12/26/2025 Youtube video summaries using Grok AI

Overcoming the Character Trait That Can Ruin Your Life: Letting Your Struggles Define Your Identity

In this deeply personal message (originally shared in a video transcript), the speaker draws from his own hard-earned life lessons to warn about a subtle but destructive mindset: allowing your identity to be entirely shaped by your struggles—whether past traumas or ongoing hardships. He argues that this single character trait can isolate you, perpetuate unhappiness, and send your life into a downward spiral. Yet, he emphasizes that it is possible to overcome it, and doing so can transform your outlook and future.

The Core Problem: Identity Tied to Suffering

Many people, often without realizing it, build their entire sense of self around what they’ve endured or are currently enduring—abuse, loss, failure, chronic illness, financial ruin, or family challenges. This becomes their “story,” the lens through which they view everything. The speaker acknowledges that real pain is valid and profound; he’s experienced it firsthand:

- The loss of loved ones

- Financial devastation

- Raising a daughter with autism for over two decades

He stresses that he’s not minimizing anyone’s suffering or speaking from a place of privilege. Instead, he’s speaking as someone who has walked through darkness and learned that clinging to pain as identity only deepens the darkness.

When struggles become “who you are,” several negative consequences follow:

- Isolation: Friends and family grow exhausted by constant focus on the pain, especially when efforts to help are rebuffed. The person becomes “inconsolable,” pushing others away.

- Perpetual Victimhood: You begin to see yourself as perpetually beaten down, tired, and hurt, reinforcing a cycle of negativity.

- Downward Spiral: Life doesn’t improve; it worsens because energy is poured into protecting and reinforcing the “wounded” identity rather than moving forward.

The speaker observes that people will fiercely defend their identity—even a damaging one—because letting it go feels like losing part of themselves.

The Trap of Seeking Attention Over Improvement

In moments of deep hurt, some crave attention or sympathy more than actual healing. This isn’t said condescendingly; the speaker admits he’s been there. When you’re at your lowest, immediate gratification (validation from others, venting, or even destructive habits) can feel like the only relief available. But it keeps you stuck.

The Way Out: A Shift in Mindset and Pursuit

The speaker shares how he personally broke free: by choosing to pursue what is right rather than chasing happiness directly.

- Pursuing happiness as a primary goal often leads to disappointment—you fixate on the life you “should” have had and mourn what’s missing.

- Pursuing righteousness (doing what’s good, moral, and meaningful) naturally brings fulfillment and moments of joy as byproducts, without the false expectation that life should always feel good.

Key insights he’s learned:

- For every negative reaction possible, there’s an opportunity for a positive one instead.

- The list of good things still possible in life—and the good already present—far outweighs the struggles when you choose to see them.

- Embracing the life you actually have, rather than resenting the one you wanted, is liberating.

He celebrates the power of deciding not to lie down and die because of what you’ve been through. Rising up, going against the grain, and determining that your life will be defined by more than heartbreak is transformative.

Hope and Redemption

The closing message is one of encouragement: You are still here. Your heart is still beating. You can fight back. You can still do good. Redemption lies ahead.

Change may not happen overnight—it takes time and deliberate effort—but the moment you stop identifying solely with your pain and start embracing possibility, everything begins to shift.

Final Takeaway

Don’t let this one trait ruin your life. Recognize if your struggles have become your identity, and make the personal decision to redefine yourself. Choose action over victimhood, righteousness over fleeting happiness, and gratitude over grievance. In doing so, you reclaim your life and open the door to a future that isn’t dictated by the past.

(This summary distills the original message into a concise, reflective piece designed to be read in about 10 minutes while preserving the speaker’s authentic voice, empathy, and urgency.)

How Money Really Moves Between Countries: The Invisible Global Plumbing System

Have you ever wondered how a sneaker buyer in New York pays a factory in Vietnam, or how an expatriate in Dubai sends money home? Every day, roughly $5–6 trillion flows across borders in international transactions. Yet, contrary to what most people imagine, almost none of this money physically moves. No planes loaded with cash, no ships carrying pallets of banknotes. Instead, the global financial system operates on ledgers, trust, and information. Understanding this hidden infrastructure reveals how modern international business truly works—and why some people and companies succeed globally while others fail.

1. The Ledger Illusion: Money Doesn’t Travel, Ownership Does

When a Seattle coffee shop pays $10,000 to a Colombian bean farmer, you might picture dollars journeying south and being converted to pesos. In reality:

- The U.S. bank debits the coffee shop’s account.

- It instructs a correspondent bank in Colombia to credit the farmer’s account with the equivalent in pesos.

- Ledgers update on both sides. The money itself never leaves the banking system.

International payments are almost entirely accounting entries—numbers shifting in databases. Physical cash is rarely involved. What “moves” is the claim or ownership of the money.

This system works only because banks trust each other to honor these instructions. Remove trust, and the entire network freezes.

2. The Currency Dance: The World’s Largest Market

Most transactions involve different currencies. The Seattle shop has dollars; the Colombian farmer wants pesos. Someone must exchange one for the other.

Enter the foreign exchange (FX) market—the biggest financial market on Earth, trading about $6 trillion daily. It’s a vast, decentralized swap meet where participants trade currencies based on supply and demand.

- Exchange rates fluctuate constantly, second by second.

- These rates influence everything: the price of imports, the affordability of foreign vacations, the competitiveness of exports, and even geopolitical power.

High demand for a currency makes it stronger; low demand weakens it. The FX market self-regulates through millions of daily trades.

3. The Correspondent Banking Network: The Hidden Infrastructure

Most banks don’t have branches in every country. A small Texas bank has no direct presence in Thailand or Vietnam. So how do transfers happen?

Through correspondent banks—large global institutions (e.g., Citibank, HSBC, JPMorgan Chase) that maintain relationships with banks worldwide.

- Your local bank routes the payment instruction through one or more correspondent banks.

- Each link in the chain charges a fee, explaining why international transfers often cost $20–50.

- The network functions like the internet: payment instructions (not money) travel through “routers” (banks) using “addresses” (account numbers).

This invisible web enables global commerce but adds cost, complexity, and delay.

4. SWIFT: The Texting System for Banks

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is the standardized messaging network banks use to communicate payment instructions.

- A bank in the U.S. sends a SWIFT message to a bank in Japan: “Please credit this account with X amount in yen.”

- The format is universal, preventing chaos from thousands of custom protocols.

- SWIFT messages are near-instantaneous, but actual settlement—updating all ledgers across correspondent banks—can take days.

SWIFT is also a geopolitical lever. Excluding a country’s banks (as happened to some Russian banks) effectively isolates them from global finance.

5. The Settlement Problem: Balancing the Global Ledger

Countries continually track flows via the balance of payments (imports, exports, investments, remittances, tourism).

Persistent imbalances can’t last forever:

- Too many U.S. imports from China → China accumulates dollars, U.S. needs more yuan.

- Adjustment mechanisms:

- Exchange rates shift (yuan strengthens, making Chinese goods pricier).

- Central banks use foreign exchange reserves (huge holdings of other currencies) to smooth imbalances.

The U.S. dollar’s status as the world’s primary reserve currency gives America enormous advantages: lower borrowing costs, ability to run deficits, and influence over global finance. But it also makes the system dependent on dollar stability.

The Fragility Beneath the Surface

The entire apparatus—$5–6 trillion daily—runs on confidence:

- Banks trust counterparts.

- Countries honor obligations.

- Exchange rates adjust gradually.

- Institutions function reliably.

When trust erodes (banking crises, debt defaults, wild currency swings), the system seizes up quickly.

Real-World Impact: Two Businesses, Two Outcomes

Marcus ran a U.S. online clothing brand. When European orders arrived, he assumed international payments would work like domestic ones.

- His processor struggled with euros.

- He priced only in dollars, causing erratic pricing abroad.

- High fees (4–5%) and unpredictable settlement times eroded margins.

- After six frustrating months, he abandoned international sales.

Jennifer sold digital graphic design courses. Before expanding globally, she studied the system.

- She set stable local-currency pricing and adjusted quarterly for exchange rates.

- She chose specialized cross-border payment processors with lower fees and faster settlement.

- She planned cash flow around known delays (3 days from Europe, 4–5 from Asia).

Result: Within a year, 40% of her revenue came from international customers, and her business thrived.

The difference wasn’t luck, talent, or capital—it was understanding the rules of the game.

The Bigger Picture: Information, Not Money, Moves

At its core, international money transfer is about information flow:

- Instructions, authorizations, verifications.

- Messages racing at light speed through cables and SWIFT.

- Coordination and ledger reconciliation taking days.

The money mostly sits in bank accounts and reserves. What changes is who owns it.

This insight empowers individuals and businesses:

- Choose better payment providers.

- Time transfers for optimal exchange rates.

- Minimize fees and plan around delays.

- Grasp why sanctions work, why reserve currencies matter, and how global trade functions.

