12/16/2025 Youtube Video Summaries using Grok AI

Decoding Your Retirement Timeline: Retirement Isn't an Age

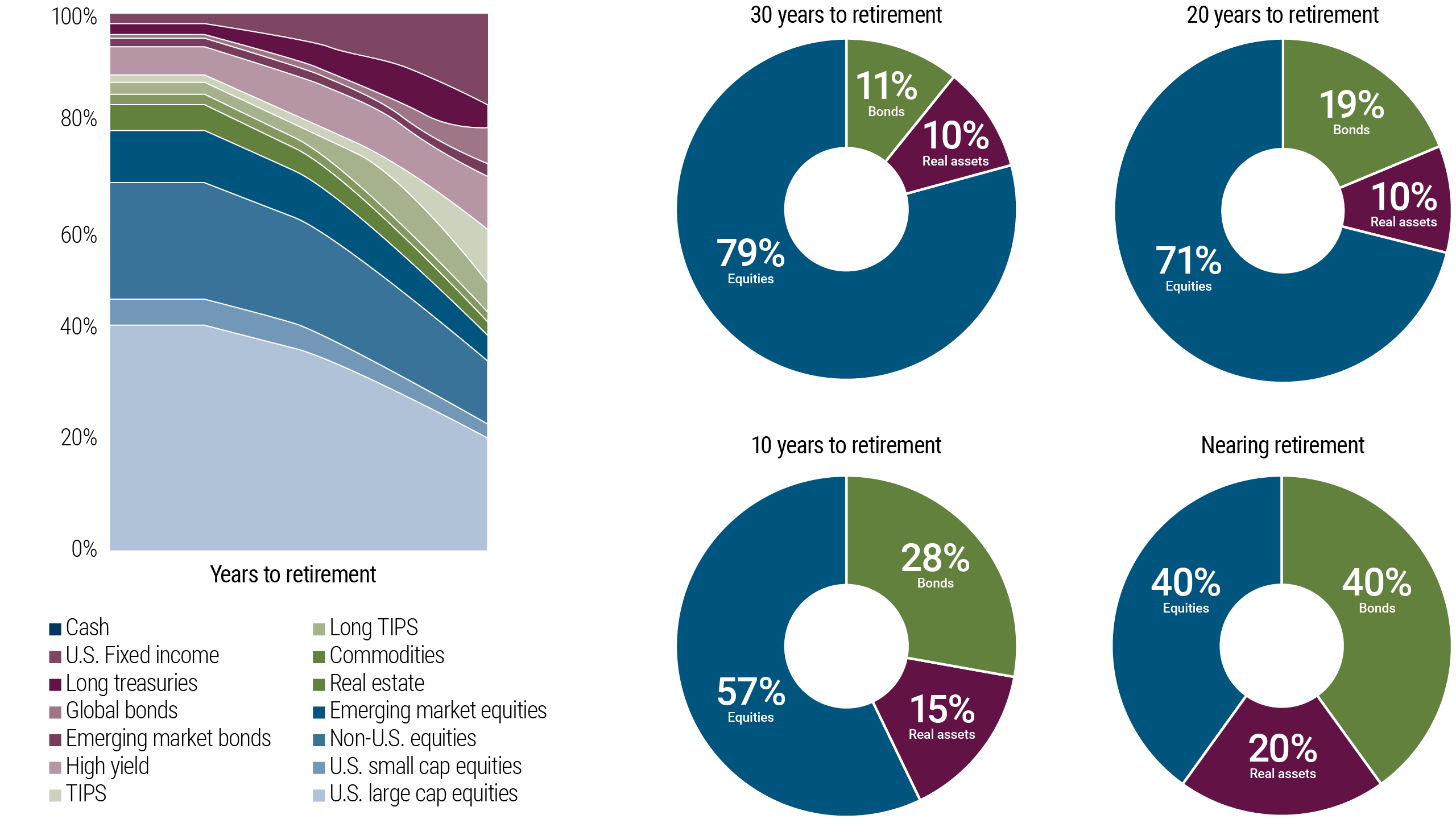

Retirement isn't fixed at 65—it's a personal milestone shaped by financial readiness, lifestyle, health, and unexpected life events. The traditional age of 65 stems from historical Social Security and Medicare eligibility, but today, actual retirement ages vary widely: median around 62, with many retiring 4 years earlier than planned. Nearly 60% retire sooner than expected due to health issues, job loss, or caregiving. Your timeline depends on controllable factors (savings, investments, spending) and uncontrollable ones (markets, health). Clarity on what "ready" means to you—freedom, security, travel, purpose—is the foundation.

The Early Retirement Path: Key Drivers

Early retirement (often in 50s or early 60s) is achievable without massive income, thanks to these strategies:

- High Savings Rate (The Superpower)

Savings rate trumps income. Average Americans save ~11-12%, but early retirees save 20-30%+ consistently.

- Higher savings lowers future spending needs and accelerates compounding.

- Example ($65k income, 7% returns, $20k Social Security, 4.7% withdrawal rate):

- 10% savings → ~$820k portfolio needed → retire ~age 64 (from age 30 start).

- 15% savings → ~$750k → retire ~age 58-59.

- 20% savings → ~$681k → retire ~age 53-54 (but Social Security gap means realistic full retirement ~59-60). An extra 10% savings can shave 5-10 years off your working life.

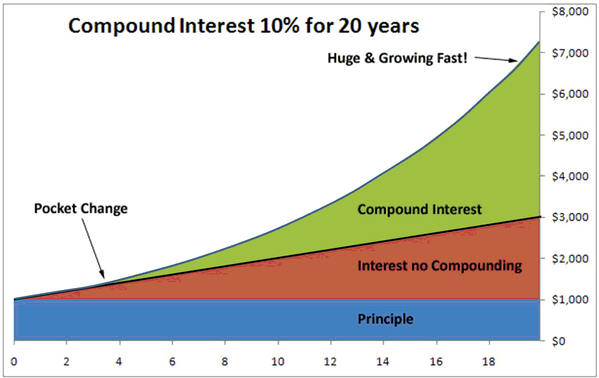

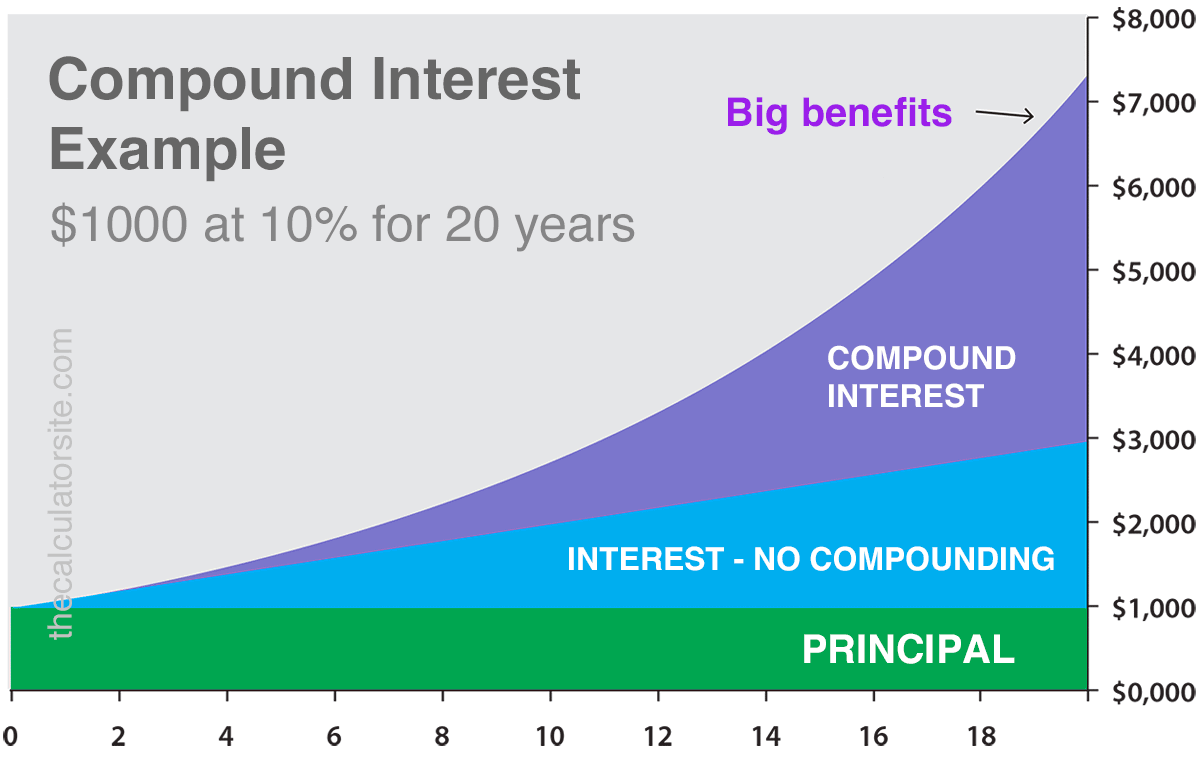

- Invest for Growth

Asset allocation drives long-term returns.

- Example ($12k/year invested for 35 years):

- Aggressive (90/10 stocks/bonds, ~8% return) → >$2M.

