) to become a multi-billionaire.

Key Highlights:

- Started in 1983 with a $25k loan; initial aim: "Enough for weed and beer."

- Poor student (second-to-last in class) but relentless entrepreneur.

- Sold majority stake in 2019; net worth ~$2–3 billion today.

- Life-changing advice (1987): "If you can't measure it, you can't manage it." Know your numbers; people follow actions, not words.

- Turnaround story: In 2003, with 70/200 stores failing, shifted to honest franchising—told prospects it's a brutal grind (24/7/365 lifestyle). Sold one store at a time to committed "grinders," leading to 2,500+ locations.

- Differentiation: "Freaky fast" delivery (from B/C locations) via aggressive sampling on campuses.

- Investments: Understandable assets like farmland (easy to manage, profitable) and gold/land early on. Bets on "jockeys" (passionate entrepreneurs without excuses).

- On work-life balance: "Biggest line of [BS] ever created." Building from nothing requires extreme sacrifice—no shortcuts.

- Regrets: None—"All we have is now and the future."

- Survival mindset: Endured betrayals, scams; focused on moving forward.

Liautaud's story is raw hustle: Measure everything, demand excellence, embrace the grind.

3. Charlie Sheen: Resilience Through Highs and Lows

Charlie Sheen (age 60), iconic actor (Wall Street, Two and a Half Men), was once TV's highest-paid star but faced public scandals, addiction, and financial fallout.

Key Highlights:

- Made millions acting; peak earnings made him one of Hollywood's richest.

- Current net worth: ~$3 million (down from $150 million peak due to personal issues).

- Success driver: "Believe in myself when others didn't." Don't let small minds cancel big dreams.

- On money: Not the best advisor—save for "rainy days" that can become "rainy decades."

- People lessons: They constantly surprise; stay observant (as an actor).

- Through adversity: Hollywood "banished" him, but "they couldn't put my brain in timeout." Never gave up on himself.

- Advice for rock bottom: "It's never too late for a fresh start."

- Best advice (from dad Martin Sheen): Honor your word—especially promises to yourself.

- Guiding principle: "DFSU" (Don't F*** S*** Up).

- Overall: Most people mean well; put yourself first sometimes.

:max_bytes(150000):strip_icc():focal(999x0:1001x2)/aka-charlie-sheen-premiere-090925-814480b8b0fa455c9c23bc2b90373bf0.jpg)

Sheen's segment shifts to resilience and self-belief amid setbacks.

Common Themes and Host's Pitch

All three stress persistence, self-reliance, and learning from failures. Ramsey and Liautaud highlight measurable systems and sacrifice; Sheen focuses on inner belief.

The host promotes his "School of Mentors" community and a free "Generational Wealth Day" event (noted as past October 2025).

This video mixes inspiration with raw truths: Wealth demands grit, smart risks, and often faith or forgiveness. (Word count ~950; ~8–10 minute read.)

The Brutal Truth About Real Survival: Why 90% of Prepper Gear Is Useless

This no-nonsense rant challenges common "prepper" misconceptions, arguing that societal collapse isn't dramatic—it's slow death from dehydration, exposure, hunger, and thirst. Most survival kits are overloaded with gimmicky, complex gear ("tactical theater") that becomes dead weight. Instead, focus on five simple, reliable tools addressing core needs: clean water, fire, cutting, immediate filtration, and shelter. Everything else is luxury that hinders mobility and endurance. Mastery and practice trump hoarding.

The author warns: Collapse offers no warnings, no tutorials, no retries. Skill + reliable function = survival. Complexity kills.

The Five Essential Tools

- Metal Container for Boiling Water Water is priority #1—you die in ~3 days without it. Storage fails when empty; focus on production and sterilization. Boiling (1 minute) kills nearly all pathogens (bacteria, viruses, parasites). Need: Bare metal (stainless steel preferred) that withstands direct fire—no coatings, insulation, or plastics that melt/explode. Efficient heat conduction is key.

- Ferrocerium Rod (Ferro Rod) Fire Starter Fire purifies water, cooks, warms, signals, and deters threats. Convenience items (lighters, matches) fail when wet, cold, or depleted. Need: Mechanical spark producer (5,000+°F sparks) that ignites damp tinder reliably, with thousands of uses. Pair with a striker.

- Full-Tang Fixed-Blade Knife Avoid multi-tools or folders (fragile moving parts). Need one solid piece of steel (full tang: blade extends through handle). Blade length: 4–6 inches (versatile for control and heavy tasks). Material: High-carbon steel (sharpens easily on rocks, holds edge better than stainless—rust is manageable with care). Uses: Processing food/wood, building shelter, countless tasks. In untrained hands, it's a self-injury risk.

- Portable Water Filter Boiling takes time/fuel; filters provide instant hydration from dubious sources (removes bacteria/parasites/protozoa). Doesn't handle chemicals/heavy metals but prevents immediate illness/dehydration. Need: Compact straw or pump system rated for thousands of gallons (e.g., Sawyer Mini or LifeStraw equivalents).

- Heavy-Duty Tarp Exposure (cold, wet, wind) kills fastest. Tents are bulky/rigid; tarps are lightweight, packable, infinitely adaptable. Size: ~8x10 ft waterproof material. Configurations: Lean-to, A-frame, ground sheet, rain catcher, windbreak, signal panel, stretcher. Subtle colors avoid attention.

Why This Minimalist Approach Wins

- Less weight → Better mobility/endurance (critical when fleeing or foraging).

- Fewer failure points → Reliability under stress (wet, cold, dark).

- Mastery over gadgets → Practice these five until instinctive; confidence from competence.

- Ditch the "132-piece kits"—they scatter focus and become abandoned junk.

The hard truth: Survival is cold, quiet suffering. No drama, just biology failing. Prep with function, simplicity, and skill—not fantasy gear. Strip your kit to these essentials. Practice relentlessly. When the world ends, you'll function while others fumble.

(Word count ~920; estimated 8–10 minute read.)

Dave Ramsey Critiques Graham Stephan's ~$20M Portfolio: Leverage vs. Debt-Free Freedom

In this popular YouTube video, real estate investor and YouTuber Graham Stephan (known for frugal-yet-luxurious lifestyle content) sits down with personal finance icon Dave Ramsey for a rare portfolio review. Graham, in his mid-30s, has built substantial wealth primarily through real estate deals in California and Las Vegas. Dave, the debt-averse guru with hundreds of millions in paid-off real estate, offers candid feedback—praising Graham's talent while pushing his signature "no debt" philosophy.

Graham's Portfolio Breakdown (~$20M Net Worth)

- Real Estate Heavy (core strength): Multiple rental properties, primarily in California (selling some) and Las Vegas.

- Early buys: Cash or high down payments (e.g., first property $59.5k cash + $12k reno).

- Standouts: "Zero dollar home" (refinanced to pull out all equity, lived rent-free via rentals/studio use); clever duplex flip (added wall to turn 1-bed into 2-bed, boosting rent/value 50%).

- Current home: $2.1M Vegas property (large down payment for low payment); half studio for content.

- Equity: Massive appreciation (e.g., one property from $780k buy → $1.35M value).

- Stocks: ~80% S&P 500/international index funds; small individual holdings (e.g., top: Google, Apple).

![OC] My Stock Portfolio Vs. S&P 500 : r/dataisbeautiful](https://i.redd.it/wdhdayncwfn91.png)

- Crypto: ~$450k (down from $1M peak; slightly underwater on cost basis).

- Cash: Large reserves (feels "excessive" but comforting as safety net).

- Angel Investments: Fintech startups (~play money, not counted in net worth).

- Luxuries: Cars/watches bought as "enjoy for free" investments (e.g., Ford GT appreciated significantly).

- Debt: ~$4.02M across five 30-year fixed mortgages (rates 2.875%–3.625%—very low, tax-deductible).

Dave Ramsey's Critique and Advice

Dave compliments Graham's sophistication and real estate savvy ("unusually gifted"—far beyond typical high-net-worth individuals he studies). He notes wealthy people often keep portfolios "ridiculously primitive": Find what you understand/excel at, then do it repeatedly (e.g., farmers buy farmland).

Key Feedback:

- Real Estate Dominance: Perfect fit for Graham—lean into it (80/20 real estate/stocks). Suggests 1031 exchanges when selling CA properties; shift toward commercial for higher cash flow/IRRs.