Final Takeaway

The global financial plumbing is remarkable: trillions flowing daily through ledgers, trust networks, and standardized messages, enabling modern commerce. Yet it’s more fragile than it appears, resting on shared confidence.

Whether you’re a business owner eyeing international markets, sending remittances, or simply curious, understanding this system gives you an edge. The winners in global commerce aren’t always those with the most money—they’re the ones who understand how money truly moves.

(This summary distills the original explanation into a clear, engaging article designed for a ~10-minute read, preserving the wonder, key examples, and practical lessons.)

Are You Really Lazy? The Truth About Environment and Achieving Success

If you've ever labeled yourself "lazy" despite having ambitious dreams, this message challenges that notion head-on: Laziness isn't an inherent flaw—it's often a symptom of being in the wrong environment. Success isn't solely about ironclad discipline; it's profoundly shaped by proximity—the people, places, and systems around you. By intentionally curating your surroundings, stealing ambition from high performers, and building supportive habits, you can unlock greater productivity, wealth, and freedom.

Proximity Equals Performance: The Contagious Nature of Success (and Failure)

Research backs this up strongly. A study from the Kellogg School of Management found that sitting within 25 feet of a high performer boosts your own productivity by about 15%, thanks to spillover effects like inspiration and peer pressure.

Conversely, proximity to toxic or low-performing individuals can drag performance down by up to 30%.

Success is contagious, but so is mediocrity—or worse. Your neighbors, friends, and colleagues profoundly influence outcomes.

Studies on economic connectedness (from Opportunity Insights, led by Raj Chetty) show that children from similar backgrounds achieve vastly different incomes in adulthood based on the socioeconomic diversity of their networks—cross-class friendships are one of the strongest predictors of upward mobility.

Living in areas with higher economic connectedness can lead to significantly better life outcomes, far outweighing many other factors.

Outwork These Three People (Not the Entire World)

You don't need to grind harder than everyone else to succeed—just these key figures:

- Past You — The version who procrastinated on hard tasks (gym, early mornings, late nights). Outwork them by consistently choosing discomfort today.

- The Person Who Has What You Want — Study their mindset, sacrifices, and execution. Then do 10% more—one extra call, rep, or effort.

- The Doubter Counting on You to Quit — Prove them wrong through relentless showing up.

Do this consistently, and you'll gain not just wealth, but freedom.

Curate Your Circle: Seek Allies, Not Just Friends

Surround yourself with people you admire for at least one standout trait (humor, intelligence, success, drive). A-players seek other A-players to win big; lower performers avoid threats to their ego.

Find allies who push you—like a partner who drags you to workouts or shares growth hacks.

Avoid starting your day with your phone; it floods your mind with negativity from people you don't even like (as Mel Robbins advises—charge it in another room).

The Wealth Triangle: The Three Key "Whos" for Getting Rich

It's rarely "how"—it's "who":

- Mentor → Provides wisdom and shortcuts (e.g., seasoned entrepreneurs who've built empires).

- Investor → Sees leverage and opportunity where others see risk; provides capital and growth mindset.

- Operator → The executor who turns ideas into reality.

Protect your plans like equity—share only with proven investors in your vision.

The Power of Place: Clean Spaces for Clear Minds

Your physical environment matters immensely. Princeton Neuroscience Institute research shows that visual clutter overloads your brain's visual cortex, competing for attention and reducing focus and productivity.

A messy desk creates "cortex overwhelm," leading to stress and impaired performance.

In contrast, clean spaces promote clarity and control. Surveys (e.g., from Staples) indicate that 94% of workers feel more productive in tidy environments.

Adopt rituals:

- The five-minute rule — Clean and organize your desk at day's start and end.

- Lay out gym clothes annoyingly to force action.

- Pair tough tasks with rewards (wine, candles, favorite shows) to build positive associations.

As Jordan Peterson famously said: "If you want to change the world, start by cleaning your room."

Steal Ambition Through Systems and Communities

You rise (or fall) to your systems, not just goals. Attend events, join rooms with ambitious people, and "steal their homework"—processes, hacks, and drive.

Rituals breed discipline; proximity in high-energy groups multiplies opportunities (mentors, investors, collaborators).

Final Takeaway: You're Not Broken—You're Misplaced

Laziness often masks environmental mismatch. By choosing better rooms, allies, and habits, you can redefine your trajectory. Start small: Clean your space, seek one admirable influence, outwork your past self today. Over time, these shifts compound into extraordinary results.

(This summary captures the motivational essence of the original talk in an engaging, structured ~10-minute read, with supporting evidence for key claims.)

Taiwan's $40 Billion Defense Boost: A Declaration of Readiness in the Face of Rising Threats

Taiwan has just unveiled a staggering $40 billion U.S. boost to its defense budget—the largest sustained military investment in its modern history. This isn't a distant plan; it's immediate action, part of a broader push to reach 5% of GDP on defense by 2030. At the heart of this move is a stark reality: 2027, the year Chinese President Xi Jinping has targeted for the People's Liberation Army (PLA) to be fully prepared to seize Taiwan. This announcement sends a clear message to Beijing: If you come for us, we're ready. But it also reassures allies like the U.S. and Japan that Taiwan is committed to its own defense. Let's break down the strategic, historical, and geopolitical implications.

Why Now? The Evolving Threat Landscape

For over four decades, peace across the Taiwan Strait has rested on two key U.S. pillars: the 1979 Taiwan Relations Act, which commits America to support Taiwan's defense, and Ronald Reagan's 1982 Six Assurances, which clarified that the U.S. wouldn't pressure Taiwan to negotiate with China or alter its arms sales policy. These frameworks emphasized deterrence through strength, fostering stability.

Today, that stability is under siege. China is amid an unprecedented military buildup, with record PLA incursions into Taiwan's air defense identification zone—sometimes hundreds in a single month. Beijing's aggression extends beyond Taiwan: militarizing the South China Sea, intimidating Japan and the Philippines, and challenging the post-World War II international order. Xi's internal plans explicitly aim for PLA readiness by 2027, not as speculation but as documented strategy.

Taiwan's President Lai Ching-te (often referred to as William Lai) sees this $40 billion infusion not as a knee-jerk reaction but as strategic continuity—reinforcing the principles that have preserved peace while adapting to heightened risks.

Internal Challenges: Politics and the Illusion of Dialogue

Taiwan's defense push comes amid domestic turbulence. The legislature is fractured, with opposition parties like the Kuomintang (KMT) favoring closer ties to China, including high-profile visits to the mainland. There's suspicion of Chinese Communist Party (CCP) influence operations, and a minority of politicians advocate more "talks" with Beijing.

The issue? China's version of dialogue demands Taiwan first acknowledge it's part of "one China"—essentially forced surrender disguised as diplomacy. Former President Ma Ying-jeou (KMT) recently criticized the budget, arguing it leads to a "dead end" and pushing for reconciliation. But this mindset is outdated, rooted in a pre-Xi era when China feigned global cooperation. Under Xi, China has crushed Hong Kong's freedoms, erased opposition, stifled the press, and turned a thriving financial hub into a shrinking economy plagued by issues like recent massive fires symbolizing broader decay.

Ma's talking points ignore 2025's realities: constant PLA drills simulating invasions, normalized incursions, and threats to regional neighbors. If Taiwan doesn't build credibility through capability, it risks collapsing quickly in a conflict—leaving no time for allies to intervene.

Reassuring Allies: The U.S. and Japan Watch Closely

The U.S. stance is unambiguous: Washington will assist Taiwan, but only if the island demonstrates the will and means to defend itself first. As America reduces commitments in Europe and the Middle East to focus domestically, it's urging allies to share more responsibility—a echo of Reagan's 1980s logic.

Japan views the stakes even more acutely. Former Prime Minister Yoshihide Suga once stated that a Taiwan crisis is a Japan crisis, prompting Chinese backlash. Geographically, a Taiwan Strait conflict threatens Japan's shipping lanes, Okinawa's security, and national survival. Taiwan's budget boost reassures Tokyo and Washington: We're a reliable partner, prepared to fight first, not just rely on you.

Breaking Down the $40 Billion Investment

Taiwan's defense spending has already doubled recently, hitting 3.3% of GDP next year and targeting 5% by 2030. This isn't tinkering—it's a historic transformation. Key elements include:

- Major Weapons and Asymmetric Warfare: The bulk funds U.S. acquisitions like missiles and AI-driven platforms. Emphasis on "asymmetric capabilities" (e.g., mobile, hard-to-target systems) raises the cost and uncertainty of any PLA assault, deterring invasion through high risks.

- TDOM Missile Defense System: Accelerating development of the Taiwan Defensive Operation Missile (TDOM), a multi-layered shield against missiles, rockets, drones, and aircraft. It's Taiwan's "unbreakable sky shield," inspired by systems like Israel's Iron Dome but tailored to PLA threats.