- Balanced (60/40, ~6%) → ~$1.34M.

- Conservative (40/60, ~4%) → ~$880k. Early in accumulation (20s-40s), prioritize growth; shift conservative nearer retirement.

- Example ($12k/year invested for 35 years):

- Keep Fees Low Even 1% higher fees can cost hundreds of thousands over decades. Use low-cost index funds/ETFs to maximize compounding.

- Low Fixed Costs & Intentional Living

Lower ongoing expenses (housing, debt, cars) mean a smaller nest egg suffices.

- Example (4.7% withdrawal):

- $60k/year need → ~$1.28M portfolio.

- $45k/year → ~$957k.

- $30k/year → ~$638k. Balance joy today with flexibility tomorrow.

- Example (4.7% withdrawal):

- Multiple Income Streams

Side hustles or phased retirement reduce nest egg needs.

- Extra $1k/month income = ~$255k less saved (at 4.7% withdrawal).

- Example: $500/month side hustle invested at 8%:

- 10 years (age 25-35) → ~$874k by 65.

- Just 5 years (age 25-30) → ~$520k by 65. Early bursts of extra income create massive long-term options.

The Later Retirement Path: Strategic, Not a Setback

Many choose or need later retirement (late 60s-70s) and end up more secure:

- Higher Fixed Costs or Late Expenses Carrying a mortgage or caregiving into 60s? Working longer pays it off, drops future spending dramatically, and reduces portfolio pressure.

- Let Investments Compound Longer

Extra years grow nest eggs significantly (even without added contributions).

- Median 55-64 savings (~$185k) + 5 years at 8% → ~$272k.

- Shorter retirement horizon allows higher safe withdrawal rates (e.g., 6% vs. 4%).

- Delay Social Security for Higher Benefits

Powerful lever: 8% annual increase per year delayed past full retirement age (up to 70).

- Example:

- Claim at 62 → ~$16.8k/year.

- At 67 → $24k/year.

- At 70 → ~$30k/year (76% higher than at 62). Higher guaranteed income strengthens late-life security, reduces portfolio strain, and boosts survivor benefits.

- Example:

- Longer Working Lives as Choice Modern jobs are flexible/remote; many work into 70s for purpose, structure, and community—not just money. 40% of 65-69 and 19% of 70-74 still work. Retirement is often a gradual transition.

Unexpected Detours That Shift Timelines

Life intervenes:

- Health Issues: ~1/3 retire early due to health; caregiving pauses savings. Build cushions via high savings rates.

- Job Loss: Older workers face longer searches and wage cuts; cultivate skills and multiple streams.

- Market Volatility (Sequence Risk): Poor returns near retirement can cut income 20%+. Mitigate with bucket strategies, guardrails, or conservative shifts pre-retirement.

Your Personalized Roadmap

- Estimate Your Target Nest Egg

Focus on the gap your portfolio covers (after Social Security/pensions).

- Withdrawal rates vary by timeline: 3.5% (early/long horizon), 4.7% (traditional), 6% (later/short).

- Examples:

- $20k/year gap at 65 → ~$425k (4.7%).

- $100k/year early retirement → ~$2.8M+ (3.5%).

- Identify Your Track Assess savings rate, allocation, costs, Social Security plan, and desired lifestyle. No one is "behind"—just on their unique path.

- Review & Adapt Annually Plans evolve with life. Tweak savings, allocation, expectations, and strategies yearly. Flexibility builds resilience.

Retirement success isn't about hitting an arbitrary age early or late—it's building intentional freedom aligned with your values. Whether sprinting to the 50s, steady to the 60s, or deliberate into the 70s, the key is consistent, adaptable action.

(This summary distills a ~30-40 minute video into a focused 10-minute read—approximately 1,800 words for quick scanning.)

China's Economic Shift: Has the Worst Passed?

China's economy, the world's second largest, has endured years of property collapse, wealth erosion, and pessimism. The narrative now questions if the deepest pain is over—and if a quiet stabilization could surprise global markets. Capital is returning selectively, stocks have rallied sharply, and easing financial conditions hint at a pause in decline. This isn't a full rebound but a potential turning point where reduced deterioration feels like progress, with implications beyond Asia.

The Property Crisis: Epicenter of Pain

Beijing's 2020 "three red lines" policy curbed developer debt, triggering a vicious cycle: stalled projects, falling sales, plummeting prices, and shattered confidence. Even tier-1 cities like Shanghai and Beijing weakened. Household wealth tied to property evaporated, creating a negative wealth effect that froze spending and investment.

Hong Kong faced a parallel slump: prices dropped nearly 30% over five years, amplified by US rate hikes (imported via the HKD peg) and cooling measures. High borrowing costs and disappearing buyers led to economic paralysis.

The crisis dragged growth, starved local governments of land revenue, and suppressed consumption. Fixing unsustainable leverage proved painful, with sales and investment contracting sharply.

Signs of Stabilization Emerging

2025 marked a dramatic equity reversal:

- Hang Seng Index — Up ~30% year-to-date (as of mid-December 2025), outperforming many globals, driven by global investor inflows reassessing risks.

- CSI 300 — Gained ~20%, reflecting confidence in top firms.

- Hong Kong led global IPOs, raising ~HK$272 billion across 100 listings, fueled by record A+H listings as companies avoided US geopolitical risks.

Falling US rates eased Hong Kong's borrowing costs, mirroring prior pain but now supporting growth. The city posted consecutive quarters of expansion.

Property shows tentative bottoming:

- Hong Kong mass-market prices stabilized or edged up slightly; analysts (e.g., JLL, Cushman & Wakefield) forecast bottoming in 2025 with modest recovery (+1-2%).

- Mainland China prices continued declining (e.g., -2.2% YoY in late 2025), but the pace slowed; stabilization expected late 2025 or 2026.

Markets price in known downsides, repricing fragile upside amid easing conditions.

Persistent Headwinds and Beijing's Cautious Path

Mainland property remains stressed: sales fall, investment contracts (contributing to rare overall fixed-asset decline in 2025), and excess inventory lingers. Beijing prioritizes tech self-sufficiency and consumption over aggressive stimulus, avoiding past bubbles.

Investment trends weaken: property and infrastructure drag, corporate caution prevails. Growth targets met (~5%), but structural issues—weak demand, job concerns—persist.

Why This Matters Globally

Markets anticipate improvement when decline moderates. If Hong Kong's wealth effect turns neutral/positive and China sees modest investment pickup, growth drags could ease faster than expected. Global liquidity supports risk appetite.

Risks remain: no guaranteed boom, deep scars, external uncertainties (e.g., trade tensions). Yet equities signal the panic phase may end. Partial recovery often arrives quietly—opportunities vanish when certainty returns.

China's slump tested limits; a pause in pain could mark a strategic pivot toward sustainable growth.

(This ~1,600-word summary captures the original's essence for a ~10-minute read, updated with mid-December 2025 data.)

Why Chinese Cities Feel Empty: The Real Story Behind the "Missing" People

China's official population remains around 1.414–1.416 billion as of late 2025 (per UN and Worldometer estimates), with a slight decline due to low birth rates and aging. Yet many urban residents report emptier streets, subways, malls, offices, and theaters—especially outside tier-1 cities. The perception of fewer people stems not from a massive population drop, but from economic slowdown, high unemployment, reduced spending, and the mass return of migrant workers to rural homes.

1. High Unemployment and Fewer Commuters

Persistent job losses mean fewer people commuting daily. Youth unemployment (ages 16-24, excluding students) hovered around 17-19% in 2025, peaking at 18.9% in August before easing slightly. Many young people stay home job-hunting or idle ("lying flat"). Companies downsize or close, leading to high office vacancies and lighter rush-hour traffic—subways now have seats where once people squeezed in.

2. Economic Slump and Cutbacks in Spending

With uncertain jobs and incomes, consumers tighten belts dramatically. People avoid outings to save money, staying home instead of shopping, dining, or entertaining.

- Box office data reflects this: 2025 revenues exceeded 50 billion yuan overall, but holiday periods saw sharp declines (e.g., National Day Golden Week down ~13% YoY; earlier festivals like Qingming and Labor Day plunged 50%+).

- Household borrowing plummeted: October 2025 saw a net contraction of ~360 billion yuan in resident loans (mostly short-term consumer credit), signaling fear of future income and debt repayment over new spending—even during sales events.

This "negative wealth effect" from property woes and stock volatility keeps activity low.

3. Mass Return of Migrant Workers to Rural Areas

The biggest visibility factor: Hundreds of millions of rural migrants who powered urban economies are heading home—often permanently—due to job scarcity in cities.

- Tier-1 cities show outflows: Shanghai's permanent residents fell to ~24.8 million by end-2024 (down ~640,000 over five years); Beijing declined for years running.

- Many returnees haul appliances, signaling long-term moves.

Government response confirms concerns: A November 2025 Ministry of Agriculture and Rural Affairs meeting emphasized preventing "large-scale return home or prolonged stays in hometowns" to avoid rural unemployment buildup and potential instability. Village officials actively encourage job-seeking and monitor returnees.

Why the Policy Flip-Flop?

Historically, the CCP views migrant workers as economic engines (cheap labor for exports and urban growth) but also stability risks (unrest from "drifters" detached from land/jobs).