- Stocks/Single Picks: Fine in small doses (<1% net worth); most individual stock pickers lose money long-term.

- Crypto: High risk—okay if you can stomach total loss ("let money evaporate"), but Dave avoids entirely.

- Cash Hoard: Smart for real estate investors (lowers risk, provides pinch protection)—common blind spot.

- Luxuries/Angels: Treat as fun/gravy, not core wealth.

- Debt (The Big Debate): Graham defends low-rate leverage (below inflation, deductible, opportunity cost). Dave counters: No wealthy person regrets going debt-free eventually. Leverage built wealth but increases risk—paying off feels liberating ("feel it leave your body"). Math ignores risk; net worth same on paper, but peace/practicality huge.

If Dave Took Over: Pay off mortgages fast (use sales/equity), go fully debt-free, heavy into paid-for real estate (residential + commercial).

Core Themes: Be You, But Consider Risk

Dave frees Graham (and viewers) to embrace strengths without chasing "sexy" diversification. No secret sauce to wealth—just consistent excellence in your lane. Graham's leverage worked brilliantly; Dave's debt-free approach built resilience. Debate highlights classic investor split: Optimized returns vs. minimized risk/peace.

Video ends with Graham pondering the emotional pull of debt freedom despite logic favoring leverage.

(Word count ~920; estimated 8–10 minute read.)

A Raw Confession: From Financial Success to $125,000 in Debt and Starting Over

In this emotional, unscripted YouTube video, a content creator (who previously built a successful business and lifestyle brand) shares the painful reality she’s been hiding for years: the complete collapse of her finances in 2023 and the long, difficult climb back.

The Fall

- In 2023 she lost her entire business and primary income streams.

- They lost their home, car, and most possessions.

- Faced impossible choices: lights off or water off? Homelessness?

- Sold everything possible to survive, including equity from previous houses.

- For over two years they’ve been in survival mode, barely keeping up month to month.

She describes the shame and fear of admitting this publicly—going from “never dreamed possible” success to staring at a massive debt list while income is drastically lower.

The Debt Breakdown (as of the video)

She lists everything on paper in real time, no fancy spreadsheets or perfect organization—just raw honesty.

Total debt: $124,759

Major categories (approximate):

- Credit cards (Capital One, Ulta, Home Depot, Lowe’s, American Express, etc.): ~$15k–$20k

- Spectrum bill (old utility): $3,398

- Husband’s student loans: $19,543

- Her student loans: ~$20,000 (with interest)

- IRS back taxes: $17,344

- Medical bills (multiple): several hundred each, totaling several thousand (insurance no longer covering some items)

- Care Credit (pet emergency): $500

- Business-related debt: ~$20k–$25k

- Personal loan: undisclosed amount

- Utility arrears: $1,200

- Various other small debts and lingering medical charges

She notes that this is already much better than the peak (~$400,000 including mortgages), thanks to selling houses and paying down chunks of debt with equity.

What She’s Learned

- She used to have bad spending habits when money was flowing freely (“I didn’t care what I spent”).

- Success bred complacency; she assumed income would always grow.

- Tried to file Chapter 13 bankruptcy to save the house but didn’t complete it; the process still closed many credit accounts even when she wasn’t behind.

- Now living paycheck-to-paycheck, every month is a struggle.

Her Plan Moving Forward

- Cash budgeting / cash-envelope system hybrid (especially for categories where she overspends).

- Separate bill-pay account for fixed expenses.

- Cash only for discretionary spending (no card swiping).

- Will share a full month’s bank statement breakdown (which she calls “the most horrendous thing I’ve ever seen”) in a future video.

- Open to community advice and support.

The Emotional Core

She cries, laughs nervously, and admits she judges herself too. The video feels like a therapy session: calculating the debt out loud, hearing her husband laugh in the background, dogs barking—it’s real life, not polished content.

Her message: “We’re going to do it. It’s nice not to be alone anymore.”

She asks viewers to subscribe, comment with suggestions, and stick around as she documents the comeback.

(Word count ~920; estimated 8–10 minute read.)

Four Life-Changing Books (Plus Bonuses) That Helped Me Save 40%+ of My Income for 5 Years

In this motivational video, a young content creator (who left his day job at 24, saved $100k by 25, and built a sustainable YouTube income) shares the unconventional books and resources that transformed his financial mindset. He rejects typical "cut lattes" advice as minor, focusing instead on extreme, proven shifts in thinking and behavior that allowed him to consistently save 40%+ of income through tiny habits, strategic sacrifice, and asset-building. These ideas helped him achieve financial freedom, better health, and a fulfilling life—results he attributes to stacking small changes over years.

1. Atomic Habits by James Clear – Tiny Changes, Remarkable Results

The foundation: Small, consistent habits compound into massive outcomes.

Key takeaways:

- Headline promise ("tiny changes, remarkable results") is real—his successes (quitting job young, $100k saved, consistent fitness, reading 100+ money books, family life) stem from stacked micro-habits.

- Examples: Batch-cooking lunches (saved ~$4,300/year vs. buying out); gym 3x/week since age 17 (lost 40 lbs, maintains health easily).

- Mindset shift: Identify and eliminate 3–5 daily money-wasters (e.g., energy drinks, eating out, expensive car). Cutting just a few for 5 years drastically changes finances without feeling deprived.

- Systems over willpower: Build autopilot habits (e.g., consistent posting led to podcast invites and opportunities).

Result: Habits make extreme saving feel effortless over time.

2. Set for Life by Scott Trench – The Freedom Runway to $100k+

Escape the frugality trap by phasing into income/housing strategies.

Key concept: "Freedom runway" – Build a base, then accelerate.

- Phase 1 ($0–$25k): Extreme frugality (e.g., chicken/rice/beans diet, thrift clothes, old cash car, no travel/dining out). Took him ~4 years on low income.

- Phase 2 ($25k–$100k+): Shift to housing hacks (house hacking, renting rooms/Airbnb) and income growth (raises, side jobs, skill-building).

- His story: Held 3 jobs while reading this; brother Airbnb'd spare rooms in duplex.

- Long-term: Frugality is short-term tool; scale via scalable income/jobs.

This book pushed him beyond saving-alone to aggressive wealth-building.

Bonus: MasterClass (Not a Book) – Learn Directly from World-Class Experts

Invest in accelerated knowledge from proven achievers.

Why it works:

- Experts condense 40 years of mastery into hours (worth far more than cost).

- Examples: Branding lessons from Liquid Death founder (humor/curiosity in marketing); habits from James Clear himself.

- Affordable (~$10/month annually); covers business, wellness, cooking, etc.

- One idea can change everything—far better return than random spending.

He credits platforms like this (plus podcasts/YouTube/courses) for shortcuts that "don't make sense not to buy."

3. Your Money or Your Life by Vicki Robin – Money = Life Energy

Radical reframe: Spending wastes irreplaceable time/life.

Core ideas:

- Money earned via time = life energy traded away.

- Examples: $50 jeans = quarter-day of work; daily soda/lunch/Amazon buys waste hours daily.

- Calculate "real hourly wage": Salary minus work expenses (commute, clothes, food, decompression).

- His revelation: $10/hour job → actually ~$4–5/hour after costs.

- "Enoughness": Diminishing returns past basics (healthy food improves life; luxury beyond doesn't).

- Result: Horrified by waste → stopped trading life for stuff; found contentment post-"enough."

Shifted him from mindless spending to intentional life design.

4. Rich Dad Poor Dad by Robert Kiyosaki + The 4-Hour Workweek by Tim Ferriss (Grouped)

From trading time → building assets/businesses that reclaim life.

Rich Dad Poor Dad:

- Assets (make money) vs. liabilities (cost money).

- Goal: Acquire enough assets to cover expenses → freedom.

- Ignited his asset focus (investments, YouTube as income engine).

The 4-Hour Workweek:

- Initially seemed "scammy"—now lives it (YouTube ~5 hours/week supports him).

- Build low-maintenance income streams.

- Met dozens doing similar (not just YouTube).

Combined: Sacrifice short-term to buy/build assets → escape time-for-money trap.

Honorable Mention: Extreme Ownership by Jocko Willink

Take radical personal responsibility.

- Broke? Your fault (decisions, habits, lack of skills/knowledge).

- Blaming system/government wastes energy—learn "cheat codes" instead.