- Whole-of-Society Resilience: A new top-level committee coordinates government, military, and civilians for cyber defenses, wartime emergencies, and societal preparedness. This holistic approach ensures Taiwan can withstand prolonged pressure.

These investments signal Taiwan's shift to a "quasi-war state," acknowledging that normalized PLA aggression isn't mere tension—it's active preparation for conflict.

The Broader Geopolitical Message: Peace Through Strength

Taiwan isn't provoking China; it's asserting sovereignty and survival. This aligns with Reagan's Cold War philosophy: Peace through strength, where deterrence stems from credible capability, not compromise. Look at Hong Kong as Beijing's "template" for Taiwan—eroded freedoms, economic decline, and authoritarian control. Taiwan rejects becoming "Hong Kong 2.0."

International partners recognize the urgency, issuing statements on Taiwan Strait stability. This unity arises from Taiwan's leadership: demonstrating action, not just pleas for help.

The only lingering question: When will Taiwan's domestic skeptics grasp the moment? Illusions of appeasing China ignore its worsening behavior. Nations that don't defend themselves don't endure in an era of authoritarian expansion.

Final Takeaway

Taiwan's $40 billion defense surge is a bold declaration: We will not be taken quietly. It reinforces decades-old deterrence while adapting to 2027 threats, reassures allies, and builds resilience. In a world where force increasingly challenges order, this move exemplifies preparation over provocation—ensuring Taiwan's democracy survives.

(This summary distills the original analysis into a concise, insightful piece for a ~10-minute read, maintaining the urgency and strategic depth.)

How to Replace Your 9-to-5 Income with Day Trading: A Realistic Framework for Part-Time Success

A full-time day trader with over five years of experience (and more than $500,000 earned in the past year) shares a practical, no-hype guide to becoming consistently profitable—even while holding a job or running a business. The key message: Day trading can replace your income, but it requires the right mindset, realistic expectations, disciplined habits, and a marathon approach. Most people fail because they chase flashy results seen on social media. This framework focuses on sustainable, repeatable progress instead.

1. Reset Your Expectations: You Don’t Need $5,000–$10,000 Days

Social media floods you with traders posting massive daily profits, creating unrealistic benchmarks. The truth:

- A comfortable six-figure income ($100,000/year) requires only $398 per day on average (assuming 252 trading days).

- That’s achievable with 1–3 solid trades per day—no need for home-run 300% winners.

Start smaller:

- Aim for $50/day consistently → scale to $100 → $150 → $200 → $300+.

- Focus on small, repeatable wins rather than P&L obsession.

- Prioritize risk management and process over immediate big money.

With a job providing steady income, you face zero pressure to pay bills from trading. Treat it as an investment in a long-term skill—success may take 6–12 months or longer, but rushing leads to blowups.

2. Time Commitment: Part-Time Trading Works

You don’t need to trade full market hours every day. A realistic part-time schedule:

- Trade 2–4 days per week.

- Allocate 2–3 hours per trading day (ideally the morning session, 9:30 a.m.–12:00 p.m. ET, when volume is highest).

- Remote workers have a huge advantage—trade mornings, work afternoons.

Daily routine example:

- Pre-market (15–30 minutes): Build watchlist, identify 2–4 high-probability stocks, mentally prepare.

- Trading session: Execute your plan.

- Post-market/evening: Journal trades, review mistakes, refine entries/exits.

- Weekends/off-hours: Backtest, study charts, use tools like Thinkorswim’s OnDemand feature for replay practice.

Repetition builds pattern recognition. Even limited screen time compounds into mastery.

3. Keep It Simple: Master One System

Complexity kills beginners. Avoid jumping between strategies, mentors, or indicators.

Recommendations:

- Focus on 1–2 high-probability setups.

- Use minimal tools (e.g., 20-period and 200-period simple moving averages).

- Develop clear, structured rules for entries, exits, trade management, and stops.

- Risk a consistent small amount per trade (e.g., $50–$100 to start).

Simple setups + consistent execution = repeatable wins. Upgrade your setup (multiple monitors, etc.) only after profitability.

4. Rules Before Quitting Your Job

Never go full-time prematurely—most blowups happen from pressure. Strict prerequisites:

- 6–12 months of living expenses saved → Eliminates “scared money” decisions.

- Strategy proven across market conditions → Bull runs (post-COVID) made many look genius; bear markets exposed flaws.

- Survived and recovered from a drawdown/setback → Builds psychological resilience.

- No tilting after losses → Prove you won’t revenge-trade or gamble profits away.

- Financial and emotional comfort → You must trade calmly, not out of survival need.

“Scared money doesn’t make money.” Quit only when trading feels secure and pressure-free.

5. Common Beginner Mistake: Scaling Risk Too Fast

Confidence from early wins tempts aggressive sizing. Resist:

- Establish consistency at small risk first ($50/trade).

- Only increase after proven stability (weeks/months of green results).

- Scale gradually: $50 → $100 → $200, etc.

Rushing size without consistency leads to large losses that erase progress.

6. Focus on Process, Not Outcome

Detach from monthly P&L goals. Early progress often shows in skill, not dollars.

Prioritize:

- Building disciplined habits.

- Refining your trading plan.

- Mastering risk management.

- Distinguishing high- vs. low-quality setups.

Results lag effort. Many quit after weeks of hard work because profits haven’t materialized—yet skill is improving rapidly. Stay process-oriented; the income follows naturally.

Final Summary: Treat Trading Like a Career

Day trading is a legitimate, learnable profession—not a get-rich-quick scheme. Success demands:

- Discipline, consistency, and patience.

- Realistic goals ($398/day for six figures).

- Part-time routine (2–4 days/week, 2–3 hours/day).

- Simplicity and mastery of one system.

- Financial buffer before going full-time.

- Process focus over instant riches.

With a job covering bills, you have the luxury of time. Invest in yourself slowly, scale cleanly, and let your edge compound. In 6–18 months, trading can become a strong side income—or fully replace your 9-to-5.

The trader emphasizes free resources (a 10+ hour course and YouTube videos) to learn his exact methodology, proving you don’t need expensive programs to start.

This approach demystifies day trading, making six-figure potential feel achievable through steady, intelligent effort rather than gambling or hype.

(This summary distills the original video into a clear, motivational ~10-minute read while preserving the speaker’s practical, grounded tone.)

The Federal Reserve's Shift in Monetary Policy: Ending Quantitative Tightening and Initiating Reserve Purchases

In late 2025, the Federal Reserve made a notable policy adjustment that has sparked debate among economists, investors, and financial commentators. After years of quantitative tightening (QT)—shrinking its balance sheet by allowing bonds to mature without reinvestment—the Fed ended QT on December 1, 2025, and began purchasing short-term Treasury securities (primarily bills) to maintain "ample reserves" in the banking system.

This move involves an initial pace of approximately $40 billion per month in purchases, starting December 12, 2025, with plans to taper after addressing seasonal liquidity needs (e.g., April tax season). The Fed describes this as reserve management purchases (RMPs), a technical operation to ensure smooth market functioning and prevent strains in short-term funding markets. However, some media outlets and analysts label it a "restart of quantitative easing (QE)," viewing it as a form of monetary easing outside of a full-blown crisis.

What Is Quantitative Easing (QE) and Why Does the Distinction Matter?

QE is a tool where the central bank buys assets (typically longer-term bonds) to inject liquidity, lower long-term interest rates, stimulate borrowing and spending, and support economic growth—often during crises. It expands the Fed's balance sheet significantly.

In contrast, the current purchases focus on short-term Treasuries to replenish bank reserves depleted by QT and growing non-reserve liabilities (like currency in circulation). The goal is liquidity management, not broad economic stimulus. That said, any balance sheet expansion adds liquidity, which can indirectly ease financial conditions, support asset prices, and risk fueling demand if inflation persists.

Background: From Pandemic QE to QT and Back

- During the COVID-19 pandemic → The Fed's balance sheet ballooned to nearly $9 trillion through massive QE.

- Starting June 2022 → QT reduced it by over $2.4 trillion, bringing reserves down while fighting post-pandemic inflation.

- By late 2025 → Reserves approached levels where money market stresses emerged (e.g., rising short-term rates, usage of emergency facilities). The Fed halted runoff and shifted to reinvestment plus active purchases.

This shift coincides with:

- Inflation around 3% (above the 2% target).

- Unemployment rising to 4.6% in November 2025 (highest since 2021).

- Concerns from Chair Jerome Powell that official job growth figures may overstate gains by ~60,000 per month due to flaws in the Bureau of Labor Statistics' "birth-death" model (estimating jobs from new/closing businesses). This suggests the labor market could be weaker than headlines indicate, potentially showing net job losses in recent months.

Implications for the Economy, Markets, and Individuals

Positive Effects:

- Supports stock markets by lowering short-term yields, encouraging risk-taking, and providing cheaper financing (especially for growth/tech sectors).