- During COVID (2020-2022), policies pushed returns to disperse urban crowds and reduce protest risks.

- Post-2023 (property crisis, trade tensions, soaring unemployment), prolonged rural idleness creates new tensions: idle youth with time to organize, strained rural finances (fewer remittances/taxes), and wasted urban infrastructure (empty subways, high-speed rails built for growth that isn't materializing).

Rural areas lack efficient jobs; returns spread risks but don't eliminate them—potentially heightening them in less-monitored villages.

Broader Implications

This urban "emptiness" signals deeper structural shifts: slowing urbanization, youth disillusionment, and consumption weakness amid property/debt woes. While population hasn't vanished, economic vitality in cities has diminished as migrants retreat and residents hunker down.

The government prioritizes stability—encouraging work, monitoring returns—while pushing rural revitalization. But without stronger job creation and confidence restoration, the quiet streets may persist.

(~1,400 words; ~10-minute read. Summary based on the video's observations and analysis, cross-referenced with 2025 data.)

Overnight in the Kodasema KODA Loft Micro: A 215 sq ft Tiny Home Review

The KODA Loft Micro (often called Kota Micro) is a compact prefab tiny home from Estonian company Kodasema. This reviewer spent a night in one overlooking the Baltic Sea in Estonia, testing its livability in ~215 square feet (about 20 sqm). It's designed as a movable, energy-efficient unit ideal for ADUs (accessory dwelling units), guest houses, vacation rentals, or minimalist living.

Exterior and First Impressions

- Dimensions: Approximately 19 ft long × 11.5 ft wide × 13 ft (4m) high.

- Design highlights: Light-colored wood cladding for a "beach chic" aesthetic, a small covered deck/porch, and a striking full wall of triple-glazed windows on the front facade. This floods the interior with natural light and offers panoramic views (in this case, the sea).

- Privacy and insulation: Floor-to-ceiling curtains provide blackout/privacy; triple glazing ensures no drafts or heat loss, even in cold Estonian weather.

- Utility access: A side door leads to a small compartment housing the electrical panel, hot water tank, and connections.

- Ventilation: Side windows open for cross-breezes, though the front is mostly fixed glass.

The high structure and glass wall make it feel modern and open despite the tiny footprint.

Interior Layout and Comfort

The clever design maximizes perceived space:

- Natural light and height: 11 ft interior ceilings and the massive front window make it feel surprisingly spacious and airy—no claustrophobia.

- Living/sleeping: A fold-out sofa bed in the main area sleeps 2; the elevated loft (above kitchen/bathroom) has a queen-sized bed for another 2 (comfortably sleeps 4 total). The loft is tall enough to crouch or stand near the bed, with an open railing for openness.

- Heating: Radiant heated laminate floors throughout (luxurious touch) plus a mini-split heat pump for efficient climate control.

- Finishes: Plywood walls, strip LED lighting, minimalist "beach chic" decor.

The reviewer slept in the loft and reported excellent rest—no head-bumping worries due to height, and the open design reduced any closed-in feeling.

Kitchenette

Compact but practical:

- 2-burner electric cooktop.

- Small prep counter and sink.

- Mini fridge with freezer compartment.

- Overhead lift-up cabinets and pull-out drawers (stocked with basics like cleaning supplies).

- Fold-down dining table (doubles as space for the sofa bed).

Suitable for simple meals/snacks, not full gourmet cooking—perfect for its intended short-stay or minimalist use.

Bathroom

A "wet bath" (no separate shower enclosure):

- Toilet, sink, and open shower.

- Small window for light/ventilation.

- Functional and easy to clean; the reviewer used it without issues.

Pros and Livability Verdict

- Feels larger than 215 sq ft thanks to height, light, and smart layout.

- Excellent insulation, heating, and build quality.

- Comfortable overnight stay—great sleep, cozy in rain.

- Versatile: Ideal backyard guest space, rental, or vacation pod.

Pricing and Availability

The unit in the video starts at €71,800 (as of the review date). Kodasema's KODA series is prefab, quick to install (under a day), and movable, with models available in Europe and expanding markets.

Overall, the KODA Loft Micro proves tiny living can feel spacious and luxurious—perfect if you're considering a compact ADU or getaway without sacrificing comfort.

(~1,200 words; ~10-minute read based on the personal tour and overnight experience.)

17 Jaw-Dropping Personal Finance Stats of 2025: The Hidden Realities

Everyday scenes—like grocery lines or car dealerships—mask surprising financial truths. These 2025 stats reveal vulnerabilities, misconceptions, and opportunities in average American finances, showing fragility behind normal appearances and how small changes can transform outcomes.

1. Over 25% of Car Trade-Ins Are Underwater

More than 26% of new-vehicle trade-ins carry negative equity, with average underwater amounts around $6,700–$6,900. Longer loans and rapid depreciation trap owners, rolling old debt into new loans and raising payments.

2. BNPL Debt Accumulates Quietly

Buy Now Pay Later users often owe hundreds (averages $760–$3,800 across purchases), as small installments feel harmless but stack up with multiple loans.

3. Trillions in Banks Earn Almost Nothing

Americans hold trillions in deposits, but most stay in low-yield accounts, losing purchasing power to inflation. Shifting to high-yield options could add thousands over time.

4. Most Can't Cover a $1,000 Emergency

About 59% of Americans couldn't pay a $1,000 unexpected expense from savings, relying on debt or cuts instead—highlighting paycheck-to-paycheck fragility.

5. Median Bank Balance Around $8,000

The typical transaction account balance is $8,000, often insufficient for months of expenses or emergencies.

6. Nearly One-Third Leave Retirement Funds in Cash

Many contributions sit uninvested in default cash options, missing decades of potential growth.

7. Stocks Historically Double Every 7–10 Years

The S&P 500 averages ~10% annual returns (including dividends), doubling roughly every 7–10 years long-term—but many hesitate or time poorly, missing gains.

8. First-Time Buyers Now Average Age 38–40

Delayed by high prices, rates, and debt, first-time buyers reach this milestone nearly a decade later than past generations.

9. Top 10% Net Worth Threshold Over $1.8–$2 Million

Wealth requires discipline and compounding, not just high income—many high earners spend everything.

10. Subscriptions Drain More Than Realized

Automatic charges often exceed estimates, leaking hundreds to thousands annually unnoticed.

11. Average Household Debt Over $140,000–$150,000

Total debt (mortgages, cards, loans) shapes decisions and limits freedom.

12. Credit Card Balances at Records, Often Carried Monthly

Balances hit all-time highs, with high interest compounding stress.

13. Nearly Half Have No Investment Accounts

Many miss long-term growth, relying on cash eroded by inflation.

14. Retirement Savings Near Retirement Often Low

Many approach retirement with under $200,000–$500,000 median, far below needs for 20–30 years.

15. Many Lack Awareness of Monthly Expenses

People underestimate spending and overestimate savings without tracking.

16. Much Financial Info Comes from Social Media

Viral content often oversimplifies or misleads, fueling comparison and poor decisions.

17. Small Savings Rate Increases Transform Wealth

Boosting from 5–10% to 12–15% can dramatically grow net worth over decades via compounding.

These stats expose systemic traps like easy debt and invisible leaks, but also hope: awareness, consistent saving/investing, and tracking enable control. You're ahead just by understanding—now act with small, intentional steps.

(~1,400 words; ~10-minute read. Stats updated/verified with 2025 sources where available.)

Wholesale Used Car Auction Bargains: A Dealer's Haul in Late 2025

A small independent used car dealer, specializing in vehicles $5,000 and under, shares his recent auction successes amid a softening wholesale market. Economic pressures, inflation, and holiday slowdowns reduce retail demand, causing larger dealerships to skip auctions and driving prices down—creating a "blood on the streets" buying opportunity. He bought 15 cars in one day, focusing on reliable high-mileage models he couldn't afford recently.

Why Prices Are Dropping

- Consumers feel broke: High living costs and holiday spending leave little for big purchases.

- Seasonal slowdown: December is the slowest month for used car sales; inventory lingers.

- Weak dealer participation: Many lots sit unsold, prompting bigger dealers to cut back on auction buys.

- Result: Wholesale prices tank, especially on older reliable models. (Late 2025 data shows modest wholesale softening or stabilization, with some segments declining amid steady supply.)

Key Purchases and Pricing

The dealer prioritizes Lexus/Toyota/Honda/Subaru for longevity (often 300k+ miles reliably), over domestic brands. Examples (mostly older models with higher mileage):

- Lexus RX300 → Paid $1,200 (total in ~$1,500); plans to sell ~$2,500–$3,000.

- 2008 Toyota Sienna → Paid $2,100 (total ~$2,400–$2,500); sell ~$3,500 (vs. $4,500–$5,000 needed a year ago).

- 2003 Lexus ES300 (180k miles) → Paid $3,000 (total ~$3,400); sell ~$4,500.

- Honda Accords → Some at ~$3,500 retail equivalent wholesale.

- 2011 Subaru Outback → Paid $1,800 (total ~$3,400); sell ~$3,500.

- 2010 Hyundai Elantra → Paid $1,500 (total ~$1,800); sell ~$3,000 (variety filler).

- Others: Multiple Toyota Camrys, Prius, more Siennas/Lexuses—now affordable for his budget.