- Do the opposite of the masses: Their average results (debt, poor health) come from conventional advice.

- Ownership = motivation + freedom (change what you control).

Overall Philosophy and Results

These resources reject mainstream "normal" paths, favoring:

- Extreme short-term sacrifice for long-term freedom.

- Habits + systems over motivation.

- Assets/business over endless grinding.

- Ownership + contrarian thinking.

His proof: Left job at 24, $100k by 25, 40%+ savings rate 5 years running, low-stress YouTube income, health/family balance—all from applying these principles consistently.

He promotes MasterClass (sponsor), Shortform for summaries, and his upcoming YouTube course cohort (goal: help 100 people quit day jobs).

Message: Be willing to be "different" and extreme—results compound insanely.

(Word count ~920; estimated 8–10 minute read.)

Why Reaching $100k Is Just the Start: The Critical Shift to $1 Million Wealth

Nick, a personal finance advisor, delivers a wake-up call for those hitting $100k in investable assets: Congratulations—you're in the top ~22–28% of Americans with significant liquid wealth (most tie net worth to homes/cars). But the strategies that built this (extreme frugality, micro-optimizations like coupons/gas savings) will trap you here if unchanged. This "false finish line" breeds complacency; coasting on compound interest won't cut it. The $100k–$1M leap requires a mindset switch: from optimization (small tweaks) to maximization (big systems, income acceleration, calculated risks). Miss this, and you'll stall for decades.

The Ladder of Personal Finance: Climb in Order

Build a "well-oiled machine" by prioritizing tax-advantaged accounts and debt elimination:

- Max Employer 401(k) Match — Free money (e.g., 50% match on 6% = instant 50% return).

- Eliminate High-Interest Debt (>7–8%) — Paying 20% credit card interest while investing at 8% loses money.

- Fund Roth IRA (if eligible) — 2025 phase-out starts ~$150k single/$236k joint; tax-free growth/withdrawals.

- Max 401(k) — $23,500 (under 50); higher catch-ups for 50+ (up to $11,250 extra for ages 60–63).

- Max HSA (if HDHP eligible) — Triple tax-advantaged (deduction + tax-free growth + qualified withdrawals).

- Taxable Brokerage — Unlimited contributions for faster acceleration.

Key Strategies for Acceleration

- Annual 1% Rule: New Year's—bump savings/investment rate 1–2%. Example: Age 30, $70k salary, starting 10% → gradually to 20% = ~$3M vs. $1.8M at retirement (8% returns).

- Automation 2.0: Sub-accounts for goals (travel, wedding); frees mental energy for big moves.

- Financial Cleanup: Consolidate old 401(k)s, close unused accounts.

- Income Over Frugality: Research market rates (Glassdoor/Salary.com/networking); negotiate raises/promotions. 10–50% jumps compound faster than returns. Side income ($1k/month → $540k+ over 20 years).

Avoid Traps: Big $50,000 Questions

Shift focus from $5 tweaks (cheap lattes) to high-impact decisions:

- Housing: Renting can beat buying (hidden costs: taxes, maintenance ~30–50% extra). Buy only if long-term fit, not pressure.

- Cars: Avoid $700+ payments—buy 3–5 year used reliable vehicles.

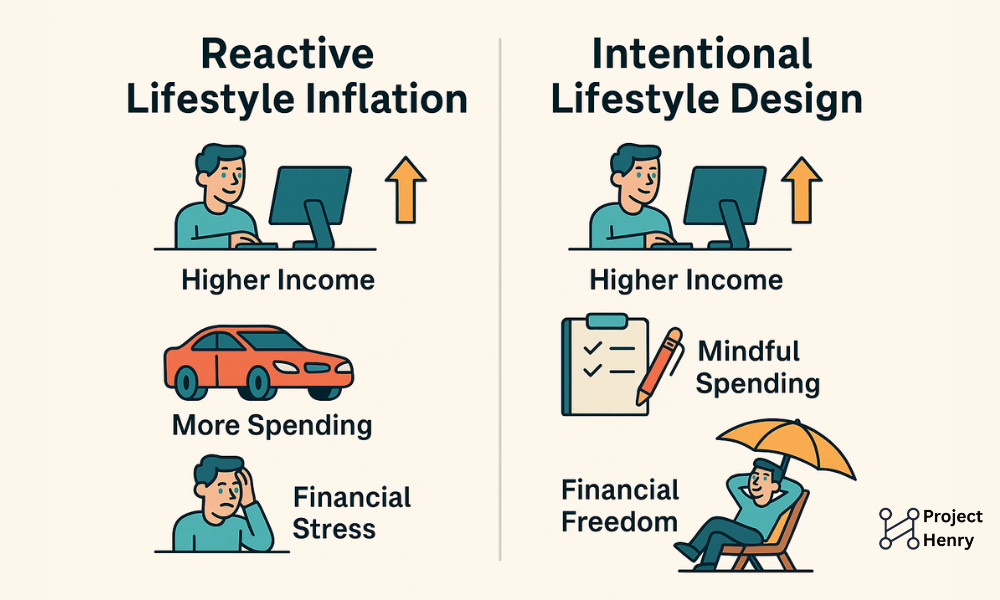

- Lifestyle Inflation: Not zero-spend, but conscious spending—splurge on 3–4 joys (travel/food), cut elsewhere. Set "worry-free" threshold ($100–200 small buys).

:max_bytes(150000):strip_icc()/FinanceYourFuture-LifestyleInflation-v12-b99d165f4b1f4f4eb4b861acccbc13e3.png)

- Taxes: Prioritize maxing accounts over exotic schemes.

Final message: You've proven discipline—now scale it. Comfort kills wealth; push for more income, systems, and intentional choices. $1M isn't more grinding—it's smarter plays for freedom.

(Word count ~920; estimated 8–10 minute read.)

Why 2-Year Trade Schools for Electricians Are Often a Waste (From a Journeyman’s Perspective)

In this controversial YouTube video, The Fat Electrician (a 10-year veteran journeyman electrician) calls out 2-year community college/tech school electrical programs as "more or less a scam." Drawing from his experience (5 years apprentice/helper, 5 years journeyman) and thousands of viewer emails (high schoolers, veterans), he argues they’re unnecessary, rarely beneficial, and often misleading—promising fast-track high pay that doesn't materialize. No affiliations or products to sell; just blunt advice to save time/money.

Core Path to Licensed Electrician (Journeyman/Master)

- Goal: Journeyman license (work unsupervised) → Master (after ~1–2 more years).

- Requirement (most states): ~8,000 hours on-the-job training (4 years full-time) + ~576–800 classroom hours + pass state exam.

- Classroom: Paid by employer/union/state (night classes or block weeks).

- Union vs. Non-Union: Both lead to same license; quality varies by program/contractor, not affiliation.

Trade school diplomas/certificates? Don't qualify you for exam alone—still need full apprenticeship hours.

Why Trade Schools Are Problematic

- No Shortcut: In ~47/50 states, diploma credits nothing toward hours/classroom (must redo apprenticeship training). Rare exceptions (e.g., some reduce hours slightly or classroom).

- No Pay Bump: Graduates start as first-year apprentices (~$18–$22/hour), same as no-experience hires.

- Misleading Promises: Schools claim "$60–$100k/year journeyman pay post-grad"—false; creates entitled attitudes (contractors avoid hiring them).

- Cost vs. Benefit: $10k–$20k+ debt for knowledge covered free in apprenticeship.

- Real-World Reality: New guys do "shitty work" (ditches, flashlight-holding) regardless— no diploma skips hierarchy.

- Anecdote: Co-apprentices with diplomas earned same, learned nothing extra.

Example comparison (two 18-year-olds):

- Trade school grad: 2 years school/debt → 4 years apprentice → journeyman ~age 24.

- Direct helper/apprentice: Starts earning day 1 → joins program faster (known/trusted) → journeyman ~age 23, no debt.

How to Actually Start

- Call local contractors: Ask for helper job, express apprenticeship interest.

- Show up on time, good attitude → likely offered apprenticeship spot (they prefer known workers).

- Union/Non-Union: Not life-altering; transferable experience common.

Other Trades?

- HVAC/Auto/Machining: Schools often helpful.

- Welding/Plumbing: Varies—residential/factory yes; high-specialty (e.g., pipefitting) no (friend wasted $40–50k on top school, still started apprentice pay).