- Eases pressure on government borrowing (interest costs >$1 trillion annually).

- Prevents funding market disruptions, maintaining stability.

Risks and Concerns:

- Could prolong inflation by adding excess liquidity when prices are still rising faster than target.

- Complicates the Fed's inflation-fighting efforts, especially with persistent deficits and potential fiscal pressures.

- Stock markets near all-time highs may mask vulnerabilities; high inflation has historically eroded real returns and challenged retirees (e.g., studies behind the 4% retirement withdrawal rule show failures often occur in inflationary periods).

Cumulative inflation since the pandemic has been ~25%, significantly impacting purchasing power (e.g., grocery prices).

Advice for Investors and Retirees

- Diversify and Prepare: Maintain proper asset allocation with buffers (e.g., cash or bonds) to weather potential market drops (20-40%). Avoid being fully invested in equities if a correction hits.

- Retirement Planning: High inflation is a major risk for those in or near retirement. Model scenarios using robust tools (not just spreadsheets) to assess sustainability.

- Caution on Greed: As markets rally on easier policy, remember warnings like Warren Buffett's: "Be fearful when others are greedy." Have "dry powder" for opportunities in downturns.

- Broader Outlook: This policy offers a compromise amid Fed divisions—easing without aggressive rate cuts. It supports growth and jobs but risks "supercharging" inflation if not managed carefully.

This development reflects a pragmatic response to evolving liquidity needs rather than a full crisis-mode QE restart. Still, it underscores ongoing challenges in balancing growth, employment, and price stability in a post-pandemic economy with elevated debt and inflation pressures.

(Approximate reading time: 10 minutes)

Trading: The Hardest Way to Make Easy Money

Trading financial markets is often portrayed as a quick path to wealth, but in reality, it’s one of the most challenging ways to earn a living — and paradoxically, once mastered, one of the easiest and most rewarding. The key lies in understanding why traditional employment limits your earning potential and how trading, when approached correctly, breaks those constraints.

The Limitations of Trading Time for Money

Most people earn income by exchanging their time for a paycheck. For example:

- Work 8 hours a day at $20/hour → $160/day, $800/week, roughly $3,200/month.

Pros of this model:

- Stability and predictability: As long as you show up, you know exactly how much you’ll earn each pay period. No surprises, no uncertainty about covering bills.

Cons — the fatal flaw: lack of scalability There are only two realistic ways to earn significantly more in a traditional job:

- Work more hours Shifting from 40 to 60+ hours per week can increase income temporarily, but it’s unsustainable long-term. It sacrifices family time, health, hobbies, and overall quality of life. Few people want their entire existence to revolve around work.

- Earn promotions or raises

Becoming exceptionally skilled might lead to a higher position and a 10–30% raise (50–70% is rare). However:

- Promotions often require disproportionate extra effort, unpaid overtime, and increased stress.

- The raise rarely matches the added responsibility (e.g., 100% more stress for 20–30% more pay).

- Many companies prioritize profits over employee loyalty. Dedication doesn’t guarantee recognition or job security.

- External threats like automation and AI are accelerating job displacement — even skilled professions (e.g., engineering) are being replaced.

In short, linear income (time → money) caps your earning potential at the number of hours you can physically work and the incremental raises your employer is willing to give.

The Power of Asymmetrical Income: Getting Paid for Skill, Not Time

True wealth comes from activities where income is not directly tied to hours worked — where effort compounds and rewards can be exponentially higher.

Trading, when treated as a serious profession, fits this model perfectly. You are essentially running your own business:

- You are the CEO, risk manager, analyst, and executor.

- Income depends on skill, discipline, and execution — not clocked hours.

Most aspiring traders fail because they treat it like a hobby or gambling:

- No plan

- Poor risk management

- Random entries and sizing

- Expecting instant profits

Successful traders treat it like a business:

- Develop a detailed trading plan

- Strict risk management

- Consistent execution

- Continuous improvement

Real-World Example of Asymmetrical Returns

Boxer Floyd Mayweather earned $50–$250 million for fights lasting 30–60 minutes. Outsiders call it “unfair,” but it’s the result of decades of unseen discipline, training, and mastery. Early in his career, he earned little; later, his skill commanded massive paydays.

Trading follows the same pattern:

- Early stage: Steep learning curve, losses, frustration, no immediate rewards. Requires daily discipline, study, and resilience.

- Mastery stage: Profits feel almost effortless. A trader might spend 2–4 hours analyzing and executing trades and earn thousands in a single session — not because of time invested that day, but because of years of skill development.

The speaker shares his experience:

- Mentored by his father (a major advantage), yet still required years of consistent effort.

- Now consistently profitable (no losing month in over 5 years).

- Can earn significant income in a few focused hours, then have the rest of the day free.

The Trade-Offs of Trading as a Career

What you lose:

- Guaranteed paycheck stability. Even profitable traders have variable monthly income — some months explosive, others slower.

What you gain:

- Scalability: Income potential is limited only by skill improvement and market opportunities.

- Control over destiny: Want to earn more next year? Improve your edge, execution, and risk management.

- Time freedom: Once profitable, trade a few hours daily and use the rest for family, hobbies, or other ventures (real estate, businesses, etc.).

- Location independence and flexibility.

Why Trading Is Worth the Struggle

Trading rewards those with an entrepreneurial mindset:

- Resilience in the face of setbacks

- Willingness to work hard without immediate payoff

- Discipline to follow rules even when emotions pull otherwise

It’s not a get-rich-quick scheme. Success requires:

- Commitment to learning (proper education, not random YouTube videos)

- Patience through the unprofitable beginner phase

- Daily consistency

But for those who persevere, trading becomes one of the most powerful skills on the planet: the ability to generate substantial income in a short time, with full control over your financial future.

Final Thought

Trading is indeed the hardest way to make easy money. The front-loaded difficulty — years of learning, losses, and discipline — filters out most people. Those who break through gain a rare combination of high earning potential, time freedom, and personal autonomy that few careers offer.

If you're willing to invest in mastering a skill that pays asymmetrically rather than hourly, trading can transform from brutal to profoundly rewarding.

(Approximate reading time: 10 minutes)

Why Trading Feels Impossible for 95% — And Obvious (Even Boring) for the Top 5%

Trading financial markets is brutally difficult for most people: 95% blow up accounts, quit in frustration, blame manipulation, algorithms, or "rigged" systems. Yet the remaining 5% find it straightforward, systematic, and predictable — almost dull. They operate in the same markets, with the same charts and opportunities. The difference isn't intelligence (many brilliant PhDs and engineers fail spectacularly), capital (failure rates are similar whether starting with $100 or $100,000), or information access (everyone sees the same data).

The core distinction: The 95% treat trading like a war to win through prediction and control. The 5% treat it like a probability game they've already rigged in their favor through disciplined execution.

Two Traders, Two Outcomes

Consider two real-world examples:

- David, a software engineer, approached trading analytically. His charts were overloaded with 47 indicators — moving averages, RSI, MACD, Fibonacci, Bollinger Bands, volume profiles, order flow, and more. He spent hours daily on economic calendars, reports, sentiment analysis, and institutional positioning. After 18 months, he blew four accounts totaling $65,000.

- Sarah, a former casino dealer with no formal finance background, understood one truth: The house wins via a consistent edge, not emotion. Her system had just three rules: Trade only in specific high-edge hours; risk exactly 1% per trade; exit at predetermined levels (win or loss). No extras. After 18 months, her account grew 42%.

The pattern: Complexity destroys; ruthless simplicity sustains.

Why Trading Feels Impossible: The Five Psychological Traps

Trading violates ingrained ideas about success (more effort = better results). Here are the key reasons most struggle:

- The Uncertainty Paradox Most jobs offer structure and predictability. Trading has none — every decision is yours, outcomes probabilistic. Brains crave certainty, so traders pile on indicators and analysis to "predict" the unpredictable. Reality: No one knows the next move. The 5% accept uncertainty and focus on reacting to high-probability setups.

- Instant, Brutal Feedback Unlike careers with delayed results, trading delivers immediate P&L hits, triggering survival instincts (fear, greed). Losses feel personal; traders move stops or revenge-trade. The 5% detach: One trade is noise; consistency over hundreds matters.

- Complexity Addiction Brains equate complexity with progress (new indicators feel productive). But markets reward execution, not intellect. Overloading charts leads to paralysis. The 5% embrace simplicity as executable under pressure.

- Outcome Obsession Checking balances constantly ties self-worth to uncontrollable results. Wins inflate ego; losses crush confidence. The 5% measure success by process adherence (e.g., "Did I follow rules?"), not daily profits.

- Information Overload Endless news, newsletters, social media, and analyses create conflicting noise, leading to hesitation or weak conviction. The 5% practice "strategic ignorance" — ignoring everything outside their system.

The Shifts That Make Trading "Obvious"

The top 5% aren't immune to these traps; they've unlearned bad habits:

- Embrace Uncertainty: Shift from prediction to probability. "This setup has an edge; I'll take it knowing I might lose."