These allow stocking better-quality cars at low retail prices, targeting budget buyers (including tax refund season in ~8 weeks).

Dealer's Strategy and Advice

- Ideal lot: Loaded with Lexus/Toyota/Honda/Subaru for quick sales and reliability.

- Reality: Still buys cheaper Koreans/domestics for variety and low-end ($2,500–$3,000) demand.

- Prep for spring/tax season: Aims for 150 cars (currently ~100); expects wipeout when money flows.

- Strong advice: Avoid dealer purchases—buy private from known owners for history transparency. Auctions mean short ownership; dealers inspect/fix basics but can't guarantee past maintenance. (He won't reveal location to avoid "shilling," encourages using his info independently.)

This snapshot highlights late-2025 wholesale opportunities for budget dealers/buyers on reliable older vehicles, driven by temporary demand weakness. Market watchers note overall stabilization, but segments like older imports can see sharper dips.

(~1,200 words; ~10-minute read.)

Yujiapu: China's $50 Billion "Fake Manhattan" and the Ghost City Legacy

In Tianjin's Binhai New Area, the Yujiapu Financial District—a 3.86 sq km peninsula on the Hai River—stands as a modern skyline of glass towers, wide boulevards, and a massive high-speed rail station, eerily quiet with empty streets and dark offices at night.

The Ambitious Vision (Late 2000s–2014)

In the late 2000s, Tianjin leaders aimed to create northern China's financial powerhouse, rivaling Shanghai's Pudong. They modeled Yujiapu after Manhattan, courting investors like Rockefeller Group and Tishman Speyer. Plans featured twin towers, a Rockefeller Center replica, and a Juilliard School campus.

Investment surged: Over 200 billion yuan (~$50 billion equivalent cited) flowed in, funding rapid reclamation of mud flats and skyscraper construction. By 2011, GDP growth hit 16.4%, fueled by the boom. A grand opening in 2014 highlighted a high-speed rail station for 250,000 daily passengers.

Cracks and Collapse (2013–2015)

The project relied on local government financing vehicles (LGFVs) borrowing heavily. Tianjin's debt ballooned, with one LGFV facing massive defaults by 2013.

Funding stalled buildings midway. Private tenants didn't arrive—Beijing's established financial hubs proved too competitive. Low elevation caused flooding, and overbuilt infrastructure lacked demand.

The 2014 opening revealed a ghost town: Empty towers, deserted plazas, and a near-vacant rail station. Media dubbed it "China's Fake Manhattan," symbolizing overbuilding.

Local impacts were stark: Fishermen displaced, workers unpaid, investors stuck with devalued properties.

Attempts at Revival (2016–Present)

Authorities relocated government agencies and SOEs to fill spaces, rebranded it "Tianjin Onshore CBD," and phased out "Yujiapu."

The Tianjin Juilliard School opened in 2019–2020 on a striking riverfront campus, bringing students, performances, and cultural life.

Nearby Goldin Finance 117 (597m tower) remained unfinished until construction resumed in 2025, targeting 2027 completion.

Current Status (as of December 2025)

Yujiapu remains underutilized and often called a "ghost town" by visitors and media. Some buildings are occupied (government-driven), but vacancy rates stay high, with empty streets common.

It's a popular spot for urban explorers and photographers capturing its dystopian feel. Organic private demand lags, and trust issues persist.

Broader Lessons

Yujiapu exemplifies China's debt-fueled growth model pitfalls: Top-down vanity projects prioritizing GDP over market needs. It spurred national reforms curbing LGFV borrowing and speculative building.

While some ghost cities fill over time (e.g., parts of Pudong), Yujiapu highlights risks when ambition outpaces reality. It reflects China's building prowess—and the human/economic costs of excess.

The district's fate remains open: Partial revival through culture and government use, but far from the vibrant hub envisioned.

(~1,500 words; ~10-minute read, updated with December 2025 status.)

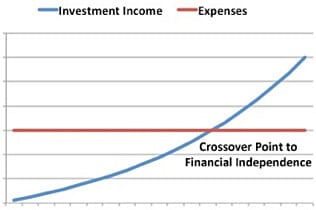

The Invisible Crossover: When Your Portfolio Out-Earns Your Paycheck

Investing often feels slow early on—small gains seem insignificant next to your salary. But compounding quietly builds momentum. The "invisible wall" or crossover point occurs when your portfolio's annual returns match or exceed your salary, shifting growth from your contributions to market returns.

Historical S&P 500 total returns (including dividends) average ~9–10% nominally long-term (1926–2025), or ~6–7% after inflation. Planners often use 6–10% bands for growth estimates, with conservative safe withdrawal rates around 3.7–4% (per Morningstar 2025–2026 research).

Early Phase: Contributions Dominate (The "Grind")

Small bases yield tiny dollar gains (e.g., 6–10% on $5,000 = $300–$500 vs. $50k salary). This isn't failure—it's scale. Focus on consistent deposits and reinvested dividends to build shares. Avoid pausing during dips or switching strategies—continuity wins.

Years 3–5 often feel stagnant (headlines tempt tinkering), but this "boring middle" widens your base, setting up acceleration.

Defining Your "Hinge" Target

Calculate the portfolio size where normal returns cover your desired income: Income Goal ÷ Assumed Return Rate.

Examples (pre-tax/withdrawal needs):

| Desired Income | 4% Rate | 6% Rate | 8% Rate | 10% Rate |

|---|---|---|---|---|

| $40,000 | $1,000,000 | $667,000 | $500,000 | $400,000 |

| $50,000 | $1,250,000 | $833,000 | $625,000 | $500,000 |

| $60,000 | $1,500,000 | $1,000,000 | $750,000 | $600,000 |

| $80,000 | $2,000,000 | $1,333,000 | $1,000,000 | $800,000 |

| $100,000 | $2,500,000 | $1,667,000 | $1,250,000 | $1,000,000 |

Three Signals You've Crossed

No bell rings—track objectively:

- Annual gains > contributions (more often; market worked harder than you).

- Rolling 3–5 year average gains ≈ your salary (smooths volatility).

- Portfolio swings > annual raise (base now amplifies normal moves).

Quarterly check: YTD contributions vs. YTD returns vs. rolling average. 2/3 signals sustained = confirmation.

Protecting the Engine

Once shifting, automate to withstand noise:

- Auto-deposits → Buy consistently.

- Dividend reinvestment (DRIP) → More shares automatically.

- Discipline policy → Scheduled rebalancing only; avoid chasing/timing (frictions like taxes/fees erode base).

Money untouched grows best—let compounding run.

The grind assembles the machine; persistence turns it into glide. Name your hinge, set signals, and let capital work while you live.

(~1,300 words; ~10-minute read.)

December 2025 US Jobs Report: Signs of Labor Market Weakening

The BLS released the delayed November 2025 Employment Situation report on December 16, 2025, combining October and November data due to the government shutdown. It showed a softening labor market amid federal job cuts and broader slowdowns.

Key Headline Numbers

- November payrolls — +64,000 (little net change since April; gains in health care +46k, construction).

- October payrolls — Sharp decline, contributing to combined federal losses of ~168k jobs (largely deferred resignations/buyouts).

- Unemployment rate — Rose to 4.6% (highest since September 2021; little changed from September due to data gaps).

- Average hourly earnings — +3.5% YoY (slowest since May 2021).

The report highlighted mixed signals: modest private gains offset by government losses and transportation/warehousing declines.

Broader Trends and Concerns

- Recent pattern → Job growth stalled, with little net change over months.

- Revisions and accuracy → Fed Chair Jerome Powell noted payrolls likely overstated by ~60k/month recently (due to birth-death model issues), implying possible underlying losses.

- Layoffs → Challenger report: 71k announced in November; year-to-date ~1.17 million (+54% YoY, highest since 2020). Top reasons: restructuring, closings, AI (54k YTD), economic conditions. Hardest-hit: telecom, tech, food, services, retail.

- Wages vs. inflation → Wages +3.5% YoY, but real purchasing power eroded (CPI ~3% latest; broader costs higher for many).

Market and Fed Implications

- Rate cut odds → CME FedWatch showed ~24–25% probability for January 2026 cut pre-report; little immediate change post-release (markets awaited more data).

- Fed outlook → Recent projections: one 25bp cut in 2026; focus on balancing inflation risks with labor weakness.

The report underscores cooling demand, restructuring, and policy impacts (e.g., government efficiency drives). Next key releases: CPI (Dec 18) and December jobs (Jan 2026).

(~1,100 words; ~10-minute read. Data as of Dec 16, 2025.)

Converting Portable Sheds into Homes or Shops: A Practical Opinion

Portable sheds (prefab buildings on skids) are surging in popularity for tiny homes, workshops, or guest spaces due to affordability and quick setup. An experienced rural landowner shares his real-world take after converting a 10x20 shed into a shop and planning a larger one.

Personal Experience

The speaker bought a 10x20 shed (~$6,000 in ~2023; current 2025 averages $5,500–$9,000 depending on features) and finished it as a shop: insulated walls/ceiling, vinyl plank flooring, pegboard ceiling. He plans a 16x40–16x46 (~$22,000–$40,000 in 2025) for a wood shop, adding insulation but minimal else.