Backlash & Rebuttals

Video responds to Twitter criticism:

- "Unpaid apprenticeship?": No—paid from day 1 (~$20/hour entry in his area, raises yearly).

- "Degree helps hiring?": Often hurts (bad attitudes/entitlement).

- "Skip basic training?": Apprenticeship is training.

Exceptions where school useful:

- College experience/partying (paying for fun/memories).

- Veterans with GI Bill (free).

Balanced note: Not all schools fraudulent, but for electrician licensing, rarely required/beneficial in most states (per sources like BLS, state boards—apprenticeship mandatory; school credits limited/rare).

His plea: Help kids/veterans avoid debt/wasted time—get paid to learn.

(Word count ~880; estimated 8–10 minute read.)

Is There an Index Fund Bubble? Breaking Down the Concerns and What It Means for Investors

As of December 2025, trillions flow into index funds (S&P 500 ETFs, etc.), but critics like Michael Burry warn of a bubble—potentially riskier than the dot-com era. This video explains funds (baskets of stocks for broad exposure) and analyzes four concerns, concluding crashes are inevitable but opportunities for patient investors.

Four Main Concerns

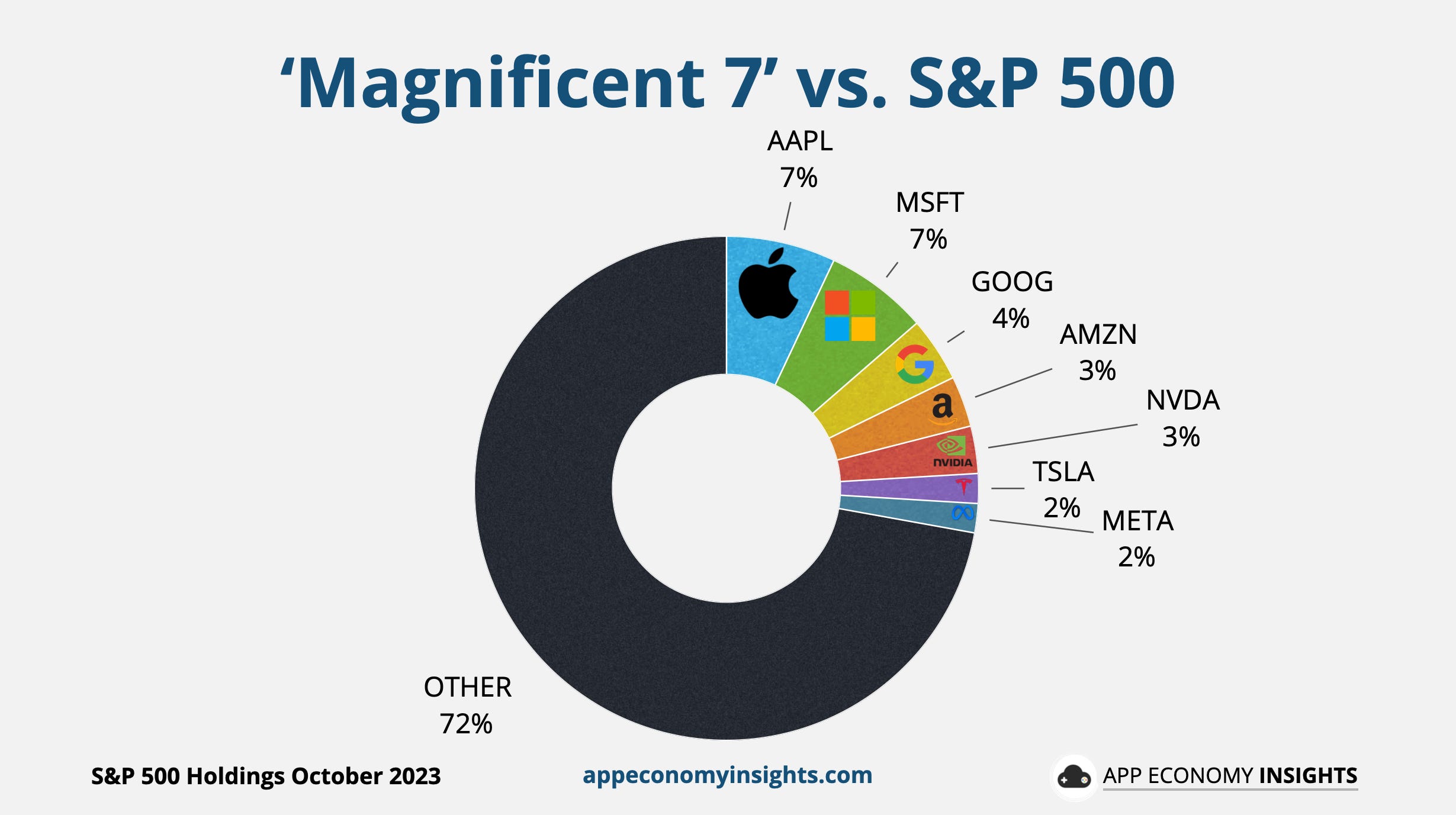

- Concentration Risk — "Magnificent 7" (Apple, Microsoft, Amazon, Alphabet/Google, Nvidia, Meta, Tesla) ~35% of S&P 500 (as of Dec 2025). Passive inflows disproportionately boost these, creating feedback: Rising prices → higher weight → more inflows → higher prices. If one falters (e.g., Nvidia miss), it drags the index.

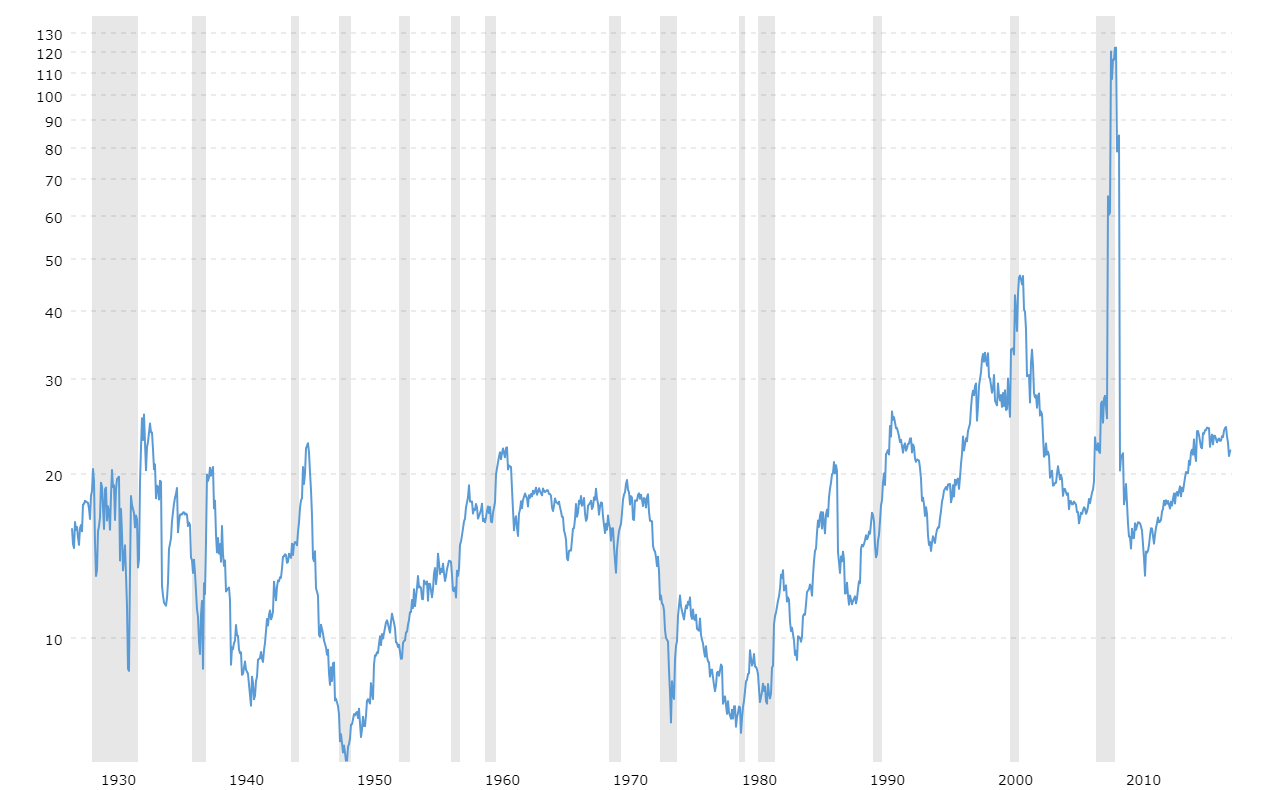

- Price Insensitivity — Passive investors buy the index regardless of valuation. S&P 500 trailing PE ~29–31 (Dec 2025), above historical ~20 average. Critics say overvaluation persists without scrutiny.