- Measure Process, Not Outcomes: Use a checklist for each trade. Success = rules followed, regardless of P&L.

- Simplify Ruthlessly: Strip charts to essentials. Master one strategy, one timeframe, few markets.

- Practice Strategic Ignorance: Cut news and opinions during trading hours.

- Cultivate Patience: Wait for setups. Doing nothing is often the best action. One trader limited himself to 3 trades/day max — win rate rose from 42% to 61%, turning breakeven into consistent profits.

The Deeper Identity Shift and the "Boring" Truth

Successful traders see themselves as disciplined rule-executors, not profit-chasers. Their identity isn't tied to wins/losses, making them resilient.

Ultimately, profitable trading is boring: Hours of waiting, interrupted by mechanical execution.

Excitement signals overtrading and emotion. The 5% thrive on repetition and patience.

David quit, blaming the system. Sarah continues steadily — trading now routine, like brushing teeth.

Your Choice

Continue the 95% path: More indicators, information, trades — fighting uncertainty. Or join the 5%: Simplify, accept probability, execute patiently. The market doesn't care; it keeps providing opportunities. The question is whether you'll have capital and mindset left to capitalize.

Trading becomes obvious when you stop fighting its nature and flow with disciplined simplicity.

(Approximate reading time: 10 minutes)

10 U.S. Cities Experiencing the Sharpest Middle-Class Decline

Over the past two decades, many former industrial strongholds in America have seen their once-thriving middle classes erode dramatically. Factories closed, jobs moved overseas or automated, wages stagnated, and living costs—groceries, utilities, insurance, taxes—rose relentlessly. What remained were affordable homes in places where residents increasingly struggled to afford everyday life. This video from "World According to Briggs" highlights 10 such cities, drawing on resident quotes and economic trends to illustrate the human impact.

Common Themes Across These Cities

- Deindustrialization: Heavy reliance on manufacturing (textiles, furniture, auto parts, steel) that collapsed due to globalization, automation, and outsourcing.

- Job Replacement Failure: New roles in service, healthcare, logistics, or retail pay far less with fewer benefits.

- Cost-Wage Disconnect: Essentials rose faster than incomes, turning "affordable" housing into a trap ("Cheap mortgage, expensive life").

- Data Context: Many align with Pew Research (2016) findings of sharp middle-class drops in Rust Belt and Southern industrial towns; recent studies show ongoing challenges in similar areas.

The Countdown

10. Rocky Mount, North Carolina Once a textile hub, mills closed in the early 2000s. Manufacturing employment fell from ~22% in 1999 to 11.6% by 2024. Warehouses replaced factories, but at lower pay. Resident quote: "Rocky Mount didn't get more expensive. My paycheck got smaller."

9. Rockford, Illinois Generations worked in machine tools, aerospace, and auto parts. Outsourcing and consolidation wiped out thousands of jobs. High Illinois taxes compounded the pain. Resident: "I lived in the same house my dad bought in the 1980s... Somehow I'm broke and he retired early."

8. Stockton, California Boomed on construction and agriculture, then devastated by the Great Recession (foreclosure capital, city bankruptcy). Wages lag California's soaring costs. Resident: "We moved here because it was cheaper than the Bay. Now it's not."

7. Mansfield, Ohio Steel, tires, and auto suppliers (including GM stamping plant closure ~2010) vanished. Homes average ~$145,000—affordable, but everything else isn't. Resident: "My mortgage is cheap, my life is not."

6. Fort Wayne, Indiana Downtown revitalization masks fading blue-collar jobs in auto parts and machinery, replaced by lower-wage healthcare/logistics. Rising rents erode affordability. Resident: "People from outside think Fort Wayne is cheap. People who live here know it's not."

5. Michigan City/LaPorte, Indiana Diversified industry (manufacturing, rail, shipping) downsized; leans on tourism and retail now. Pandemic exposed fragility. Homes under $200,000, but wages stagnant. Resident: "It slowly faded like an old photograph."

4. Hickory, North Carolina "Furniture capital" lost tens of thousands of jobs to overseas production and automation (2000–2015). Resident: "We used to make good stuff. Now we can't afford good stuff."

3. Jackson, Michigan Tied to Detroit's auto fortunes; plant closures and automation hit hard. Homes ~$200,000, but rising rents/taxes. Resident: "I can buy a house here. I just can't afford to live in it."

2. Goldsboro, North Carolina Tobacco, manufacturing, and base-related jobs collapsed; one of the largest middle-class drops nationally (2000–2014). Just rising costs, no wage boom. Resident: "Middle class didn't stand a chance."

1. Springfield, Ohio 1980s model city of strong industry and factories. Median income fell >25% (1999–2014)—one of nation's worst. Homes as low as $69,000–$150,000, but jobs scarce. Resident sentiment: Middle class "pretty much gone."

These stories reflect broader U.S. trends: Deindustrialization hollowed out middle-class anchors in many heartland towns. While some revitalization efforts (downtowns, tourism) emerge, replacement jobs rarely match the stability or pay of the past. Affordable housing draws attention, but without living wages, it becomes a mixed blessing.

(Approximate reading time: 10 minutes)

Global Market Update: Key Developments in Europe, North America, and Asia (Late December 2025)

This episode of Market Update covers three major stories shaking financial and geopolitical landscapes as 2025 ends.

France's Budget Crisis: Stopgap Measure Averts Shutdown Amid Political Gridlock

France's fractured parliament failed to agree on a full 2026 budget, forcing Prime Minister Sébastien Lecornu to push through emergency legislation rolling over 2025 spending limits into January 2026.

Both the National Assembly and Senate unanimously passed the "special law" on December 23, allowing tax collection, debt issuance, and basic state functions (policing, education, administration) to continue temporarily. Officials call it a "bare-minimum" fix that leaves the economy "fragilized"—unable to fund new initiatives like teacher recruitment, prison construction, or industrial decarbonization.

Deep divides over tax hikes on the wealthy (favored by center-left) versus spending cuts (pushed by center-right) sank negotiations. The minority government, weakened since President Emmanuel Macron's 2024 snap election loss of majority, risks a no-confidence vote if it forces a budget through without parliamentary approval—a move Lecornu has pledged to avoid.

France faces intense pressure from investors and rating agencies to cut its deficit below 5% of GDP in 2026 (from ~5.4-5.5% in 2025). A prolonged rollover could cost billions and delay ambitions, including Macron's €6.5 billion defense spending boost.

This mirrors last year's crisis, highlighting ongoing instability that has toppled multiple governments.

Compounding tensions, France urged the EU to challenge China's new provisional duties (up to 42.7%) on EU dairy products, calling them "unilateral and unacceptable" retaliation in the escalating EV subsidy trade war.

U.S. F-35 Program Under Fire: Readiness Hits 50% Amid Contractor Criticism

A scathing Pentagon Inspector General report revealed the F-35 stealth fighter fleet—history's most expensive weapons program (~$2 trillion lifetime cost)—achieved only a 50% mission-capable rate in fiscal 2024, far below requirements.

The watchdog blamed poor maintenance by prime contractor Lockheed Martin and inadequate Pentagon oversight. Despite underperformance, the Defense Department paid Lockheed $1.7 billion in sustainment fees without penalties.

Issues persist: Lack of spare parts, weak contract enforcement, and delayed upgrades. The Air Force recently halved its 2026 F-35 purchases due to soaring costs.

Lockheed claims improvements (more parts, better practices, incentive-based contracts). Growing political scrutiny, including from Defense Secretary Pete Hegseth and President Donald Trump, demands accountability over executive perks and stock buybacks.

The findings intensify calls for reform in this troubled program critical to U.S. and allied air superiority.

Japan Approves Record ¥122.3 Trillion Budget Under PM Sanae Takaichi

Japan's cabinet, led by Prime Minister Sanae Takaichi (the country's first female PM, in office since October 2025), approved a record initial budget of ¥122.31 trillion (~$783 billion) for fiscal 2026 (starting April).

This ~6-9% increase reflects Takaichi's "proactive" fiscal stance to spur growth amid entrenched inflation (core prices above 2% for over three years), aging population pressures, and regional security threats.

Key allocations:

- Social security: ¥39.1 trillion (up for healthcare/pensions).

- Defense: Over ¥9 trillion (part of push to 2% GDP).

- New bond issuance: ~¥29.6 trillion (debt reliance dips slightly to 24.2%).

Tax revenues hit record ¥83.7 trillion, aiding restraint on borrowing. Debt-servicing costs soar (assuming 3% rates, highest since 1997) as yields rise.

Markets remain muted but wary of Japan's massive debt (>2x GDP). Takaichi balances stimulus (recent massive package) with "responsible" pledges, rejecting irresponsible issuance.

This first full budget under Takaichi underscores her growth-focused, expansionary approach.