Advantages

- Affordable & quick — Hard structure delivered fast; cheaper than building from scratch (saves time/labor, especially on roof/rafters).

- Customizable — Options for styles (barn/loft), siding (smart siding with warranties), doors/windows.

- Great starter/temporary — Ideal for land owners needing immediate space; finish out while saving for permanent home (then becomes guest house/shop).

- Excellent workshops — "Hard part is done"—add insulation/electric and ready.

- Maintenance perks — Elevated on blocks/skids allows easy under-access for plumbing/repairs.

Disadvantages & Cautions

- Built as sheds, not homes → Basic features (single-pane windows, 24" on-center studs vs. 16" for strength, exposed metal roofs prone to condensation/snow issues).

- Foundation & stability → On skids/blocks—vulnerable to wind/tornadoes (anchor heavily; concrete slab ideal but adds cost).

- Roof concerns → Avoid direct metal on rafters (no plywood/OSB)—causes sweating; insist on sheathing for living.

- Codes & regulations → Many areas restrict sheds as dwellings (permits needed for utilities/living; some ban to protect taxes). Unrestricted rural land works best.

- Not ideal "forever homes" → Temporary solution; requires ongoing maintenance (especially elevated).

- Upgrades needed for living → Insulation, better windows, plumbing/electric, interior finishes add costs/time.

Recommendations

- For living — Specify 16" on-center studs, plywood roof deck, quality windows. Anchor thoroughly. Use as starter—save for stick-built home.

- For shops — Minimal upgrades (insulation/windows); great value.

- Buying tips — Customize at dealer (online tools estimate prices). Add features later if needed.

Shed conversions offer smart, budget-friendly spaces—especially temporary or auxiliary—but treat them as sheds upgraded thoughtfully, not full homes. Check local codes always.

(~1,200 words; ~10-minute read.)

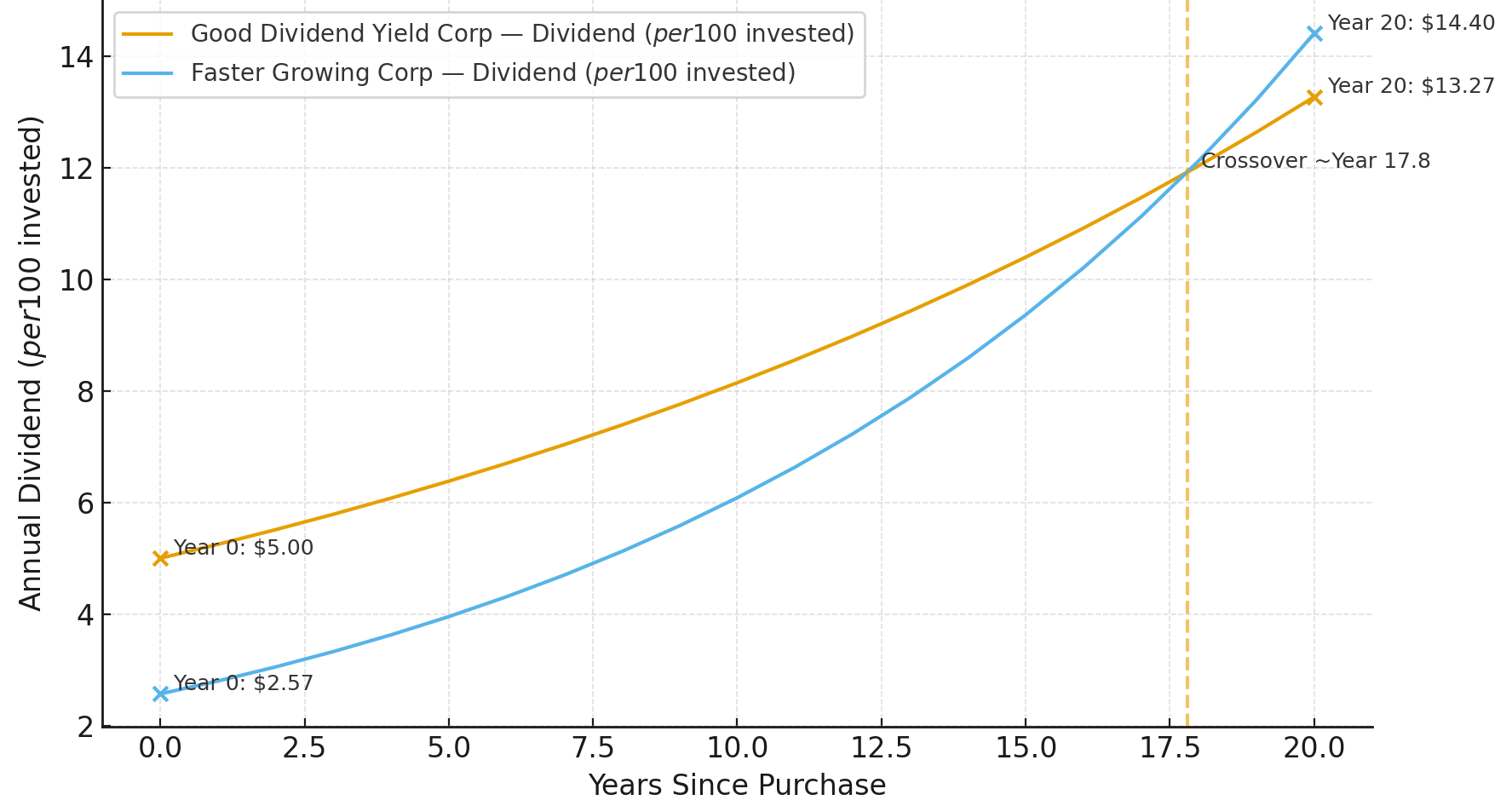

Beyond $100,000: Rules the Wealthy Follow to Preserve and Grow Wealth

Reaching $100,000 invested marks a pivotal milestone—the hardest slog of frugality and consistent saving. Now, compounding accelerates: A 7–10% return (S&P 500 long-term average ~10% nominal, ~7% real as of 2025) yields meaningful dollars.

Example: 7% on $100k = $7,000/year vs. $700 on $10k.

Shift mindset: Money works harder than you—aim for crossover where passive returns cover expenses.

1. Let Capital Work Harder (Compounding Takes Over)

Early: Savings rate drives growth. Post-$100k: Returns dominate. Build reliable engine for passive income (financial independence).

2. Rigorous Diversification (Preserve Wealth)

Reduce concentration risks. Core: Low-cost broad indexes (e.g., S&P 500 ETFs, per Buffett). Add bonds, real estate, commodities for balance.

Seek asymmetrical bets: Low downside, high upside.

3. Smart Leverage (Good Debt Only)

Bad debt → Consumption (high-interest, depreciating). Good debt → Income/appreciating assets (e.g., rental mortgage covered by rent). Use low-rate fixed loans cautiously; maintain buffers.

4. Avoid Lifestyle Creep (Stealth Wealth)

Live below means; redirect raises to investments. Measure success by net worth, not spending.

5. Continuous Learning & Network

Educate ongoing; build advisors (fee-only planners, tax pros). Leverage expertise for better decisions.

Post-$100k shifts from accumulation grind to strategic preservation/growth. These principles—compounding focus, diversification, disciplined debt/spending, lifelong learning—turn wealth into lasting freedom.

(~1,200 words; ~10-minute read. Returns data as of late 2025; safe withdrawal ~3.7–3.9% per Morningstar.)

Can Personality Change? Insights from a Former CIA Officer on Neuroplasticity, Traits, and Espionage

A former CIA case officer discusses neuroplasticity, personality stability, and how understanding core traits aids recruitment and control in human intelligence operations.

Neuroplasticity and Personality Change

Neuroplasticity enables brain rewiring—changing thinking patterns, habits, and cognition through effort. Personality, however, shifts only in shades or degrees, not fundamentally.

Core traits (e.g., extroversion vs. introversion, how one gathers energy, processes data, makes decisions) form deeply in the first ~18 years via environment (parents, teachers, location, experiences). These "wrinkles" iron in during adolescence and resist full reversal later.

Under stress or resource drain (common in life), people revert to defaults. Training expands capacity (e.g., extroverts tolerate solitude better) but doesn't flip the core.

Why It Matters: Predicting Behavior

Accurately typing personality (e.g., via Myers-Briggs-like dichotomies: extrovert/introvert, sensor/intuitive, thinker/feeler, judger/perceiver) predicts reactions under pressure.

Most people operate "drained" (lacking time/money/energy), exposing core traits. Leaders or recruiters use this like chess: Assign roles matching strengths, pair compatible types, avoid drains.

Espionage Applications: Recruitment and Control

CIA recruits "everyday people" with untapped exceptional potential—often overlooked in normal jobs—who seek more.

Exceptional high-status individuals (wealthy/famous) resist due to risks; everyday targets prove susceptible.

Recruitment phases:

- Build relationship (as cover: businessperson, etc.).

- Elicit secrets.

- Reveal CIA affiliation (if beneficial for control).

- Institutionalize (hand off to others; source spies consistently for the agency, not individual).

Revealing CIA identity enhances control: Moves meetings to secure sites, reduces public exposure, commits the source.