Insight/2020/03.2020/03.13.2020_EI/S%26P%20500%20Forward%2012-Month%20PE%20Ratio%2010%20Years.png)

- Asset Insensitivity — Funds buy everything (e.g., lesser-known #498–500 like Mosaic, Match Group), inflating prices of stocks that might not attract individual buyers.

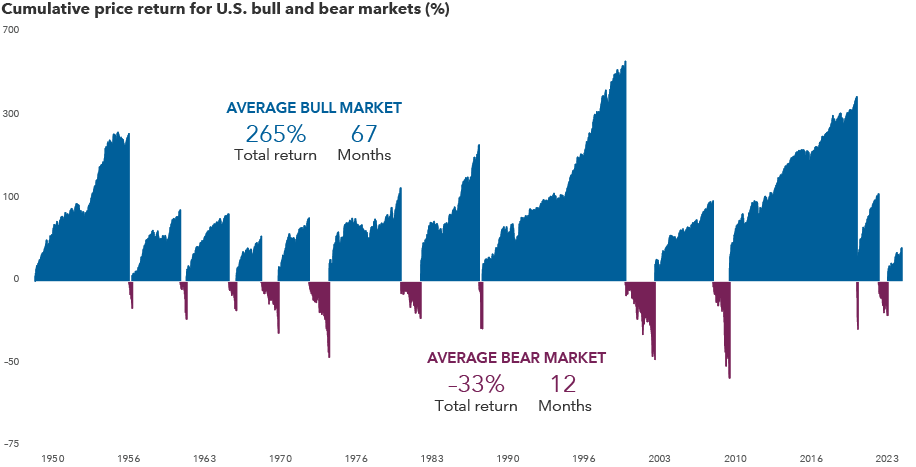

- Lack of Experience — Inexperienced investors panic-sell during downturns (buy high, sell low). Past crashes: 2022 (-20%), 2020 (-30%+), 2008 (-50%+), 2000 dot-com (Nasdaq -75%).

Even worst-timed buys (peaks) recovered long-term if held.

What This Means for You

- Bubbles/crashes/recessions are normal (~16 recessions, 25+ 20%+ crashes last 100 years).

- Alternatives to passive: Active (research stocks—higher effort/risk/reward), real estate/crypto/startups (riskier/work-intensive).

- Passive wins long-term via diversification/patience.

- Strategy: ABB (Always Be Buying) — Dollar-cost average consistently.

- POOP: Panic → Overselling → Opportunity → Profit. Crashes discount good assets; patient buyers profit on recovery.

Conclusion: Likely concentration/overvaluation issues, but passive indexing builds wealth historically. Stay educated, avoid panic—use downturns as buying opportunities. (Promotes free masterclass.)

(Word count ~880; estimated 8–10 minute read.)

15 Money Lessons from a 29-Year-Old with $450k+ Net Worth: How Early Decisions Built Freedom

At 29, content creator "Wiler" (computer science background, former engineer) shares how he built ~$450k+ net worth through disciplined habits in his 20s—not genius, high salary spikes, or luck. No inherited wealth; started near zero. These 15 lessons (hard-won from mistakes) emphasize mindset, ownership, and long-term compounding over quick wins. He wishes someone taught him this at 20 to avoid wasted years.

The 15 Lessons

- Society Owes You Nothing — No handouts; you're not "special." Take personal responsibility—learn skills, ask questions (after research), fight for opportunities.

- Be an Owner, Not a Consumer — Shift from spending (dollars gone forever) to owning assets (stocks, index funds, skills, business) that generate income. Early ownership = freedom.

- Track Your GAP (Income - Expenses) or Lose Everything — Awareness is key; log every dollar (rent, food, subscriptions). Small leaks ($19/week = $1k/year) sink ships.

- You Don’t Need a High Salary to Build Wealth — Habits > income. Consistent investing (even small) beats high earners who spend everything. Example: Janitor Ronald Read became millionaire via steady contributions.

- Starting Early Isn’t Optional — Compounding magic: $1 at 20 ≈ $22 at retirement. Early dollars multiply decades; procrastination costs most.

- Don’t Try to Get Rich Quick — Avoid scams (crypto pumps, options, NFTs). Quick wins skip character-building journey. Time in market > timing; dollar-cost average.

- Saving Money Won’t Make You Rich—Investing Will — Cash loses to inflation; invest savings (Roth IRA, etc.). Treasuries/money markets for short-term.

- The Best Investment Isn’t Stocks—It’s Skills — Upskill to raise income ceiling (his CS skills → high salary early).

- Learn to Sell and Communicate — Visibility/persuasion = money. Good communicators win promotions/business.

- Use Your Job to Win — Jobs as "launchpad" (money, skills, network). Don't hate—leverage.

- Lifestyle Inflation Is the Killer of Freedom — Upgrades delay independence. Stay cheap in 20s (lived basement/roommates despite 6 figures).

- Expect Slow Progress — Early investing boring/slow (ice cube analogy: heat builds invisibly before melt). Push through.

- Understand Taxes, Keep Your Money — Use Roth IRA/401k/HSA for tax advantages—saves hundreds of thousands long-term.

- You Don’t Have to Stay Poor — System rigged but beatable (online/AI opportunities). Grit + delusion wins; don't give up.

- Freedom Doesn’t Mean Retirement—It Means Options — Money buys time control, not endless stuff. Chase flexibility (he quit job for options).

His proof: Serious money focus in 20s = freedom/flexibility at 29. Simple rules, consistent action—no secrets.

(Word count ~920; estimated 8–10 minute read.)

How the Rothschilds Outplayed Napoleon: A Quiet Financial Victory That Built a Global Empire

This video narrates the lesser-known financial side of the Napoleonic Wars (1803–1815), focusing on how the Rothschild family—starting as modest merchants—created a private network that sustained Britain's war effort against Napoleon, shifting the conflict's balance and launching their rise to global financial dominance.

Origins and the Critical Need

The Rothschilds began in Frankfurt's Jewish ghetto. Mayer Amschel Rothschild built a coin/trade business based on discretion. He strategically placed his five sons in key European capitals: Nathan (London), James (Paris), Salomon (Vienna), Amschel (Frankfurt), Carl (Naples). This created a cross-border web unmatched by governments.

By 1813–1814, Britain faced crisis: Wellington's Peninsular War success stalled due to funding shortages. Napoleon controlled continental routes; gold (needed for local payments) couldn't flow reliably via official channels. Britain turned to private bankers—Nathan Rothschild's network proved ideal.

The Invisible Pipeline: How They Moved Gold

- Discreet Purchases: Gold bought in small lots across Europe (Amsterdam, Germany) to avoid suspicion.

- Covert Transport: Shipments disguised in ordinary trade (false-bottom crates, barrels). Couriers used merchant cover—less scrutinized than diplomats.

- Flexible Routes: Avoided blockades via Alps/southern paths; brothers coordinated reroutes.

- Speed & Reliability: Private riders faster than state messengers; network adapted to French patrols.

Result: Steady gold supply kept Wellington's multinational army (British, Portuguese, Spanish) paid/supplied—preventing desertion/collapse.

Human cost: Couriers risked robbery, arrest, death on dangerous roads. Brothers' letters show constant worry.

The Turning Point: Waterloo (1815)

Napoleon's return from Elba escalated urgency. Rothschilds raised massive funds quickly, suggesting practical solutions (e.g., melting bullion into coins). Their financing sustained ~209,000 coalition troops in Belgium.

Waterloo's military drama overshadows this: Without reliable pay, coalition might have fractured earlier. Rothschild support bought time for decisive battle.

Post-victory myths (Nathan profiting hugely from early news) are exaggerated/distorted; real advantage was pre-battle financing enabling Britain's endurance.