These stories highlight fiscal strains, trade frictions, and defense priorities shaping global markets into 2026.

(Approximate reading time: 10 minutes)

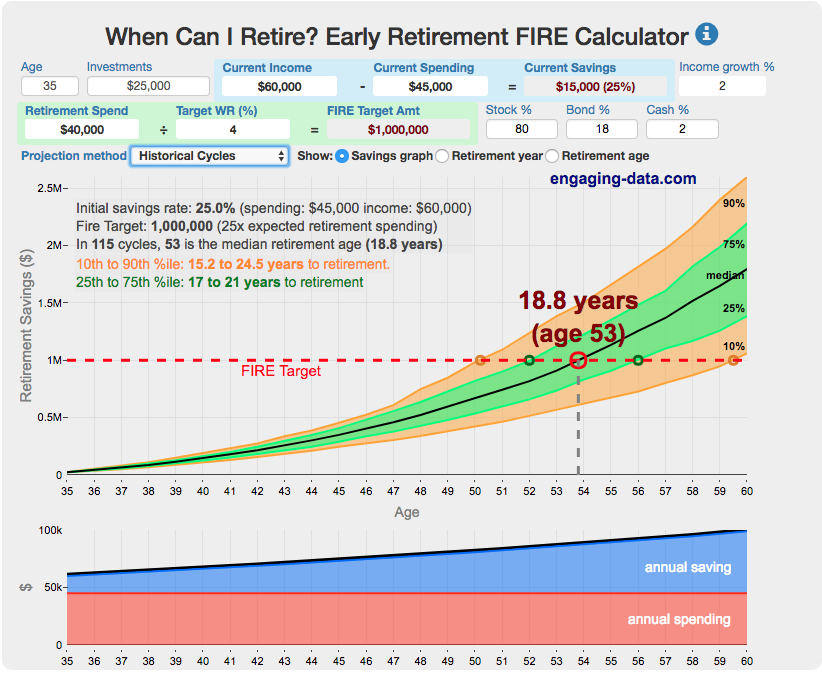

Retiring in 7 Years: The Surprising Math Behind Financial Freedom Through Intense Compounding

Imagine waking up to find your modest savings jar has grown overnight—effortlessly, while you slept. This whimsical analogy captures the essence of compounding, the core mechanism that makes retiring in just 7 years not a fantasy for the ultra-wealthy, but a realistic path for those willing to invest consistently and aggressively. The script challenges common skepticism: Retiring early doesn't require massive starting capital or insider secrets; it's about mindset, math, and momentum. The real barrier? Believing it's impossible without enormous monthly sums. Spoiler: The threshold is lower than you think—$3,000 to $4,000 monthly, scaled with income growth.

Rethinking Retirement: From 40-Year Grind to 7-Year Sprint

Traditional retirement plans stretch over decades, relying on small, sporadic savings that compound slowly. But compressing the timeline demands a paradigm shift: Intensity over longevity. Compounding rewards consistency and scale, not duration. Feed it meaningful amounts regularly, and growth accelerates exponentially—even in a short window.

Consider your baseline: Track expenses for a few months. If they total $2,000–$3,000 monthly ($24,000–$36,000 annually), that's your freedom number—not luxury, but basics covered without a job. Using a conservative 4% safe withdrawal rate (to preserve principal amid inflation and volatility), you'd need a $900,000 portfolio to generate $36,000/year indefinitely.

At first, $900,000 in 7 years sounds daunting. But it's not about raw saving; it's about leveraging compounding at ~7% real annual returns (historical equity average after inflation). Early contributions matter most—they have the longest runway to multiply.

The Magic Number: $3,000–$4,000 Monthly Investments

The script reveals the key figure: To hit ~$900,000 in 7 years, invest $3,000–$4,000 monthly consistently, assuming 7% real returns. Start lower if needed, but ramp up via income growth (job switches, promotions, side hustles like a monetized YouTube channel).

Break it down:

- At $3,000/month: ~$300,000 after 7 years.

- At $4,000/month: Closer to $400,000+.

- Why not enough alone? The portfolio doesn't stop at year 7—it continues compounding. Reinvest dividends, and market gains push it further. A strong year (e.g., 15–20% returns) can add tens of thousands.

This isn't static: Increase contributions as income rises. If you boost from $3,000 to $5,000 mid-journey, you shave months off. Market dips? Opportunities—buy more shares cheaply, amplifying recoveries.

Choosing the Right Tools for Accelerated Growth

Savings accounts (2–3% returns) or bonds won't cut it—they barely beat inflation. Real estate (via REITs) adds complexity and risk. The sweet spot: Broad-market index funds or ETFs (e.g., S&P 500 trackers) for diversified, hands-off 7–10% historical returns.

Avoid stock-picking pitfalls; focus on low-fee, passive vehicles. Reinvest everything—dividends compound the compound. In 7 years, your portfolio shifts from reliant on contributions to self-sustaining.

The Psychological Game: Endurance, Identity, and Opportunity Cost

Retiring early demands more than math—it's psychological warfare. Volatility isn't a foe; it's an ally for buying low. The tipping point: When portfolio growth matches or exceeds contributions, freedom feels tangible.

Shift identity: Become someone who prioritizes future freedom over present impulses. Question expenses not with guilt, but opportunity: That $100 splurge could grow to $200+ in 7 years at 7% returns.

Vividly visualize success: Waking up job-free, investments covering bills. Sacrifices? Investments in a lifetime of autonomy.

Making It Actionable: Start Small, Scale Aggressively

If $3,000–$4,000 feels steep today, focus on income expansion: Learn skills, network, or launch a side gig. The script plugs building a YouTube channel as an "easy mode" accelerator—many blow up quickly with proper strategies.

Consistency trumps perfection. Early years build the foundation; later ones reap exponential rewards. Don't wait for ideal conditions—start now, adjust as you grow.

Final Thoughts: Freedom Awaits the Disciplined

Retiring in 7 years compresses 30+ years of effort into focused action: High contributions, smart investing, and unwavering discipline. It's not luck—it's concentrated compounding. The $3,000–$4,000 threshold proves it's accessible, but requires ditching stagnation for growth.

Ask yourself: Is 7 years of intensity worth lifelong freedom? The math says yes. Act now, or risk regretting inaction.

(Disclaimer: Not financial advice; results vary based on personal circumstances. Approximate reading time: 10 minutes)

My First Year as a Mature-Age Electrical Apprentice in Australia

Starting an electrical apprenticeship in your 30s is a bold career pivot, especially with family responsibilities and a mortgage. This creator, over 12 months into his journey (likely in commercial electrical work), shares candid insights into the realities—far from glamorous, but rewarding for those committed to long-term gains. His experience highlights the physical demands, juggling life commitments, study challenges, financial trade-offs, and mental resilience required.

The Physical Reality of the Job

It's far more demanding than expected. Days involve constant movement: climbing ladders, roughing-in wiring, installing fittings in ceilings, hauling heavy cable drums (50–100+ kg), pulling mains cables, or handling distribution boards.

No sitting by a switchboard all day—expect at least 10,000 steps daily. If you're unfit, it'll be tough; building stamina is essential.

Balancing Work, Family, and TAFE Study

Routine is key. He finishes at 3 PM, home by 3:30, showers/snacks, then studies 4–6 PM (2 hours daily). Dinner and evenings are family time.

Committing blocks for each prevents burnout and maintains balance.

Study struggle: After 15+ years out of school, rote copying didn't work. He adopted active recall—turning notes into questions (e.g., "What is Ohm's Law formula?" instead of just V=IR), then self-testing. This boosted retention dramatically.

Finances: The Biggest Hurdle

First-year pay is low: ~$900–950 weekly (higher for commercial vs. residential; adult apprentices earn more than juniors—around $24+/hour base in 2025). It increases yearly.

Government support helps:

- Australian Apprenticeship Support Loan (formerly Trade Support Loan): Up to ~$22,000–25,000 lifetime, paid monthly; 20% discount on completion.

- Australian Apprentice Training Support Payment: ~$5,000 total (paid every 6 months, tax-deductible/free money).

Budget rigorously beforehand—cut costs, ensure sustainability with dependents. It's a pay cut for career-changers, but qualified electricians earn well ($90k–110k+ average).

Mental and Emotional Side

Tough days bring drain from workload, study, family, or finances—leading to doubt. Counter it by recalling your "why" (north star) and zooming out: 4 years is short vs. 28+ years qualified (e.g., done by 37, retire at 65).

View it as short-term pain for long-term gain: High demand, good pay, variety (commercial, industrial subspecialties), lifelong learning.

Advice for Aspiring Adult Apprentices

Plan finances thoroughly—don't go blind. The industry fascinates with constant challenges and security. Many in their 30s/40s succeed; maturity brings reliability employers value.

This path demands fitness, discipline, and vision—but offers stability and pride in a skilled trade.