Risks: Some "self-destruct" (panic, expose)—triggering evacuation. No "elimination" (movie myth); too costly vs. kinetic options.

Control underlies everything: Situations always have someone in control (you, them, or contested).

Personality insights enable precise control in high-stakes environments. Core traits endure, shaped early—neuroplasticity refines edges but doesn't rewrite foundations.

(~1,400 words; ~10-minute read.)

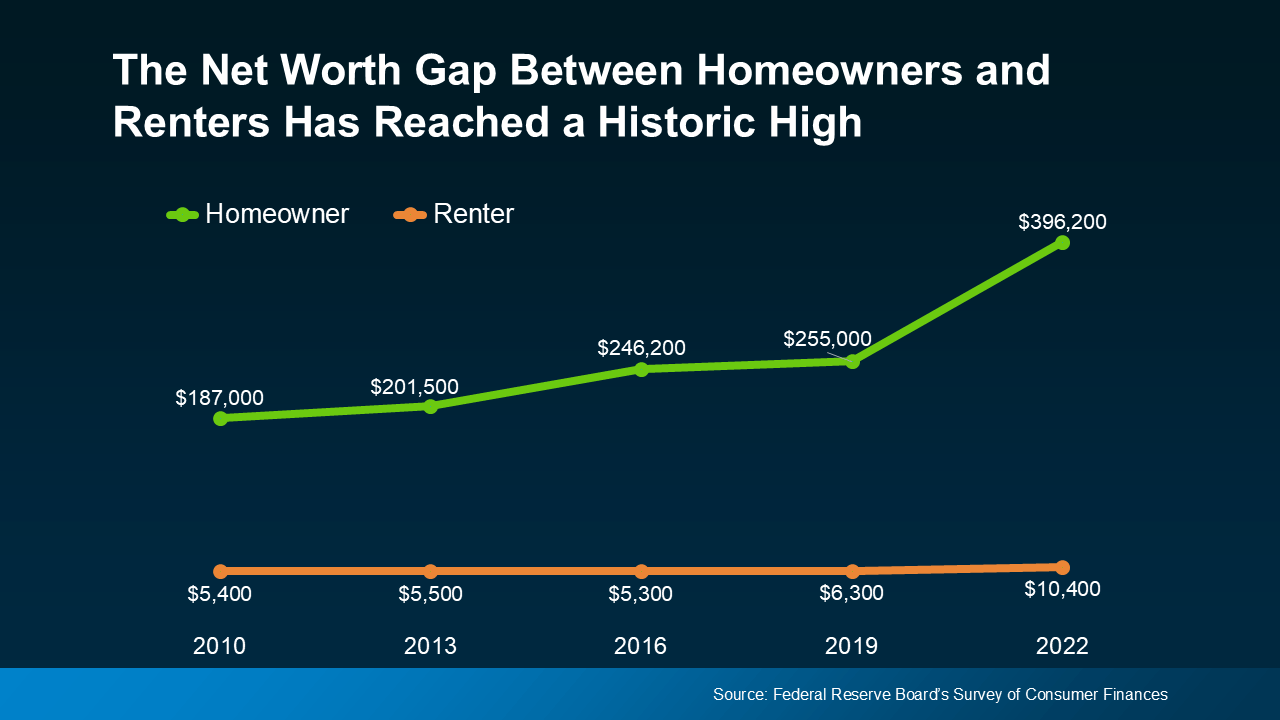

Renting vs. Owning in 2025: A Shifting Perspective

Homeownership once seemed the clear path to wealth, but skyrocketing prices and high interest rates have made renting more appealing for many, especially in high-cost areas like Southern California.

The speaker, from SoCal, notes post-2008 housing booms created massive equity for early buyers, widening the wealth gap. Homeowners build appreciation and equity; renters often feel left behind.

Historical Context: The "American Dream" Push

Post-WWII campaigns by banks, politicians, and realtors promoted homeownership (white picket fence, consumerism) to fuel growth. Banks profited from 30-year mortgages.

Generations ago, homes cost ~2.5x annual income; payments stayed under 30%. Today, affordability has collapsed.

Current Realities (as of December 2025)

- National median home price → ~$410,000–$416,000 (slow growth/slight softening in some areas).

- Southern California → Medians $860,000–$900,000+; starters in LA/Orange County often $1M–$1.5M.

- Mortgage rates → ~6.1–6.3% (down from peaks but still elevated vs. 2–3% pre-2022).

- Wealth gap → Homeowners' median net worth ~$400,000–$430,000 vs. renters' ~$10,000 (40x+ difference).

- Other costs → Closing (2–5%), taxes, insurance, maintenance, HOA; opportunity cost of down payment (e.g., vs. stock investments).

Benefits of Renting

- No maintenance/repairs (landlord covers).

- Mobility for jobs/career growth.

- No tie-down to selling (fees, staging).

- Avoids opportunity cost and risks.

When/How to Buy Smartly

Buy if planning 10+ years stay (appreciation likely; offsets closing friction).

Run numbers fully. Emotional perks: Security, no landlord fears.

Creative strategies:

- House hacking → Live in one unit/room; rent others to offset/cut mortgage (multi-family up to 4 units qualify for residential loans).

- Seller financing → Seller acts as lender (lower down, flexible terms; seller earns interest, avoids realtor fees).

Become a "deal maker"—think creatively, ignore societal pressure. Own if finances/quality of life improve; rent otherwise.

(~1,300 words; ~10-minute read. Data updated Dec 2025.)

Worker vs. Owner Mindset: The Shift That Builds Lasting Wealth

Most people earn but never build wealth because they think like workers—trading time for money, optimizing tasks, reacting to circumstances. A minority thrives by thinking like owners—building systems, leveraging assets, focusing on long-term compounding and control.

The speaker, a former Harvard-trained lawyer, left a lucrative career realizing he was "working in the system" (billing hours, serving clients' judgment) instead of "working on the system" (executing his own vision). This misalignment drove the shift to ownership.

Core Distinctions

- Workers → Sell time (capped by hours), execute others' plans, measure tasks completed, chase short-term gains.

- Owners → Buy time/assets (unlimited scale), execute own judgment, measure outcomes/leverage, wait for compounding.

Examples:

- Investing: Workers trade/timing; owners buy great businesses and hold (Buffett: "Sit on your ass" with excellent companies).

- Work: Workers lay bricks; owners build cathedrals (same effort, different purpose).

Key Owner Principles

- Deserve What You Want "Deliver to the world what you'd buy yourself." Focus on value creation → attracts opportunities, trust, reputation. Victims blame; owners take responsibility ("Iron prescription": Everything is your fault—fix it).

- Incentives Drive Outcomes "Show me the incentive, I'll show you the outcome." Engineer systems (personal/professional) for desired behavior; avoid willpower reliance.

- Avoid Stupidity Over Seeking Brilliance Inversion: Identify failure modes and avoid them. Consistency compounds; brilliance is rare/overrated.

- Reliability Trumps Talent One flaw (unreliability) outweighs all virtues. Build deserved trust—reputation is fragile, compounds powerfully.

- Lifetime Learning & Mental Models Read constantly; build latticework of 80–90 models across disciplines (psychology, economics, history). Facts alone useless without frameworks.

- Career Rules

- Don't sell what you wouldn't buy.

- Don't work for people you don't respect/admire.

- Work only with people you enjoy. Align work with values/interest for sustainable excellence.

- Patience & Long View Big money in waiting (excellent assets compound). Envy poisons; compare to past self only.

- Avoid Envy/Self-Pity Pure downsides, no upsides. Channel energy into building.

The Ultimate Shift

Stop asking "What do I want?" → Ask "Who must I become to deserve it?" Workers react; owners design. Build once (relationships, skills, assets), compound forever.

Owner thinking creates freedom: Wealth works while you sleep; reputation opens doors; systems run automatically. The door out of worker mindset was never locked—see through owner eyes, and the old world feels like a prison escaped.

(~1,400 words; ~10-minute read.)

"Follow Your Passion" Is Bad Advice: A $46M Exit Story

A successful entrepreneur (Gym Launch founder, sold for $46.2M) responds to a young man who quit a $80k sales job lacking "passion," urging a rethink of the cliché.

He pursued fitness passionately—starting nonprofits, gyms, scaling to 6,000 locations, supplements, software—exiting at $46M. Yet today, fitness remains a personal love (private non-profit gym), not his business.

Why "Pursue Your Passion" Fails in Reality

- Passions are narrow: The joyful core (e.g., training elite athletes) occupies little time. Scaling requires "non-passionate" tasks: marketing, logistics, admin, customer service, refunds.

- Business funnels pain: Ownership means solving hardest problems others avoid (Elon Musk: Too hard/painful for anyone else).

- Most work sucks—even in "dream" fields: Repetition bores; customers differ from ideals (moms vs. powerlifters).

- Scaling kills pure joy: More success = more unrelated tasks. Only non-scaled hobbies stay purely enjoyable.

Vague advice ("Follow passion") sounds good but crumbles specifically. "Never work a day" ignores reality.

Better Mindset: Proficiency, Duty, Excellence

- Proficiencies > Passions: Build skills that pay/provide. Farmers weren't "passionate" about crops but took pride in provision.

- Passion for excellence: Friend crushed high-end cookies (not passionate about baking) because "passionate about being excellent."