Post-War Expansion: From War Finance to Global Empire

Wars left Europe debt-ridden, currencies unstable. Rothschilds transitioned from wartime enablers to peacetime architects:

- Government Bonds: Coordinated massive issues across capitals—reliable when single-country banks faltered.

- Crisis Stabilization: 1825 UK banking panic—Nathan supplied critical gold to Bank of England, averting collapse.

- Industrial Finance: Funded railways (France, Austria, Germany), connecting economies.

- Resource Control: 1830—gained Almadén mercury mines (essential for gold/silver refining); 1852—took over London's Royal Mint Refinery amid California/Australia gold rushes.

Influence peaked mid-19th century: Stabilized markets, shaped infrastructure, controlled key bullion processes. Not "shadowy control"—practical solutions where governments lacked speed/coordination.

Modern Insights and Legacy

Recent research emphasizes:

- Information Edge: Couriers carried market/political data—real-time continental view via five-city network.

- Practicality Over Conspiracy: Success from speed, trust, adaptability—not manipulation.

- Enduring Model: Anticipated modern global finance (cross-border coordination, rapid response).

Legacy: Shaped bond markets, infrastructure finance, bullion standards. Private networks filled state gaps—relevant today in crises.

The Rothschilds didn't win battles but enabled victory by solving funding where empires couldn't. Their "empire" was financial infrastructure lasting centuries.

(Word count ~920; estimated 8–10 minute read.)

Home Buying Red Flags: A Realtor's Checklist to Spot a "Bad House" Quickly

In this practical video, New Jersey realtor Jackie Baker shares her step-by-step process for previewing homes with clients—helping first-time buyers (and anyone) identify major issues in ~60 seconds to minutes. Goal: Avoid "money pits" by spotting expensive repairs early. She emphasizes: No home is perfect, but multiple red flags = walk away. Always get a professional inspection (never waive); seller disclosures aren't 100% reliable.

1. Curb Appeal & Location (Drive-Up/Neighborhood)

- Street/Parking: Enough space for guests/entertaining? Driveway size adequate?

- Proximity Issues: Backs to highway, shopping center, warehouse/office (noise, privacy, resale value)?

- Neighbors: Poorly maintained yards/properties (potential ongoing disputes)?

- Overall Vibe: Safe, desirable street/location?

2. Exterior Walk-Around

- Roof: Moss, buckling, missing shingles, overhanging/tree-touching branches (expensive removal/replacement).

- Trees: Too close to house (root/foundation damage risk).

- Foundation: Cracks (vertical <1/8" often minor; >1/4" or horizontal/step cracks = serious structural concern—even if patched).

- Drainage: Pooling water near house (post-rain; grading issues → basement flooding).

- Chimney: Leaning, missing mortar/bricks.

- Pool (if present): Cracked coping/decking, old liner/equipment (liners ~$5k–10k+ replacement).

3. Interior Entry & Main Areas

- Floors (First Glance):

- Hardwood: Water stains, softening, holes/black marks (refinish/replace costly).

- Tile (ceramic/porcelain/marble): Cracks/broken pieces (removal/replacement very expensive—harder than wood).

- Walls/Ceilings: Water stains, patch jobs, large cracks (beyond normal settling).

- Windows: Single-pane/old, hard to open/close (full replacement costly).

4. Key Systems & Mechanicals

- Fireplace: Wood-burning unused long-term? (Moisture damages liner—needs inspection).

- Electrical Panel: Low amperage, overloaded (wires everywhere), old/unsafe brands (upgrade $5k+).

- Furnace/Heating: Corrosion/rust on valves/pipes (poor maintenance = shorter life).

- Water Heater: Age (check install date; 10–12 years max life → imminent $2k–5k replacement).

- Central AC: Outdoor condensers rusted/weathered (older unit → soon replacement).

5. Bathrooms/Kitchen & Hidden Spots

- Under Sinks: Leaks, mold (past plumbing issues).

- DIY Work: Shoddy/slopy repairs (uneven tile, poorly installed fixtures → full redo needed).

6. Basement (Especially Unfinished)

- Moisture Signs: Multiple dehumidifiers running, water lines/stains on walls, musty smell.

- Foundation (Interior): Matching exterior cracks (soil pressure/shifting).

Key Takeaways & Advice

- Multiple Flags = Bad House: 3+ issues often mean walk away (cumulative costs skyrocket).

- Seller Disclosures: Review pre-viewing but don't fully trust—not all honest.

- Agent's Role: Good ones spot these; ask questions if issues hidden.

- Always Inspect: Never waive—even if checklist clear.

- Mindset: Avoid money pits over "perfect" home.

Jackie stresses quick scans reveal deal-breakers; focus on big-ticket items (roof, foundation, mechanicals, water damage). Promotes connecting viewers to local agents.

(Word count ~850; estimated 8–10 minute read.)

Why Leverage Is the Silent Killer of Wealth: The One Mistake Smart People Keep Making

This reflective essay warns that intelligent, successful people most reliably destroy wealth through leverage (borrowed money)—not poor investments or bad luck. "There are only three ways a smart person can go broke: liquor, ladies, and leverage." The first two are alliteration; leverage is the real threat. It turns temporary declines into permanent ruin via simple math, psychology, and history. Unleveraged losses are survivable; leveraged ones multiply to zero (or worse).

The Math: Leverage Creates Zeros

- Without leverage: Worst case = lose invested amount (e.g., $100k → $0 = -$100k loss; recovery possible).

- With leverage: Declines trigger margin calls → forced selling at lows → total wipeout (or debt).

- Markets routinely drop 30–50%+ (Berkshire Hathaway: 50%+ declines 4 times despite legendary performance).

- Example: 2:1 margin on a 50% drop = 100% loss + potential owed money.

- Key asymmetry: Gains capped by realistic returns; losses unlimited (exceed everything owned).

"Any string of positive numbers multiplied by zero = zero." One leveraged blow-up erases decades of gains.

Historical Catastrophes: Smart People Destroyed by Leverage

- 1929 Crash: 10% margin ($10 down → $100 stock) → 10% drop wiped equity; cascading forced sales caused spiral.

- Led to margin regulations (Fed authority to limit leverage—used wisely until weakened).

- Long-Term Capital Management (1998): 16 brilliant minds (2 Nobel economists, 350–400 years experience) → $4.6B fund.

- 25:1+ leverage ($125B assets on $5B equity).

- Russia default → positions collapsed; $4.6B lost in months; Fed-orchestrated bailout.

- Lesson: Genius + models irrelevant; leverage forces exit at worst time.

- Archegos Capital (2021): Bill Hwang → $20B lost in days via 5:1+ leverage (total return swaps—off-books).

- Banks (Credit Suisse -$5.5B) enabled for fees; short-term profits blinded risk controls.

Pattern: New instruments (swaps vs. old margin) bypass rules; each generation thinks "this time different."

Everyday Leverage: Consumer Debt as Slow Suicide

- Lifestyle debt (credit cards 18%+) compounds against you.

- $10k debt @18% (minimum payments) → ~$30k paid over 25 years.

- Same $10k invested @8% → ~$70k.

- Lifetime difference: ~$100k lost opportunity from one decision.

- Inflation + debt = compounding enemy.

Exception: Sensible fixed-rate mortgage (non-callable; affordable payments).

Psychology: Why Smart People Fall

- Overweight gains, underweight losses.

- Envy ("neighbor richer via leverage").

- Recent bias ("bull market = permanent").

- Overconfidence ("I'll exit before crash").

- Fees lure enablers (banks collect upfront; pain later).

Inversion: Avoid Going Broke

List wealth-destroyers; don't do them:

- Borrow for declining assets.

- Confuse bull markets with skill.

- Assume future = recent past.

- Bet irresponsibly with dependents.

- Think you're exception.

"Goal: Get rich permanently, not quickly." Survival > maximization.

Patient Alternative Wins

- 8% steady compounding: $100k → $1M+ in 30 years (no brilliance needed).

- Leveraged chase (15% short-term) → inevitable wipe-out.

- "Sit on assets" = sophisticated (low fees/taxes, no whipsaw).

Personal note: Author references profound loss (implied Charlie Munger-like story: divorce, child death, poverty) → rebuilt without leverage. Warnings carry weight from bottom.

Final truth: Avoid stupidity > chase brilliance. Discipline + humility + no leverage = reliable wealth.