(Approximate reading time: 10 minutes)

Exploring the Ward Mining District: Nevada's Best-Preserved 19th-Century Ghost Town and Charcoal Ovens

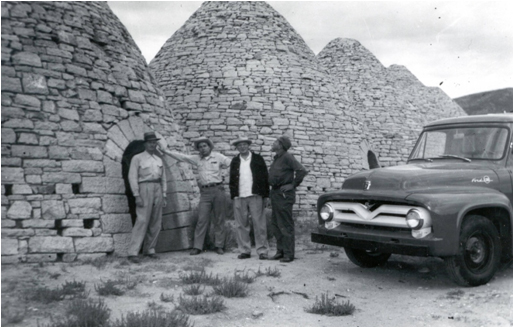

Nestled in the rugged hills of eastern Nevada's White Pine County, the Ward Mining District stands as one of the state's most intact remnants of the Wild West silver boom. This exploration video takes viewers through the abandoned Ward Mine facilities, the faint traces of the once-bustling ghost town, the historic cemetery, and the iconic beehive-shaped charcoal kilns that fueled the operation.

History of the Boom and Bust

Discovered in 1872, rich silver-lead ore sparked a rapid rush. The Ward Mining Company invested heavily: building stamp mills, roads, and water systems. By the mid-1870s, the mine yielded millions in precious metals.

The town of Ward sprang up nearby, peaking at over 1,500 residents by 1877. It boasted stores, saloons, hotels, a school, and even a newspaper (The Ward Reflex). Miners hauled supplies across harsh desert by wagon.

Prosperity faded quickly. A devastating 1883 fire destroyed much of the town, combined with plummeting silver prices and depleting high-grade ore. Attempts to revive operations in the early 20th century failed, and by the 1930s, Ward was fully abandoned.

The Assay Office and Mine Facilities

The explorer focuses on a massive later-era building (likely from a 20th-century revival), contrasting older 1870s ruins. Inside the sprawling assay office:

- Shelves once held thousands of ore samples for testing viability.

- A gutted laboratory with sinks and desks.

- Offices, locker rooms, bathrooms, and showers for workers.

- Scattered sample bags and artifacts litter the floors.

The site includes a water tower (water trucked in) and extensive piping. Most mine shafts are caved in or sealed for safety, leaving surface structures as the main draw.

The Ghost Town Site

Little remains of the original 1870s town—wooden structures rotted away. Durable stone foundations and walls endure, alongside scattered artifacts: rusted cans, glass bottles, and debris piles.

A modern outhouse hints at occasional visitors, but the core townsite is marked by a sign and rocky outlines on the hillside.

Ward Cemetery

About half a mile away, the small cemetery holds graves of ~46 residents, reflecting the era's hardships and violence (common in 1800s Nevada mining camps).

Some headstones are well-preserved or updated (possibly by descendants), with dates from the 1870s–1880s. Wooden markers (rare survivors) and child graves add poignancy.

The Iconic Charcoal Kilns

The highlight: Six beehive-shaped charcoal ovens built in 1876, each ~30 feet tall and remarkably preserved (now part of Ward Charcoal Ovens State Historic Park).

Workers converted thousands of acres of local timber into charcoal to fuel ore smelters. The stone craftsmanship has withstood over 140 years; interiors echo dramatically.

These are among Nevada's best examples, outlasting many similar kilns elsewhere.

Ward's story encapsulates Nevada's mining heritage: explosive growth, environmental toll (deforested hills), tragedy, and swift decline. Today, it offers a serene, evocative glimpse into the past—perfect for history buffs and off-grid explorers.

(Approximate reading time: 10 minutes)

6 Things Women Quietly Love About Men (But Rarely Say Out Loud)

In modern dating, women often respond instinctively to certain male traits that foster connection, safety, attraction, and feeling truly seen—without needing overt performance. These aren't complex demands; they're emotional responses to grounded, authentic behaviors. Courtney Ryan breaks down six such traits that stand out profoundly, even if women don't verbalize them directly.

1. Taking Social Pressure Off Her

Early dating carries invisible tension for both sides: Men feel pressure to lead and impress; women to appear perfect and adaptable. A man who creates a low-pressure environment stands out immensely.

This shows in:

- A calm, steady vibe (not performative or tense).

- Decisiveness (e.g., choosing a restaurant when options overwhelm).

- Adapting to minor hiccups (traffic, delays) without overreacting.

- Not overinterpreting small things (like delayed texts).

It allows her to relax, be playful, and reveal her true self. Women feel this ease deeply, even if unsaid—it's about emotional safety, not fragility. Developing this requires inner work, like therapy for breaking autopilot reactions (sponsored segment on BetterHelp).

2. Noticing the Subtle Stuff

Simple awareness makes women feel truly present-with and valued.

Examples:

- "Your hair looks different today—really good."

- "That perfume smells amazing."

- "Those earrings are cool—are they new?"

It's not about constant compliments or tactics; genuine, effortless observation signals presence. Women love feeling seen (not evaluated), distinguishing real connection from performance.

3. Leading Without Dominating

Balanced leadership is highly attractive but often unvoiced.

Healthy examples:

- Suggesting specific plans (not endless "What do you want?").

- Handling logistics (reservations, transport).

- Proposing ideas then adapting to her input flexibly.

This reduces decision fatigue, signaling competence, confidence, and reliability—without control or ego. Women appreciate direction that honors their voice.

4. Having Standards (Even with Her)

Men with boundaries and self-respect are magnetic, countering the myth that total agreeability wins favor.

Signs:

- Maintaining routines/commitments (not dropping everything last-minute).

- Kindly addressing disrespect.

- Sticking to values/preferences.

It communicates stability and choice (not neediness), making her feel secure in a predictable, non-desperate partner.

5. Subtle Warmth

Warmth—confidence mixed with approachability—is underrated but powerfully attractive.

Manifests as:

- Relaxed expressions and light humor.

- Genuine appreciation.

- Calm interest without guardedness or pushiness.

It lowers defensiveness, signaling emotional maturity—women feel safe opening up without judgment.

6. Consistency Over Intensity

Flashy intensity excites briefly; steady consistency builds deep trust.

:max_bytes(150000):strip_icc()/6-types-of-relationships-and-their-effect-on-your-life-5209431_V1-a0f57cea6a114b9cbfa1553c0142ec92.png)

Key: Actions matching words over time—reliable communication, stable affection, showing up on ordinary days. It creates emotional predictability, reducing anxiety and enabling investment. Great women prioritize this trustworthiness.

These traits aren't about perfection or people-pleasing; they're intentional emotional steadiness that fosters ease and security. Women respond instinctively because they feel calmer and more connected—qualities that naturally elevate attraction in today's dating landscape.

(Approximate reading time: 10 minutes)

Economic Turmoil in Late 2025: Dollar Weakens, Tariffs Backfire, Silver Surges, and Global Shifts Loom

As 2025 wraps up, the U.S. economy faces mounting pressures from a weakening dollar, underwhelming Treasury auctions, escalating tariffs under President Trump, a parabolic silver rally driven by Chinese demand, and potential policy shifts in Japan. This commentary warns of a "doom loop" entering 2026, where structural changes could exacerbate inflation, debt issues, and currency debasement. While some claims (like $18 trillion in tariff revenue) appear exaggerated or misstated, data confirms broader trends of volatility and risk.

The Dollar's Structural Decline: Year 1 of a Multi-Year Downturn

The U.S. dollar index (DXY) has plunged over 10% in 2025—its worst year since 1973—closing around 97-98 by late December.

Options traders remain bearish, anticipating a prolonged cycle lasting 5+ years. Drivers include:

- Federal Reserve money printing, increasing dollar supply.

- Interest rate cuts, reducing bond yields and demand for U.S. assets.

- Trump's tariffs, shrinking global trade and reducing dollar exports (the USD is America's top "export").

This isn't cyclical—it's structural, altering global dollar flows and eroding confidence in U.S. fiscal policy.

Treasury Auction Disaster: Foreign Investors Flee U.S. Debt

Recent 2-year Treasury auctions in December 2025 showed weak demand, with yields around 3.5% and international participation dropping to ~53% (from 57%).

Graded a "D+" for demand, this signals eroding faith amid endless borrowing under Treasury Secretary Scott Bessent. Investors fear elevated yields (keeping bond values low) and a collapsing dollar, making U.S. paper risky even for short-duration notes.

Trump's Tariffs: A "Doom Loop" of Inflation and De-Dollarization

Trump's "Liberation Day" tariffs (April 2025) imposed broad import taxes, aiming to cut trade deficits and revive industry.

Impacts:

- U.S. imports from China dropped from ~25% to 8.4% share, accelerating decoupling but spiking inflation (e.g., 45% duty on a $59 item).

- Trade deficit narrowed, but overall deficits grew; global trade volumes fell, reducing dollar outflows.

- Consumer "backlash": Higher prices transfer wealth to the government, yet borrowing escalates.