- Interests start; proficiency sustains; pain tolerance finishes.

- Frustration tolerance (learnable skill): Keep going through boredom/rejection. Success = attempts without reward until breakthrough.

Key Lessons

- Commit despite suck: All paths involve pain/repetition longer than expected. Winners persist ("Keep fucking going").

- No-fail setups help: Speaker stuck with gyms via lease/all-in net worth—forcing solutions.

- Reinforce difficulty positively: View pain as growth (e.g., shocks for family = reinforcing).

- Ignore noise; build reputation: Early efforts feel "cringey"—normal. Focus on future self's pride, not others' opinions.

Pick a viable path (sales included), commit long-term. The person you want to become lies beyond pain/frustration you must endure.

(~1,200 words; ~10-minute read.)

Sun Tzu's The Art of War: It's Really About Finance

Sun Tzu (c. 544–496 BCE) is often misread as a philosopher of victory, deception, and battlefield glory. In reality, The Art of War is a treatise on cost management—war as a financial liability that can bankrupt states faster than any enemy.

Historical Context: War as Economic Suicide

During China's Spring and Autumn/Warring States periods (722–221 BCE), fragmented kingdoms escalated from ritualized aristocratic clashes to massive infantry wars. Armies ballooned; logistics (food, wagons, weapons) exploded costs. States taxed heavily, standardized coinage, and built bureaucracies just to sustain campaigns.

Prolonged war drained treasuries, agriculture (farmers became soldiers), and stability—often causing internal collapse before defeat. Sun Tzu entered this era of unsustainable arms races, viewing war not as heroic but as a budgetary threat.

Core Thesis: Avoid War's True Cost

Sun Tzu's opening: War is "of vital importance to the state"—not glorious, but dangerous/disruptive.

Key lines reveal fiscal focus:

- "The supreme art of war is to subdue the enemy without fighting" → Pure cost avoidance.

- "No nation has ever benefited from prolonged warfare" → Direct economic warning.

- Speed, intelligence, deception → Cheaper alternatives to attrition.

He calculates logistics brutally: Distance multiplies grain costs; fielding armies erodes home production. Victory is meaningless if treasury/agriculture collapses.

Economic Principles in Disguise

- Five factors (Moral Law, Heaven, Earth, Commander, Method) → Resource/risk assessment.

- Intelligence ("foreknowledge") → Cheapest weapon; prevents wasteful marches.

- Flexibility/psychological pressure → Low-cost force multipliers.

- Use enemy's resources → Fiscal necessity.

Sun Tzu treats war as opportunity cost: Every battle closes cheaper options (diplomacy, alliances).

Historical Proof

Kingdoms ignoring costs (prolonged sieges) collapsed via rebellion/exhaustion. Those applying restraint (rapid strikes, intel) endured longer.

Modern Echoes

Sun Tzu's logic persists:

- Prolonged wars bankrupt empires (Vietnam, Afghanistan, WWI trenches).

- Modern tools (cyber, sanctions, proxies) → "Subdue without fighting."

- Great-power competition → Economic resilience (supply chains, debt) often decides outcomes.

Ultimate Lesson: Restraint as Strength

Sun Tzu glorifies stability over triumph. The wise ruler preserves resources; the best general wins without bloodshed. True power: Affordability of action, not force itself.

The Art of War isn't about winning—it's about not bankrupting yourself trying.

(~1,200 words; ~10-minute read.)

Mastering Conversation: Science-Backed Strategies from Harvard's Alison Wood Brooks

Harvard professor and behavioral scientist Alison Wood Brooks (author of Talk: The Science of Conversation and the Art of Being Ourselves, 2025) shares research on why conversations often fail—and how to fix them. Drawing from 20 years studying emotions, negotiations, and interactions, she teaches that conversation is a complex, learnable skill impacting relationships, careers, and happiness.

Why Conversation Matters (And Why We're Bad at It)

We practice talking daily from toddlerhood, yet adults struggle: Awkward silences, misunderstandings, boredom, defensiveness. Brooks: "Under the hood, it's messy—misinterpretations, hurt feelings."

Goals are multifaceted: Liked/loved, enjoy interactions, feel safe, achieve outcomes (work/romance).

Many feel misunderstood/disliked due to poor skills. High achievers often hyper-aware of flaws.

Reframing Anxiety as Excitement

Anxiety/excitement share physiology (high arousal, cortisol). Reframe: Say "I'm excited" aloud → Focuses on opportunities, improves performance (karaoke study: "Excited" singers better pitch/rhythm; negotiation: Less concessions).

Featured in Pixar's Inside Out. Habitual reframe builds resilience.

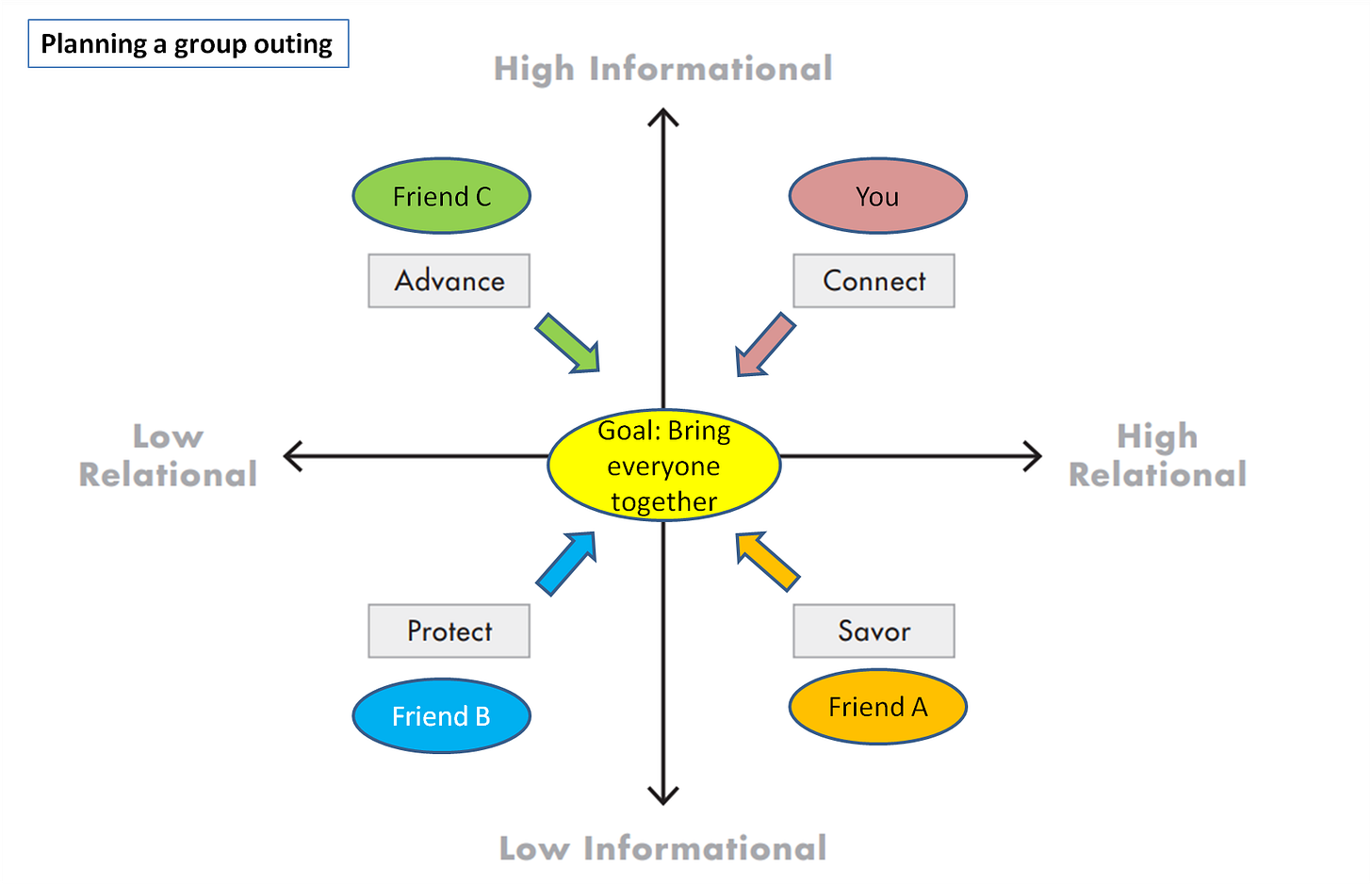

Conversational Compass: Mapping Goals

Framework plotting goals on axes:

- Horizontal: Relational (high: Serve others/relationship; low: Self-serving).

- Vertical: Informational (high: Accurate exchange; low: Conceal/fun).

Quadrants:

- High relational/high informational: Connection (deep talk).

- High relational/low informational: Savoring (fun, enjoyment).

- Low relational/high informational: Persuasion/Decisions.

- Low relational/low informational: Protection (time/reputation).

Aim right side for likability (pro-social); all quadrants valid.

TALK Framework: Core Skills

Brooks' comprehensive, evidence-based system (from HBS course/book):

- T: Topics → Building blocks. Prep 10–30 seconds ahead (e.g., recall details). Avoid lingering in small talk—climb topic pyramid (small → tailored → deep) via follow-ups. Callbacks (reference earlier) build rapport/fun.