(Word count ~920; estimated 8–10 minute read.)

7 Things the Bible Says You Should Keep Quiet About for Financial Prosperity

This faith-based video from "Biblical Finances" teaches that careless words can sabotage success. Drawing from Scripture, it lists seven things to guard closely—not out of secrecy or pride, but wisdom, stewardship, and protection. Oversharing invites criticism, envy, doubt, or interference that disrupts God's process. True prosperity grows in quiet obedience.

1. Don't Share All Your Plans Prematurely

Excitement leads many to broadcast ideas/projects early. But Proverbs 15:22 warns plans succeed with wise counsel, not crowds.

- Early exposure invites doubt/criticism that weakens faith.

- Biblical examples: Joseph (dreams → betrayal), David/Jesus (prepared privately).

- Silence protects focus/discipline; let results speak.

Wise: Build first, announce later.

2. Don't Reveal Your Exact Income

Cultural norm to discuss earnings, but biblically risky (Proverbs 11:13—faithful spirit conceals matters).

- Sparks envy, expectations ("obligation" to help), or judgment.

- Matthew 6:3—give secretly to preserve humility/peace.

- Public income → decisions for appearances, not conviction.

Quiet prosperity lasts longer; avoids external pressures.

3. Don't Disclose Your Specific Financial Strategies

Share principles, not personal moves (investments, contacts, plans—Proverbs 27:12: prudent hide from danger).

- Exposes to copying, competition, or interference.

- Luke 14:28—calculate costs privately.

- Wrong ears bring distraction/opinions from limited experience.

Safe progress built in private with God/wise counsel.

4. Don't Share All Your Inner Struggles

Oversharing vulnerabilities common today, but Proverbs 4:23—guard heart above all.

- Wrong people judge/give ungodly advice.

- Psalm 42:5—David spoke to self/God first.

- Public battles invite weaponized weakness.

Process privately with God; protects focus/faith.

5. Don't Announce Prosperity Too Soon

Premature celebration risky (Genesis 37: Joseph’s dreams → rejection/pain).

- Invites envy, pressure to spend for appearances.

- Ecclesiastes 3:7—time to speak/silent.

- Ego inflation or social demands erode gains.

Blessings mature privately; solid when revealed.

6. Don't Share Goals with Negative People

Not all have faith/vision (Proverbs 13:20—walk with wise).

- Negative voices project fear/frustration, weaken motivation.

- Numbers 13—spies' doubt blocked Promised Land.

- Unbelief "extinguishes" vision.

Surround with faith-adders; protect goals' "soil."

7. Don't Share Everything You Know

Wise store knowledge (Proverbs 10:14); fools' mouths invite ruin.

- Oversharing invites criticism/manipulation.

- Matthew 27:14—Jesus silent before accusers.

- No need to prove superiority.

Strategic silence = self-control/leadership. Faithful stewardship > boasting.

Core Message: Silence as Stewardship

These aren't manipulative secrecy—protection for God's work. Oversharing interferes with process (Luke 16:10—faithful in little). Guard mouth/heart; manage quietly. God blesses stewards, not announcers.

Video calls for subscription, comments on resonant point.

(Word count ~880; estimated 8–10 minute read.)

From $0 to $125k Invested by Age 26: My Step-by-Step Journey and Key Habits

In this motivational YouTube video, a 26-year-old content creator shares his real, unglamorous path to building a ~$125k investment portfolio starting from zero at age 21. No windfalls, high salaries (started ~$55k/year), or lucky trades—just disciplined habits, learning from mistakes, and long-term focus. He emphasizes: It's not about genius; it's consistency and avoiding traps. If you're in your 20s struggling to save/invest, his story shows it's possible with smart choices.

The Starting Point: COVID Chaos and Rookie Mistakes (2020)

His journey began March 2020—peak pandemic, market crash (~30% S&P 500 drop). About to graduate college, he dove in ignorantly:

- Options Trading (1–2 Months): Gambled on short-term bets—"loser's game." Lost money quickly.

- High-Yield Dividends (May–June 2020): Chased "15% yields" on risky stocks. Realized prices dropped, eroding value—"too good to be true."

By July 2020, frustrated with minimal gains despite market rebound, he switched strategies.

Evolution to Dividend Growth Investing (July 2020–2024)

Focused on companies with low initial yields (2–3%) but strong dividend growth (10–20%+ yearly) + stock appreciation. Key picks:

- Microsoft: $5,244 invested → $143 dividends + sold $9,453 (big winner, started early 2020).

- Costco: $4,391 → $151 dividends + sold $6,734.

- JP Morgan: $3,012 → $325 dividends + sold $6,025.

Underperformers (no losses, but lagged S&P 500): Vici Properties, Realty Income, Domino's Pizza.

Gradually added ETFs for diversification:

- Built habit of monthly investments (started $25–$75, grew to thousands).

Recent Portfolio Overhaul (2025)

Realized individual stocks underperformed S&P 500 (e.g., market +24% vs. his +18–20%). Shifted to passive, simplified mix:

- 70% VOO (S&P 500 ETF—broad market exposure).

- 20% SCHD (Schwab dividend growth ETF).

- 10% VUG (Vanguard growth ETF—tech-focused).

Current breakdown (~$125k total):

- Brokerage/Roth IRA: ~$100k.

- 401(k): ~$24k.

Annual investments scaled: $8k (2022) → $22k (2023) → $28k (2024) → $24k YTD (2025)—averaging ~$2,900/month (~$35k/year).

Habits That Made the Difference

Success wasn't strategy alone—rooted in frugal, disciplined lifestyle enabling high savings (while income grew from $55k → higher via job/remote work).

- Live Below Your Means: Extreme frugality early (March 2022–Feb 2023: Saved for house). Drove 2006 Camry (paid cash, still owns). No designer clothes/flexing. Apartment: Bed, dresser, desk only—no couch/TV (ate/worked at desk).

- Expenses: ~$950 rent + utilities (~$90/month total).

- Track Income/Expenses Religiously: Knew exact costs (e.g., water $20–30). Avoided leaks; focused surplus on investing.

- Avoid Debt Traps: No credit card debt/loans—lived cash-based.

- Patience & Long-Term Mindset: Portfolio flat 12+ months (2021–2022) despite deposits—didn't panic. Increments accelerate: $0–$10k slow; $100k–$125k < months.

- Dips = opportunities: "Buy discount" vs. panic (e.g., 2022 flat despite $8k invested).

- Scale Investments Gradually: Started small ($25–$75/month) → built habit → larger as income grew (expenses flat).

Lessons & Encouragement

- Start Small: Doesn't matter if $10–$50/month—habit compounds (e.g., his early $200–$430 deposits snowballed).

- Time in Market > Timing: Even bad timing recovers long-term; consistent buys win.

- It's Never Too Late: Best time: Today; next: Tomorrow.

- Balance Life: Frugality temporary—not forever. Enjoy once stable.

He's launching "Road to $200k" series: Monthly updates, goals (e.g., $40k invested 2025). Focus: Big-picture thinking—$125k could 2–4x in 5–20 years without more deposits.

Message: Discipline > luck. Avoid short-term traps; build habits for acceleration.

(Word count ~850; estimated 8–10 minute read.)

China's Escalating Internet Crackdown: Toward a Tighter Digital Control Ahead of 2027

In late November 2025, the Chinese Communist Party (CCP) Politburo held its 23rd collective study session on "strengthening the governance of the internet ecosystem." Presided over by President Xi Jinping, the session signaled a major escalation in China's approach to online control. Xi emphasized creating a "clean and upright cyberspace," combating "online chaos" driven by profit-seeking, and using artificial intelligence (AI) as a tool for governance. He called for "daring to show the sword" against disruptions, cutting off "interest chains" behind sensationalism and rumors, and integrating AI to enhance predictive control. This meeting is widely interpreted as a turning point, framing the internet not just as a platform to manage but as a critical arena tied to national security and regime stability.

The timing is no coincidence. With the 21st Party Congress scheduled for 2027—where Xi is widely expected to secure an unprecedented fourth term—narrative control is paramount. Authoritarian leaders rarely fall due to formal processes but from losing grip on public perception. Shared doubts or alternative stories can erode legitimacy. To prevent this, the CCP is intensifying measures to starve society of unapproved information, amplifying official voices while suppressing others. This builds on longstanding controls but marks a more comprehensive, preemptive phase, leveraging technology to foresee and neutralize potential threats.