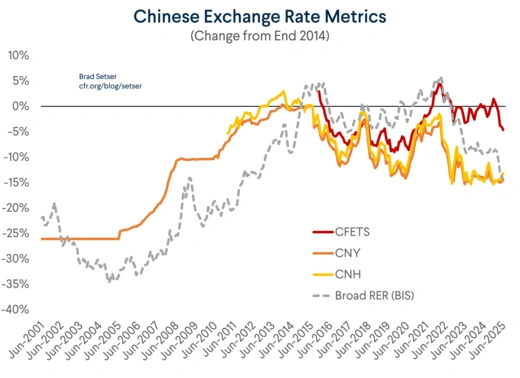

Ironically, tariffs strengthen China's yuan (up 4% vs. USD in 2025, past 7 per dollar), pushing Beijing to "yuan-ize" trade.

As the world's manufacturer, China's shift reduces global dollar demand— a "virtuous cycle" for the yuan but a threat to USD hegemony.

Silver's Parabolic Rally: Debasement and Shortages Drive 150% Gains

Silver has skyrocketed to $73-74/oz by late December, up ~150% YTD—its best year ever—amid dollar debasement and supply-demand imbalances.

Factors:

- Global shortages: Mine supply lags demand; fifth straight deficit year.

- China's mania: Industrial/investment surge for chips, solar, defense; local prices hit $80/oz (10% premium), funds oversubscribed with 60% premiums.

- Strategic stockpiling: U.S./China race for critical metals (silver, rhodium, palladium, platinum).

While corrections loom (parabolic charts invite pullbacks), long-term dynamics favor higher prices as silver becomes a "strategic metal."

Japan's Cornered BOJ: Rate Hikes and Potential Treasury Dump Threaten USD

The Bank of Japan (BOJ) hiked rates to 0.75% in December—highest in 30 years—but the yen hasn't rallied significantly, keeping import costs high and inflation persistent.

To save the yen:

- More hikes signaled for 2026 (potentially to 1%).

- Unwind yen carry trade: Narrowing U.S.-Japan yield gaps push funds out of USD assets.

Critically, Japan may sell U.S. Treasuries (from massive reserves) to intervene in forex or retire debt—flooding markets and pressuring USD bonds. This, amid U.S. tariffs, amplifies global risks.

Outlook for 2026: A Perfect Storm?

The transcript paints a dire picture: Tariffs ignite inflation and de-dollarization, silver signals shortages/debasement, and Japan's moves could trigger Treasury dumps. While exaggerated (e.g., no $18 trillion revenue), data supports weakening USD, tariff pains, and commodity frenzy. Investors: Brace for volatility; diversification into metals or alternatives may hedge risks.

(Approximate reading time: 10 minutes)

9 "Sweet Lies" Women Tell When Using a Man — And How to Spot the Truth

Women who exploit men rarely admit it outright. Instead, they use flattering, harmless-sounding phrases to keep you invested—providing time, attention, emotional support, or money—while avoiding real commitment. This video aims to empower respectful men to recognize manipulation, not to criticize all women. Focus on actions over words: Genuine interest shows consistency and reciprocity.

:max_bytes(150000):strip_icc()/how-to-tell-if-spouse-is-lying-2300996-1500x1000-Text-Final-18b579094ea643da9c12068e49980947.png)

:max_bytes(150000):strip_icc()/10-red-flags-in-relationships-5194592-final-95724a6fa0094612b5b91caa62c8dba7.gif)

1. "I'm Over My Ex"

Hidden Meaning: He's still relevant (texts, thoughts, or contact). She cries on your shoulder, calls you "different," but posts cryptic quotes or keeps him around. You're likely a rebound filling a void. Truth Indicator: She never mentions him, doesn't stalk his socials, and mood stays stable. Red Flag: Excessive ex-talk without investment in you.

:max_bytes(150000):strip_icc()/pathologicalliar-GettyImages-1454367444-3257d2484249495f83664c8b7dd22f72.jpg)

2. "We Don't Need Labels"

Hidden Meaning: She wants boyfriend perks (dates, intimacy, support) without exclusivity or commitment. You're monogamous; she's not—still on apps or seeing others. Truth Indicator: She deletes apps, treats you like her partner (e.g., social media posts). Red Flag: Dodging "What are we?" after meaningful time together.

3. "You're Different from Other Guys"

Hidden Meaning: Buttering you up to chase harder—it's a recycled script. Feels flattering, but actions show flakiness or convenience-only contact. Truth Indicator: Consistent effort, initiation, and support for your goals. Red Flag: Words without matching behavior.

4. "I Don't Care About Money"

Hidden Meaning: She enjoys your spending but avoids contributing. Loves expensive outings you fund; low-key suggestions get excuses. Truth Indicator: Splits bills, suggests affordable dates, or surprises you. Red Flag: Lifestyle reliant on your wallet.

5. "I Don't Usually Do This"

Hidden Meaning: Standard line to make you feel uniquely chosen (e.g., intimacy or favors early). Often paired with confident delivery, not genuine shyness. Truth Indicator: Real hesitation, awkwardness, or vulnerability afterward. Red Flag: Never lend money pre-marriage—huge warning.

6. "I Just Need Space" (But Don't Want to Lose You)

Hidden Meaning: Keeps you as backup while exploring options. Still texts when bored/needy, but posts hint at others. Truth Indicator: Clear communication, timeline, and genuine follow-through. Red Flag: Breadcrumbing without risking loss.

7. "You Deserve Someone More Amazing Than Me"

Hidden Meaning: Soft rejection—flattery to ease orbiting while seeking elsewhere. Praises you as "husband material" but never commits. Truth Indicator: Full withdrawal (no mixed signals or check-ins). Red Flag: Keeps hope alive manipulatively.

8. "You Just Get Me"

Hidden Meaning: You're her free emotional support ("tampon"), not romantic partner. Unloads problems, calls you a great listener/friend, but no flirtation or dates. Truth Indicator: Reciprocal interest, physical affection, and effort. Red Flag: Friend-zone venting without romance.

9. "I'm Not Ready for a Relationship Right Now"

Hidden Meaning: Not ready—with you. Buys time until preferred option appears. Keeps contact/favors flowing, then dates someone else soon after. Truth Indicator: Clean break—no stringing along. Red Flag: Polite evasion of commitment.

These phrases hook via flattery while extracting benefits. Genuine women match words with actions: Investment, commitment, respect. Spot patterns early—prioritize reciprocity to avoid exploitation.

(Approximate reading time: 10 minutes)

Russia's Economic Strains in Late 2025: Sanctions, War Costs, and Domestic Pressures

As 2025 draws to a close, Russia's economy faces significant challenges from prolonged war spending, Western sanctions, Ukrainian strikes on infrastructure, and structural issues like labor shortages and high interest rates. While some narratives claim imminent "collapse" with hyperinflation and empty shelves, official data and independent analyses paint a picture of slowing growth, persistent inflation, and mounting fiscal strain—resilient so far due to military prioritization, but increasingly unsustainable into 2026.

Inflation and Living Standards: Elevated but Cooling

Inflation has been a major pain point, peaking earlier in the year but easing by December. Official figures show ~8-9% annual rate mid-year, dropping to ~6% by year-end (Central Bank target: below 6%).

The Central Bank cut rates to 16% in December, signaling confidence in disinflation, though expectations remain elevated. Wages grew in real terms earlier but stagnated amid cooling demand. No widespread reports of "empty shelves" or 15%+ inflation; food and essentials prices rose, but shortages are localized (e.g., fuel in some regions from strikes).

GDP Growth: Sharp Slowdown After War Boom

After ~4% growth in 2024 (war-fueled), 2025 saw deceleration: ~1-2% forecasts, with Q3 at 0.6% y/y. Central Bank projects 0.5-1%; others ~1%. Military spending (~6-8% GDP) drove prior expansion but now crowds out civilian sectors amid labor shortages and high rates.

Sanctions and Frozen Assets: Indefinite Lock and Growing Pressure

~€210bn ($246bn) in Russian Central Bank assets remain frozen in Europe (mostly Euroclear, Belgium). In December 2025, the EU made the freeze indefinite (no 6-month renewals), removing veto risks (e.g., Hungary) and facilitating potential loans to Ukraine (~€90-165bn backed by profits/collateral).

Russia sued Euroclear; no relief expected. This limits war funding and stabilization, though Russia uses National Wealth Fund and domestic borrowing.

Ukrainian Drone Strikes: Significant but Not Crippling Oil Sector

Ukraine's 2025 campaign hit ~17-20 refineries, disrupting ~10-20% capacity temporarily (peaks higher during waves). Fuel shortages emerged regionally; prices rose ~9% gasoline.

Russia offset via spare capacity; exports curbed but not collapsed. Oil revenues down (e.g., 49% drop one month), amplified by sanctions on Rosneft/Lukoil and discounts.

War Costs and Domestic Impact: Unsustainable Trajectory