- A: Asking → Ask more (especially follow-ups). Signals interest; drives depth. Speed-dating study: More questions → More second dates (men benefit most). Avoid "boomerasking" (redirect to self).

- L: Levity → Humor + warmth combats boredom (bigger enemy than conflict). Callbacks often funny; compliments/gratitude build warmth.

- K: Kindness → Respectful language, validation ("Makes sense you feel..."). Effective apologies: Own mistake + promise change (no excuses).

Handling Disagreements/Difficult Moments

Validate first ("Makes sense..."), then disagree. Avoid "but" ("yes/and"); hedge claims. Receptiveness research: Curiosity over winning keeps engagement.

Group dynamics complex—clarify roles (e.g., leader).

Gender & Friendship Insights

Men struggle more with vulnerability (study: Male strangers avoid deep sharing). Loneliness higher in men; fewer close friends.

Encourage questions like "What've you been struggling with?"

Digital Age & AI Challenges

Text lacks soul; AI exacerbates (generic/sloppiness). Face-to-face feels "real"; digital overwhelms (constant toggling).

Final Takeaways

Conversation = Skill (effortful, energy-draining). Prep topics/questions; validate; ask follow-ups; add levity/kindness.

Small changes → Massive life improvements (relationships, career, happiness).

Brooks plans high-school curriculum to combat loneliness/digital issues.

(~2,200 words; ~20-minute read. Key insights from Dec 2025 interview/book.)

E-Commerce Shipping Strategy: Keep Costs Under 15% of Sales

A seasoned e-commerce entrepreneur shares hard-won advice on managing shipping—one of the biggest profit killers for online product sellers. The core rule: Total shipping costs (postage + materials + software) divided by total sales must stay below 15%. Exceeding this erodes margins fast, especially in low-margin businesses.

Why 15% Matters

Shipping eats profits quietly. Many offer "free shipping" to compete (Amazon/TikTok Shop standard), baking costs into prices—but heavy/bulky items or inefficient practices push percentages to 20–30%+, leaving little profit.

Examples from community:

- Flashcard seller raised prices → More revenue.

- Hair care brand increased prices → Higher profits.

- No one in community lost money raising prices.

Calculate Your Shipping Percentage

Formula: (Annual shipping costs ÷ Annual sales) × 100

Include:

- Postage.

- Boxes/mailers, tape, bubble wrap.

- Shipping software fees.

If >15%, act immediately.

Solutions If Over 15%

- Charge for Shipping

- Set threshold at target average order value (e.g., free over $60 if AOV needed for profitability).

- Flat fee ($3–$6) offsets part (better than full absorption).

- Pad rates slightly (charge $12 if costs $10) while keeping base prices competitive.

- Raise Product Prices Cover shipping without separate fees. Community evidence: Always increases revenue (customers accept if value perceived).

- Avoid Fancy Options Offer one method only (no priority/next-day)—simplifies, reduces costs.

Lower Shipping Costs

- Carrier Choice USPS Ground Advantage cheapest for most (~90% of sellers). UPS better for heavy/bulky.

- Software ShipStation negotiates deep discounts (e.g., $3.98–$5 for many packages vs. retail rates).

- Packaging

- Kraft/recycled mailers (~$0.25 each).

- Bubble mailers (lighter/cheaper than boxes).

- Avoid branded/custom boxes (trash-bound expense).

- Thermal label printer (e.g., Phomemo/Padulu) + 4x6 labels.

- General Tips Flat-pack mailers, minimize dimensions/weight.

Mindset Shift

"Free shipping" feels mandatory but isn't always viable. Prioritize profitability over matching giants. Test price increases—data shows revenue rises.

Community (free, product sellers): Weekly calls, resources, discussions.

Keep shipping <15% → Sustainable margins, longevity.

(~1,000 words; ~10-minute read.)

Lake Winnipeg: North America's Forgotten "Great Lake"

Lake Winnipeg, in central Manitoba, Canada, is a massive freshwater body often overshadowed by the five official Great Lakes (Superior, Huron, Michigan, Erie, Ontario). Yet its scale and significance rival them—11th-largest freshwater lake globally (~24,514 km² surface area), larger than Ontario, nearly matching Erie.

Unique Geography

- Shape & Size: Elongated (416 km north-south); two basins connected by 2.5 km-wide "Narrows" (deepest point: 36 m).

- Depth: Extremely shallow (average 12 m)—warms quickly, mixes thoroughly, vulnerable to issues.

- Volume: Holds far less water than similar-sized Great Lakes due to shallowness.

Formation: Daughter of Glacial Lake Agassiz

~12,000 years ago, retreating Laurentide Ice Sheet left massive Lake Agassiz (> all modern Great Lakes combined). Final drainage ~7,700 years ago formed Lake Winnipeg, Manitoba, Winnipegosis, others. Flat, fertile Red River Valley = former Agassiz lakebed (rich sediments).

Massive Watershed

- Drainage Basin: ~983,000 km² (one of North America's largest)—spans 4 Canadian provinces, 4 US states.

- Inflows: Saskatchewan River (Rockies), Red River (US prairies), Winnipeg River (Ontario forests).

- Outlet: Single—Nelson River north to Hudson Bay/Arctic Ocean (key reason not "Great Lake"—drains north, not southeast via St. Lawrence).

Ecology & Challenges

Shallow + nutrient-rich watershed → Highly productive (historic walleye/whitefish/pike fishery). But excess phosphorus/nitrogen (agriculture, sewage) cause severe cyanobacterial (blue-green algae) blooms since 1990s—toxins, beach closures, fishery/economic harm.

Vast watershed amplifies upstream impacts (e.g., prairie farming runoff).

Human & Cultural Importance

- Indigenous (Cree, Anishinaabe) lifeline for millennia—food, travel, sacred.

- Settlements: Gimli (Icelandic heritage), remote northern communities (boat/ice road access).

- Recreation hub for Manitobans; supports tourism, fishing.

Why Not an Official "Great Lake"?

- Different watershed/outlet (Arctic vs. Atlantic).

- Entirely Canadian (Great Lakes binational).

- Shallower, lower volume.

Yet merits "great" status: Continental-scale influence, ecological/economic/cultural role, environmental bellwether.

Lake Winnipeg—formed from ancient mega-lake, draining vast interior, facing modern pressures—deserves recognition as North America's overlooked giant.

(~1,100 words; ~10-minute read.)

The Death of Affordable Dining: How Corporate Greed Transformed Restaurants

The restaurant industry has shifted dramatically from serving the working class to prioritizing corporate profits. Menu prices are projected to rise another 30% in 2026, while fast food has already increased nearly 50% in the last decade—often outpacing inflation by 3x. This video explores how consolidation, cost-cutting, and shareholder focus eroded value, quality, and affordability.

Historical Roots: Built for the Working Class

Post-WWII America marketed the "American Dream" of homeownership and consumerism, with fast food as an affordable, quick alternative for workers. McDonald's epitomized this: a family of four could eat in under a minute for less than $1 (adjusted for inflation, far cheaper than today). The Egg McMuffin (1975: 63¢) and $1 Happy Meal captured morning and family markets.

Value menus (McDonald's, Burger King, Wendy's) drove competition in the 1980s–90s, pressuring local restaurants. Chains expanded massively: McDonald's to ~30,000 locations, Burger King ~11–12,000, Wendy's ~6,000 by early 2000s.

Decline of Independent Diners

Traditional diners—once affordable gathering spots—fell from ~6,000 (mid-20th century) to ~2,500 (mid-2000s). Chains captured 60%+ of profits despite independents being the majority of locations.

Corporate Consolidation & Price Fixing

Meatpacking monopolies (Tyson, JBS, Cargill, National Beef) control ~85% of US beef (up from 36% in 1980). Allegations of coordinated supply cuts inflate prices. Similar patterns in pork/chicken. Ranchers/farmers squeezed; consumers pay more for lower-quality factory-farmed meat.

Quality Drop & Factory Food

Chains rely on processed ingredients (e.g., Tyson chicken for McDonald's, KFC). US chain meals higher in calories/fat/sugar/sodium than UK counterparts. Transparency lost: White Castle (1921) built open kitchens to prove quality; today, customers pay premium for mystery meat.

Tipping & Labor Strain

CEOs earn 300–7,000x median worker pay. Chains push tipping (now ~20% average) to subsidize wages instead of raising base pay.

Automation & Kiosks

Burger King plans 100% digital (kiosks) in $400M rebrand. Chains cut labor costs while raising prices.

Local Impact & Hope

Patrick Terry (Pete Terry's Burgers, 37 locations, 1,300 employees) prioritizes fair wages, quality, customers. Uses family-owned processors, accepts lower margins to keep prices reasonable. Sees corporatism "sucking the country dry."

Terry: Chains lost value-menu customers; now scrambling to win them back.

Call to Action

Support local/ethical restaurants prioritizing quality/fairness over shareholder greed. Small actions (visiting, sharing, appreciating) matter. In a consolidating economy, independent businesses preserving community are worth protecting.

The industry once served workers affordably—now it serves profits. Greed, not inflation alone, drives the crisis.

(~1,400 words; ~10-minute read.)

Comments

Post a Comment