Key Mechanisms of the Crackdown

The strategy employs multiple interlocking tools to dominate information flow:

- AI-Powered Surveillance and Predictive Censorship AI is now central to monitoring images, videos, comments, and even private messages. Systems in some provinces enable real-time censorship, flagging content based on tone, mood, or potential to mobilize opinion. This goes beyond reactive deletion to proactive intervention—detecting "clouds that might become storms." Xi has positioned AI as essential for regime support, enabling governance to anticipate dissent before it forms.

- Algorithmic Control Platforms must align recommendation systems with "mainstream values," requiring regulatory approval for algorithms that influence public opinion. Propaganda gets amplified, emotional or critical content is throttled, and dissenting narratives rarely trend. This subtle burial of ideas eliminates the need for outright bans; unwanted content simply fails to reach audiences.

- Real-Name Verification and Identity Linkage All social media accounts are tied to real identities via phone numbers, IDs, and facial recognition. By 2025-2026, platforms must deny service to unverified users. This eradicates anonymity, allowing rapid identification and punishment for sensitive posts, extending accountability to the physical world.

- Expanded Monitoring of Private Spaces Group chats and one-on-one messages (e.g., on WeChat) face increased scrutiny, with embedded censorship interfaces and human reviewers during sensitive periods. Private communication is no longer safe, fostering widespread self-censorship as silence becomes the default.

- VPN Restrictions Unauthorized VPNs remain heavily restricted, with ongoing blocks and warnings against circumvention. While not fully banned, enforcement tightens, sealing cracks in the Great Firewall and limiting access to global information.

- Targeting Independent Voices and the Influencer Economy "Self-media"—independent creators on platforms like Weibo, Douyin (TikTok), and WeChat—are prime targets. Recent 2025 regulations require verified professional credentials (degrees or certifications) for discussing sensitive topics like finance, health, law, or education. Influencers spreading "pessimism" (e.g., on economic woes, low birth rates, or work-life balance) have faced account bans. This disrupts monetization, closes live-stream hubs, and preemptively neutralizes those with mobilization potential, even if non-political.

Broader Implications: A "Digital Winter"

The cumulative effect is a chilling of online discourse. Users increasingly avoid debate, hints, or risks, leading to what critics call a "digital ice age." Independent income streams for creators are drying up, grassroots mobilization is stifled, and society is isolated from external comparisons.

Historically, tightenings occur before major events (e.g., 2022 Congress). But this phase appears more systemic, aiming for long-term dominance ahead of 2027. While blocking information is feasible with advanced tech, sustaining legitimacy without genuine public buy-in remains challenging. Critics warn of parallels to highly isolated systems, though China's scale and economic integration make a full "digital North Korea" unlikely in the near term.

This crackdown reflects Xi's view of the internet as a "battlefield" for survival—prioritizing control over openness to secure his legacy and the CCP's rule. As 2027 approaches, expect further refinements to ensure a flat, visible, and silent digital landscape.

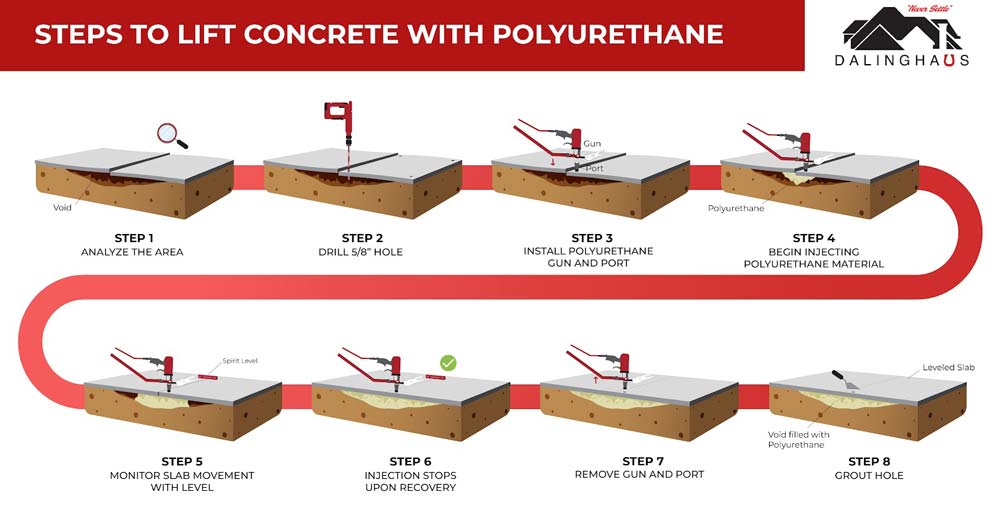

A Low-Overhead, High-Profit Home Service Business: Polyurethane Concrete Leveling

Concrete leveling (also called concrete raising or polyjacking) uses expanding polyurethane foam to lift and stabilize sunken slabs like driveways, sidewalks, patios, and pool decks. This method fixes tripping hazards, improves aesthetics, and prevents water pooling at about one-third the cost of full replacement. In sprawling areas like Texas (especially Houston and Dallas-Fort Worth), expansive clay soils and heavy concrete use create constant demand.

The video features Jeff, owner of Texas Slab Guys, who launched his business in mid-2025. With no prior industry experience, a full-time W2 job, a wife, and two kids, he generated nearly $20,000 in revenue in his first 90 days (mostly in the last 60), with 30-40% gross margins. He projects $250,000 in revenue by year-end (potentially $50-100k profit) and $1 million next year at 20-40% margins.

Why This Business Model Works So Well

- High demand — Sunken concrete is common due to soil settlement, tree roots, or poor drainage.

- Premium pricing — Jobs average $2,500 revenue, with $800-1,000 profit per job.

- Low ongoing overhead — No employees needed; subcontract the physical work.

- Quick jobs — Most complete in hours, with foam curing in 15 minutes (drive-on ready immediately).

- Scalable — Remote/virtual quoting allows handling many leads without site visits.

- Differentiation — Focus on quality, communication, and extras like free power washing.

Jeff's approach: Subcontract to experienced operators (often veterans who own equipment), handling sales, quoting, and customer relations himself.

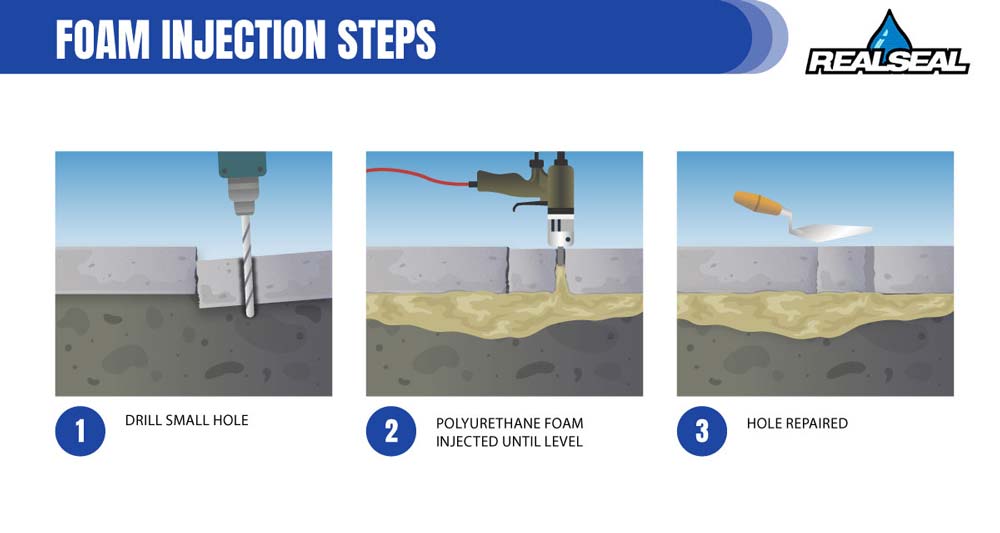

How the Process Works

- Drill small (dime-sized) holes in the slab.

- Inject two-part polyurethane foam (A + B components) via a heated hose and gun.

- Foam expands rapidly, filling voids, compacting soil, and precisely lifting the concrete.

- Patch holes (nearly invisible on unstained concrete).